It’s been a volatile 4-week stretch for the major market averages, with the Nasdaq-100 Index (QQQ) correcting by more than 8% and the S&P-500 (SPY) breaking one of its longest streaks in history without a 5% correction. The good news is that this correction has removed short-term overbought conditions on the market that were present in early September. The bad news is that we still haven’t seen any real semblance of fear in the market, and valuations still remain at some of their highest levels in history. This is evidenced by the S&P-500 trading at a price-to-sales ratio just shy of 3.20, a figure that is 22% above the Dotcom Bubble peak figure of ~2.60. However, with the market now in a short-term correction, it’s a great time to start building shopping lists in case the weakness persists and we do see some fear enter the market. In this update, we’ll look at two high-growth names which are beginning to pull back towards key support levels and dig into potential low-risk buy points:

(Source: TC2000.com)

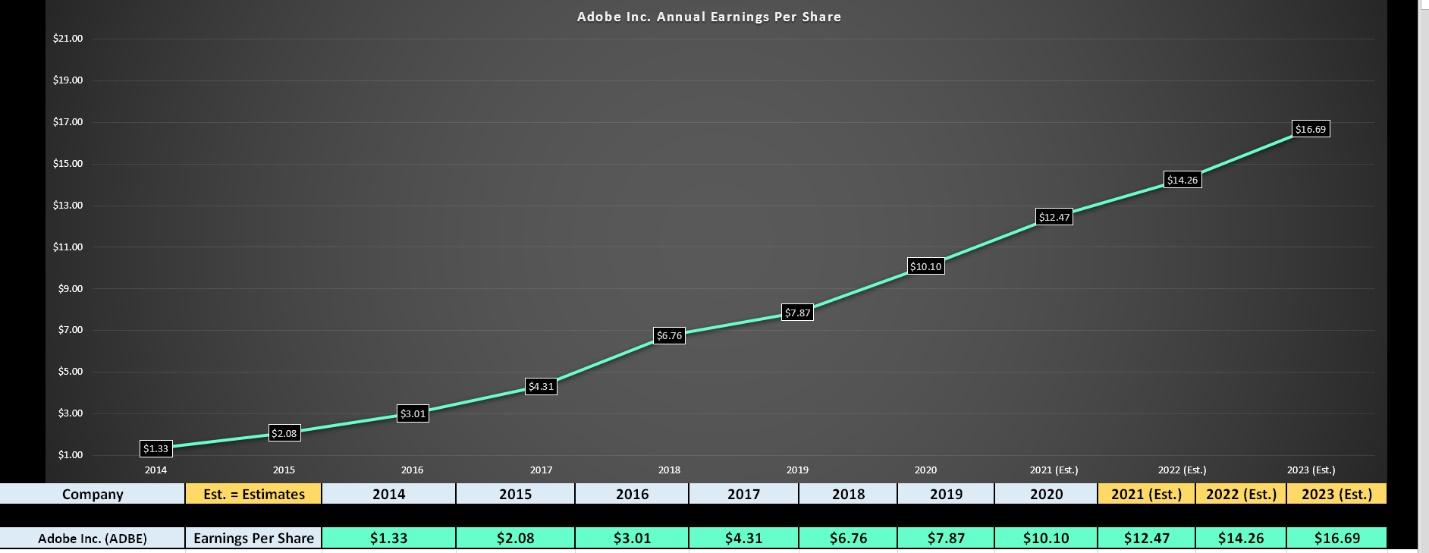

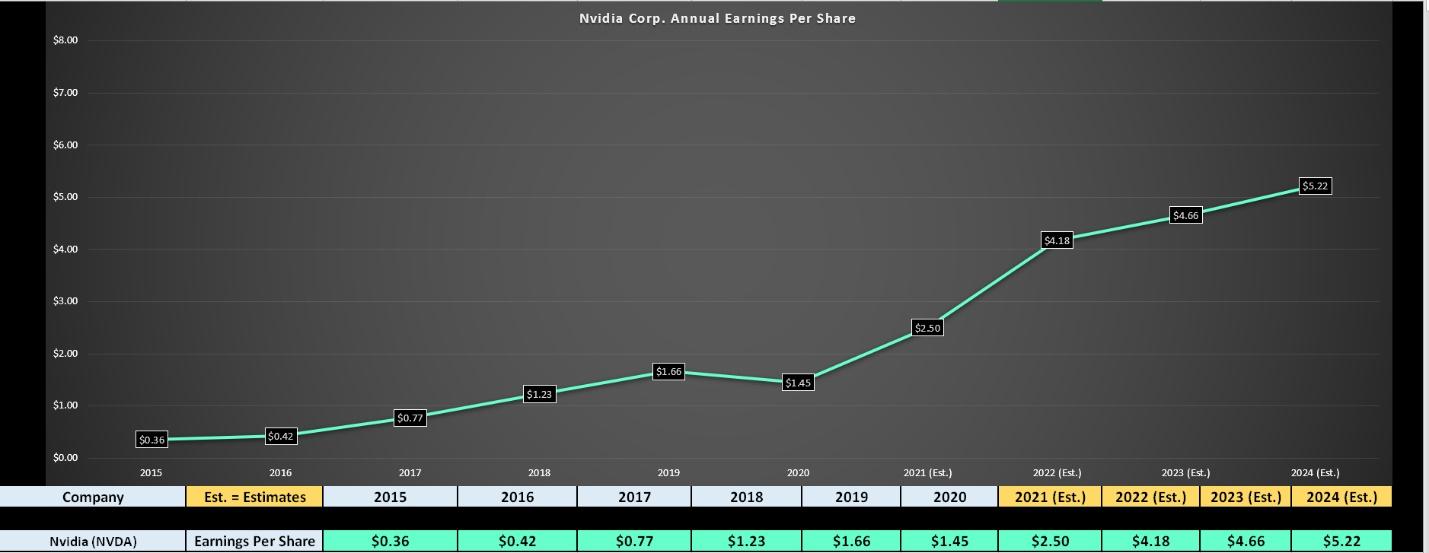

Adobe (ADBE) and Nvidia (NVDA) have little in common as they hail from different industry groups, but they do share two key traits: they both have a track record of steady earnings growth with compound annual earnings growth rates above 35% since 2014, and they both continue to find strong support at their 40-week moving averages on any pullbacks. In ADBE’s case, the stock has a 40% compound annual EPS growth rate since FY2014 and just came off a strong quarter with 22% sales growth. In NVDA’s case, the stock has an incredible ~38% compound annual EPS growth rate for a mega-cap company and just had its second strongest quarter in the past two years from a sales growth standpoint, posting 68% revenue growth while lapping 50% growth in the year-ago period. Let’s take a closer look at both companies below:

Adobe just came off an outstanding quarter in late September, with sales up 22% year-over-year to $3.94BB, helping by record performance in its Digital Media business. This segment posted revenue of $2.87BB, up 23% year-over-year, and Document Cloud also continues to perform well, with transactions up exponentially over the past three years. Given the strong sales growth and slight margin expansion, ADBE is on track for meaningful growth in annual EPS this year, with estimates currently sitting at $12.47. This would translate to 23% growth vs. FY2020 levels, with continued high double-digit growth expected in FY2022 and FY2023. Based on FY2023 estimates of $16.69, ADBE currently trades at just ~35x earnings, which is a very reasonable valuation for this growth story with an industry-leading return on equity figure of 41%.

(Source: YCharts.com, Author’s Chart)

Looking at the technical picture below, we can see that ADBE got quite overbought heading into earnings, which explains why the stock fell sharply despite what was a decent report. However, this sharp pullback has now left ADBE sitting right on top of its trend line off the March 2020 lows and just above its prior breakout level near $515.00. If the stock were to come within 5% of backtesting this breakout area, this would likely help to shake out further weak hands and leave ADBE trading at barely ~30x FY2023 earnings estimates. So, if this weakness continues and ADBE dips below $535.00, I would view this as a low-risk buying opportunity.

(Source: TC2000.com)

Moving over to NVDA, the company has significant tailwinds given the strength of the Semiconductor Industry, with the recent World Semiconductor Trade Statistics Report suggesting that the market should increase by ~9% in 2022 and grow to nearly $1TT by 2030. This would translate to a compound annual growth rate of 8.5% for the decade (2020-2030), and Nvidia is clearly a market leader, growing at quadruple this pace with an average revenue growth rate of ~67% on a trailing-twelve-month basis. The company just released its Q2 results in late August and reported revenue of ~$6.51BB, a new record driven by impressive strength in gaming, which soared 85% year-over-year. The company also called out laptop demand as very strong and announced two new GPUs for gamers and creators, the GeForce RTX 3080 Ti, and the RTX 3070 Ti. These offer 50% faster performance than their predecessors, with features like real-time retracing, Reflex, and DLSS.

(Source: YCharts.com, Author’s Chart)

As the chart above shows, the strong results have set NVDA up for impressive annual EPS growth in FY2022, with FY2022 annual EPS estimates currently sitting at $4.18, up from $2.50 in FY2021 and $1.45 in FY2020. This would translate to 67% growth year-over-year after lapping 72% growth in FY2021, making NVDA one of the highest growth mega-cap companies in the market. Looking ahead to FY2024, we are likely to see some deceleration after two back-to-back years of high-double growth, but annual EPS is still forecasted to grow another 25% from FY2022 levels. So, while the stock may appear a little expensive at more than 80x FY2021 earnings, it’s actually quite reasonably valued relative to FY2023 earnings estimates, sitting at just 45x estimates of $4.66. This doesn’t mean that the stock has to bottom here, but it suggests that the valuation will become quite compelling if we see a deeper correction.

(Source: TC2000.com)

If we look at NVDA’s technical chart above, we can see that Nvidia broke out of a massive base earlier this year and is now re-testing an 18-month uptrend line off the March 2020 lows. With this being the 4th test of this uptrend line and a somewhat obvious support level, it is quite possible that NVDA could see a shake-out below its recent low at $195.00. Having said that, if the stock were to undercut this level, it would find itself just above its 40-week moving average (purple line), which has provided very strong support over the past two years. So, if this correction in NVDA does continue, I would view any pullbacks below $181.00 as a low-risk area to start a position. Notably, if the stock were to pull back this sharply, it would reset trade an even more attractive valuation of just 39x FY2023 earnings estimates. In summary, while I’m not in a rush to buy NVDA yet, I do think it’s a very solid buy-the-dip candidate if we do see a deeper pullback.

With a limited amount of fear in the market, I still don’t see this as the time to rush in and buy the dip, but NVDA and ADBE look like two names to keep a very close eye on if we do see more turbulence. As noted above, I would view any dips below $181.00 on NVDA as a low-risk buying opportunity, with ADBE becoming attractive from a swing trading standpoint below $532.00

Disclosure: I have no positions in any names mentioned.

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

NVDA shares were trading at $211.69 per share on Thursday afternoon, up $4.69 (+2.27%). Year-to-date, NVDA has gained 62.25%, versus a 18.98% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post BUY the Dip on These 2 Tech Stocks appeared first on StockNews.com