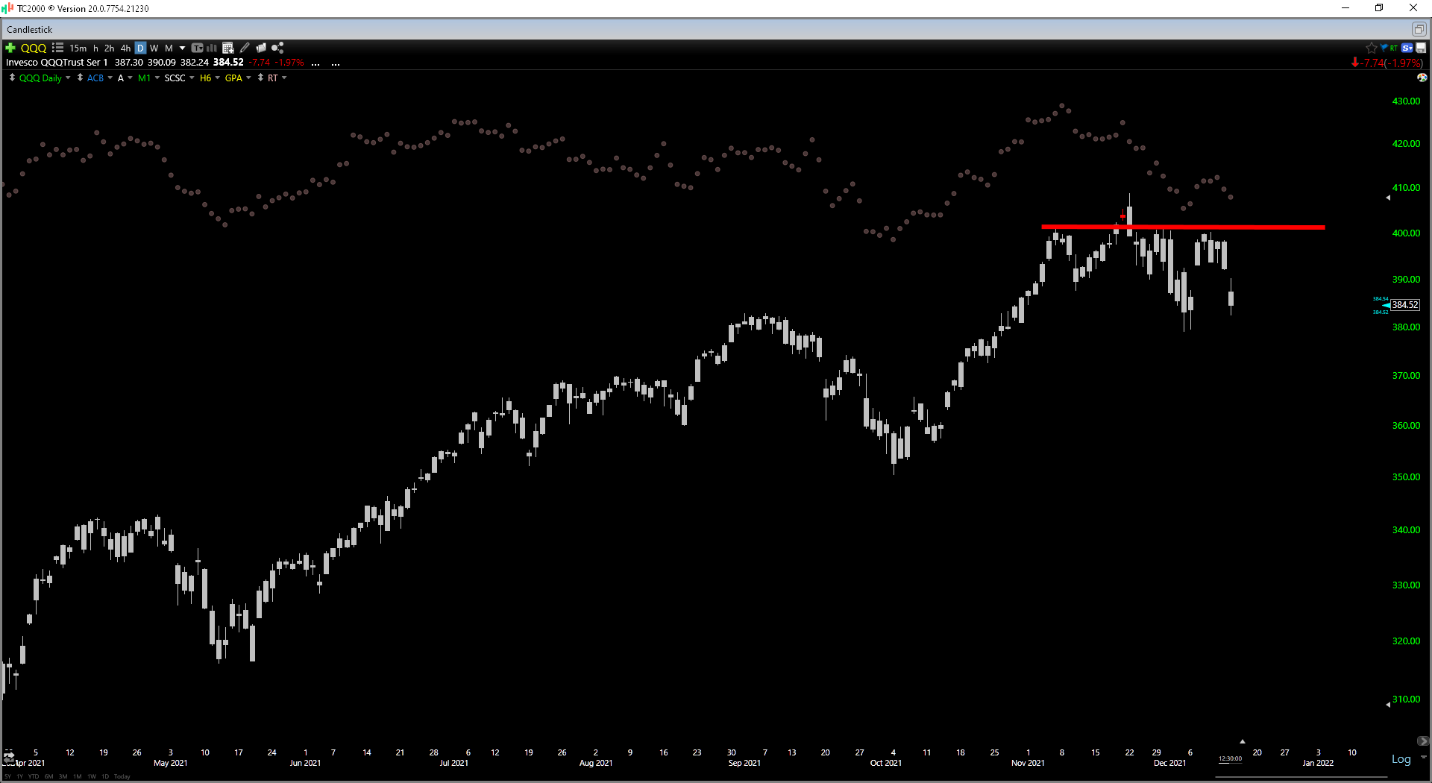

It’s been a rough start to the week so far for the Nasdaq-100 Index (QQQ), which has given up more than 2% ahead of the much-awaited and final Federal Reserve Meeting for December. The fear is that due to persistently high inflationary readings, Fed Chairman Jerome Powell could accelerate tapering of its bond purchases and potentially pull forward the initial rate hike. This has had an outsized impact on the Nasdaq-100 Index, given that this is where the valuations are the most expensive, which has only been able to be justified by the low-interest-rate environment we’re in currently.

The good news is that market volatility breeds opportunity if investors don’t panic and are patient to buy some of the highest-quality names at a deep discount to their fair value. Currently, two names are beginning to look much more interesting from a valuation standpoint within the Nasdaq-100, with these being PayPal (PYPL) and Netflix (NFLX). Let’s take a closer look at both companies below:

(Source: TC2000.com)

From a business model standpoint, NFLX and PYPL have little in common, with one hailing from the Online Payments industry group and the other being in the Leisure/Movies & Related industry group. However, both companies do share similarities from a growth standpoint, with each boasting high double-digit compound annual EPS growth rates and being leaders in their respective industry groups. However, with fears about competition for both names, we have seen multiple compression and earnings estimates continue to be scaled back for FY2022 and FY2023. Having said that, while giving up some of their business looks likely, both companies are still thriving and set to enjoy high double-digit annual EPS growth in 2022.

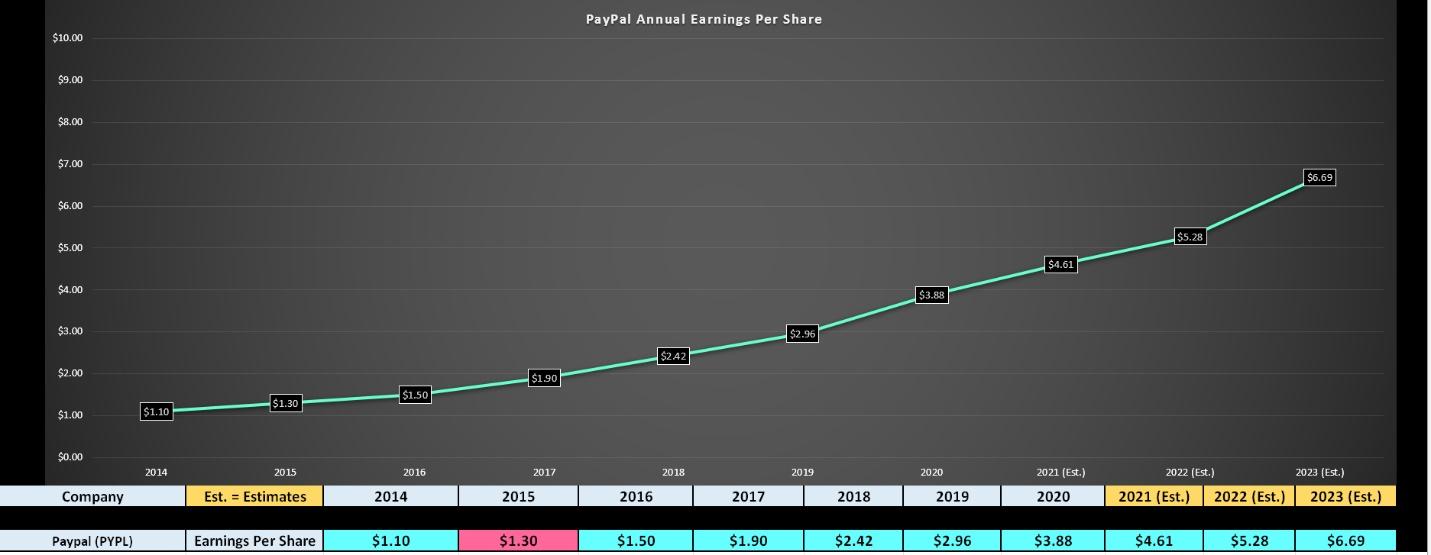

Beginning with PYPL, the company just came off a much weaker quarter in Q3, posting revenue of $1.11BB, up 13% year-over-year. This marked one of the weakest quarters for the company in the past two years and was well below its trailing 2-year sales growth rate of ~21%. However, as shown below, PayPal continues to enjoy steady annual EPS growth and is expected to grow annual EPS by more than 14% next year based on current estimates ($5.28). Looking ahead to FY2023, growth is projected to accelerate to more than 20%, with annual EPS expected to come in at $6.69.

(Source: YCharts.com, Author’s Chart)

Obviously, there is room for misses on these estimates, and two years is a long time to rely on earnings, especially with competition heating up. However, even if we see competition from names like Shopify (SHOP) and the rise of buy now pay later options. However, with PYPL more than 40% from its highs, much of this negativity is priced into the stock. This is because PYPL has historically traded at more than 45x earnings and currently trades at 35x FY2022 earnings estimates at a share price of $186.00.

Based on stiffer competition and the lower grates that we’re seeing, I would argue that a fair earnings multiple for PYPL is 40, which is much more conservative than its historical multiple. However, even at this figure and assuming PYPL misses 2023 annual EPS estimates, its fair value still comes in at $252.00. This represents a meaningful upside from current levels to its 18-month target price. So, while it’s easy to be negative on the stock while many analysts are downgrading, I believe it’s time to be open-minded that the stock may be trying to bottom out here.

(Source: TC2000.com)

Finally, if we look at the technical picture, PYPL has a support level below at $171.00 going back to last year, and no resistance until $235.00. This translates to a reward/risk ratio of better than 3 to 1 from support to resistance, suggesting that further weakness should present a low-risk buying opportunity. So, while I am not long the stock yet, I would view pullbacks below $180.00 as an opportunity to start a position in the stock.

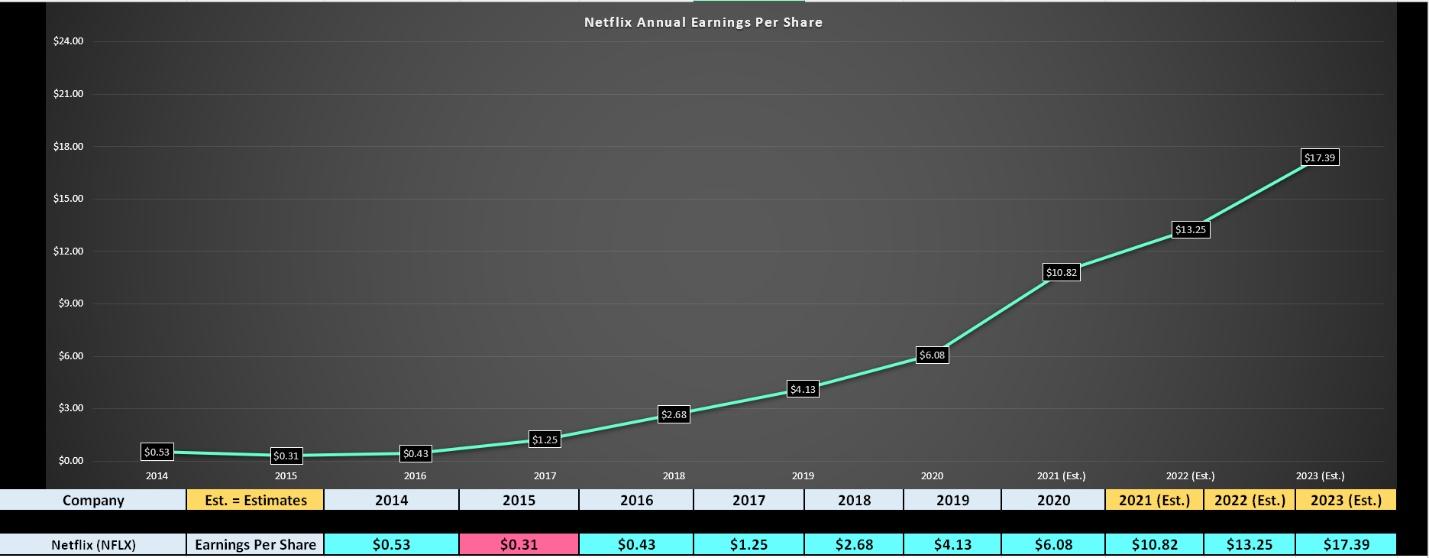

Moving over to NFLX, the company also came off a weaker quarter in Q3, with revenue up just 16%, the company’s softest quarter for growth in over two years. However, it’s important to note that this was lapping a very strong quarter of 23% growth in Q3 2020 due to the global lockdowns. Meanwhile, even though revenue was only up mid-double-digits, quarterly EPS soared by 83% to $3.19. During the quarter, the company easily beat projected paid subscriber growth of 3.84MM, coming in at 4.4MM for Q3, and the company is expecting 8.5MM members in Q4, which would translate to a solid finish to the year.

(Source: YCharts.com, Author’s Chart)

As shown in the chart below, these solid results have set NFLX up for another year of high double-digit annual EPS growth, with the company on track to grow earnings by more than 76% year-over-year ($10.82 vs. $6.08). If we look ahead to FY2022 and FY2023, estimates are sitting at $13.25 and $17.39, respectively. Assuming NFLX can meet these FY2023 estimates, this would represent 186% growth vs. FY2020 levels, with NFLX boasting a market-leading compound annual EPS growth rate of ~47% since FY2014 ($17.39 vs. $0.53).

Based on what I believe to be a fair earnings multiple of 45, I see NFLX’s fair value at ~$783.00, based on current FY2023 earnings estimates. This points to significant upside from current levels ($590.00), but I generally prefer at least a 30% discount to fair value to add to positions. This would require a dip below $548.00. As NFLX’s technical chart shows, this lines up with a very strong support level where the stock broke out from earlier this year and would represent a relatively low-risk buy point to add to positions. So, while I am neutral here but long-term bullish, I would strongly consider adding to my position below $548.00.

(Source: TC2000.com)

While several tech high-fliers remain extended from their recent bases, NFLX and PYPL have lagged some of their higher-growth peers, and sentiment is worsening on both names. This is great news, given that it has improved each stock’s valuation, and both names are now approaching their upper support levels. So, if we were to see NFLX dip below $548.00 or PYPL dip below $180.00 before the end of January, I would view this as a buying opportunity to start a position in either name.

Disclosure: I am long NFLX and short QQQ

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

PYPL shares were trading at $186.80 per share on Tuesday afternoon, up $0.42 (+0.23%). Year-to-date, PYPL has declined -20.24%, versus a 25.15% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 2 Tech Stocks to Buy on this Market Dip appeared first on StockNews.com