Over the past six months, Stanley Black & Decker’s shares (currently trading at $69.06) have posted a disappointing 19.5% loss, well below the S&P 500’s 4.5% gain. This might have investors contemplating their next move.

Is there a buying opportunity in Stanley Black & Decker, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Stanley Black & Decker Will Underperform?

Despite the more favorable entry price, we're cautious about Stanley Black & Decker. Here are three reasons why there are better opportunities than SWK and a stock we'd rather own.

1. Core Business Falling Behind as Demand Declines

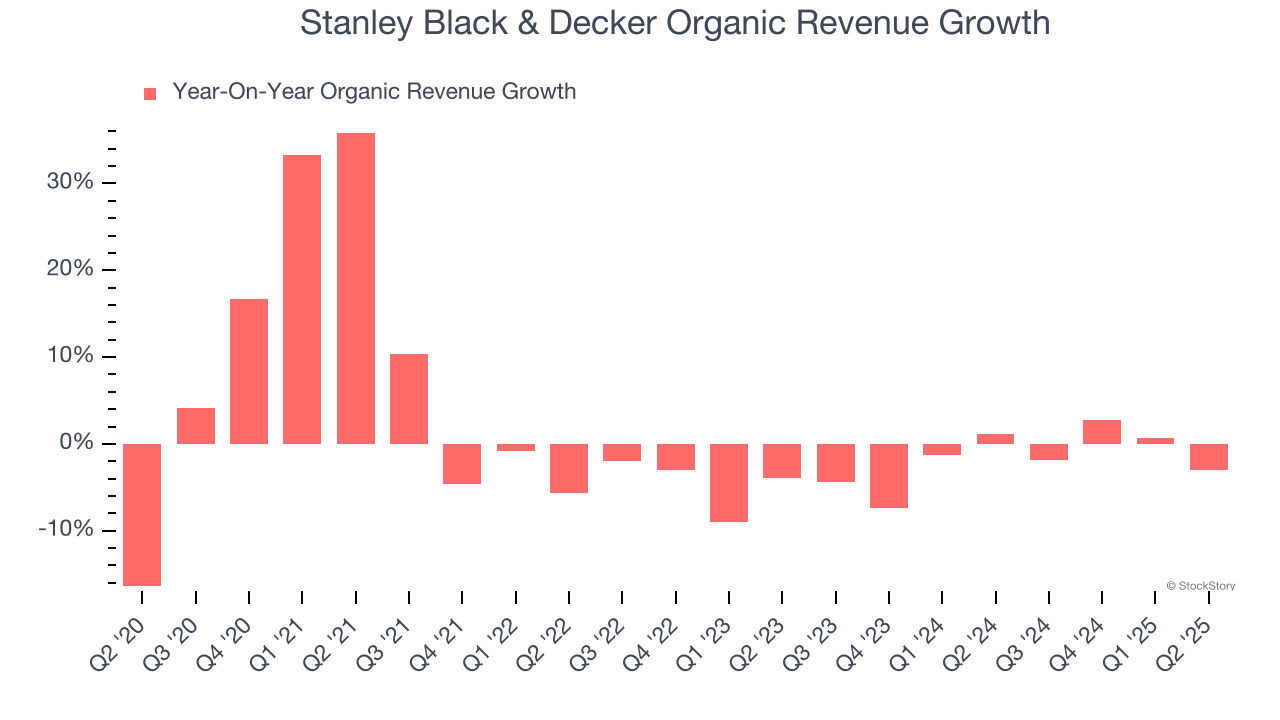

We can better understand Professional Tools and Equipment companies by analyzing their organic revenue. This metric gives visibility into Stanley Black & Decker’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Stanley Black & Decker’s organic revenue averaged 1.7% year-on-year declines. This performance was underwhelming and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests Stanley Black & Decker might have to lean into acquisitions to grow, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

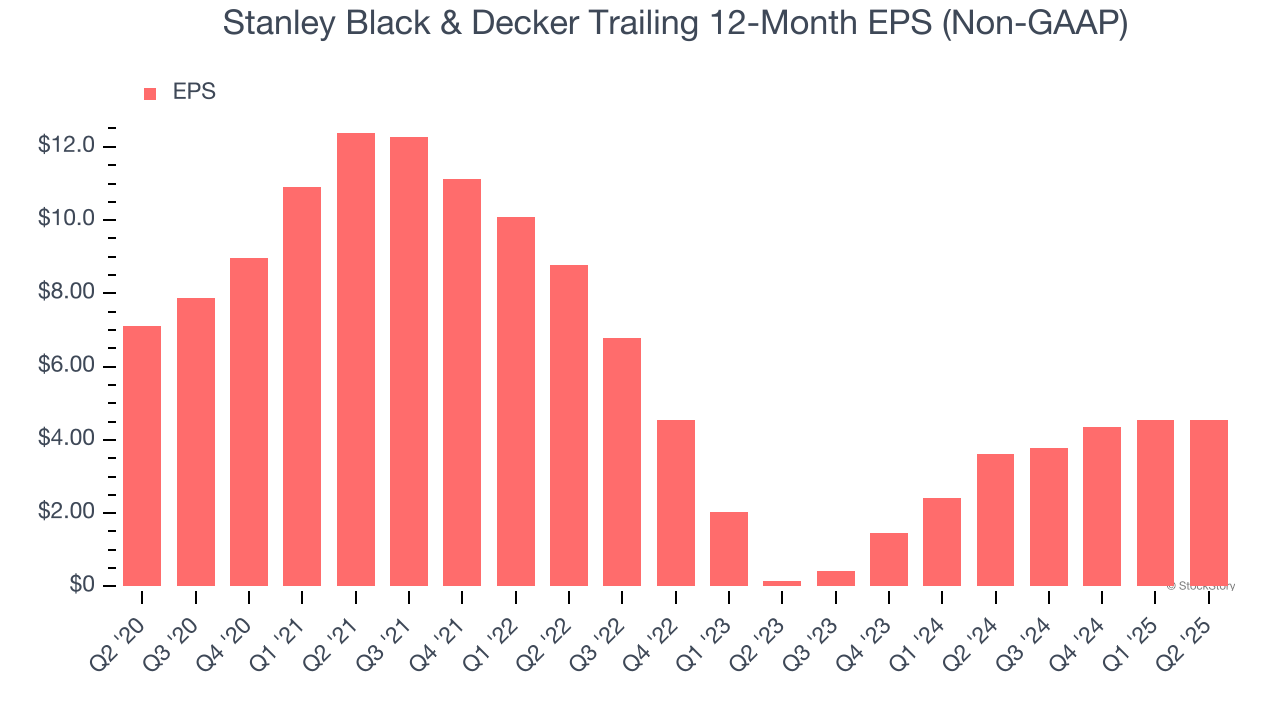

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Stanley Black & Decker, its EPS declined by 8.6% annually over the last five years while its revenue grew by 3.3%. This tells us the company became less profitable on a per-share basis as it expanded.

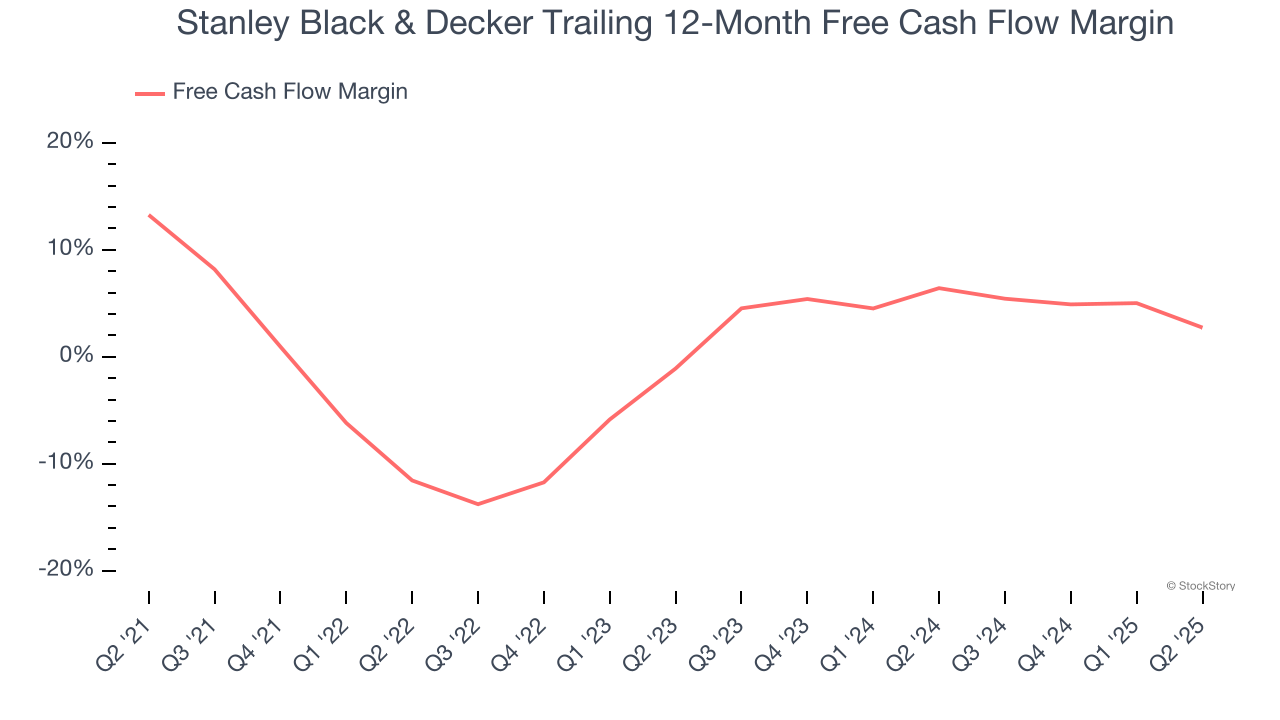

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Stanley Black & Decker’s margin dropped by 10.5 percentage points over the last five years. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s in the middle of a big investment cycle. Stanley Black & Decker’s free cash flow margin for the trailing 12 months was 2.7%.

Final Judgment

We cheer for all companies making their customers lives easier, but in the case of Stanley Black & Decker, we’ll be cheering from the sidelines. After the recent drawdown, the stock trades at 12× forward P/E (or $69.06 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are superior stocks to buy right now. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

High-Quality Stocks for All Market Conditions

Donald Trump’s April 2024 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.