Over the past six months, Verisk’s shares (currently trading at $265.69) have posted a disappointing 10.2% loss, well below the S&P 500’s 5% gain. This might have investors contemplating their next move.

Given the weaker price action, is this a buying opportunity for VRSK? Find out in our full research report, it’s free.

Why Does Verisk Spark Debate?

Processing over 2.8 billion insurance transaction records annually through one of the world's largest private databases, Verisk Analytics (NASDAQ: VRSK) provides data, analytics, and technology solutions that help insurance companies assess risk, detect fraud, and make better business decisions.

Two Positive Attributes:

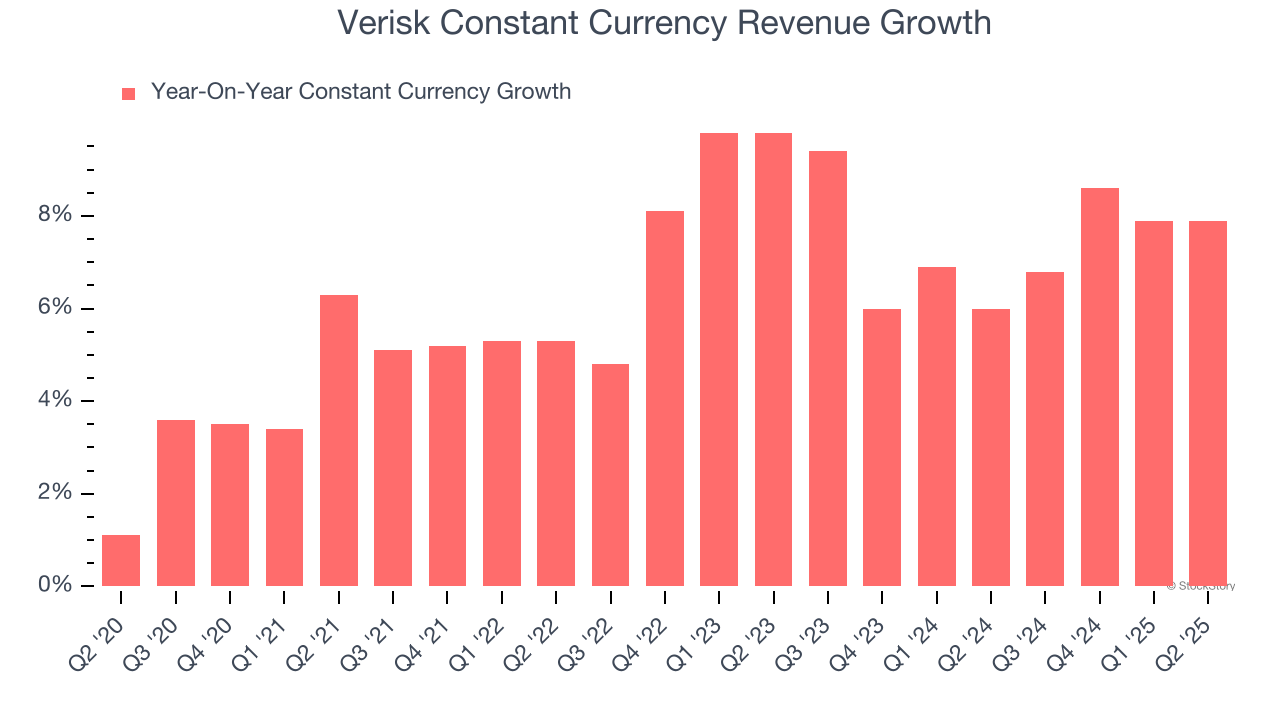

1. Constant Currency Revenue Drives Growth

Investors interested in Data & Business Process Services companies should track constant currency revenue in addition to reported revenue. This metric excludes currency movements, which are outside of Verisk’s control and are not indicative of underlying demand.

Over the last two years, Verisk’s constant currency revenue averaged 7.4% year-on-year growth. This performance was solid and shows it can expand steadily on a global scale regardless of the macroeconomic environment.

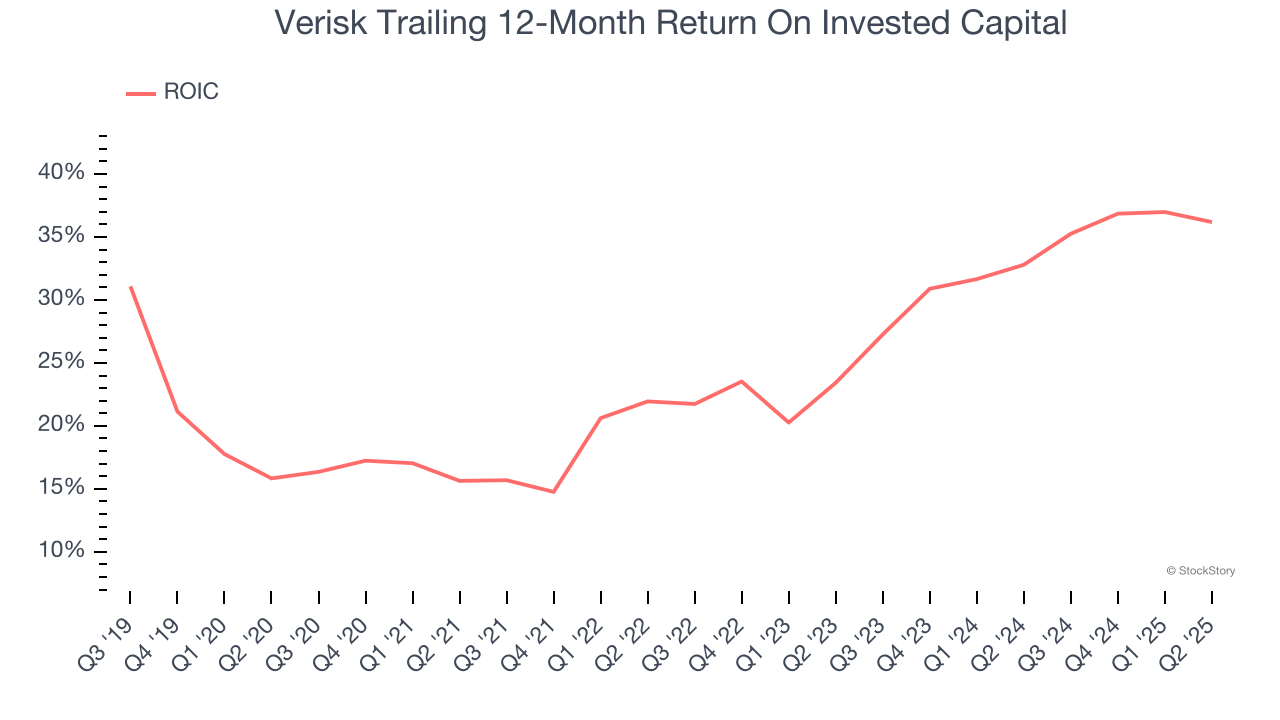

2. New Investments Bear Fruit as ROIC Jumps

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Verisk’s ROIC has increased significantly over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

One Reason to be Careful:

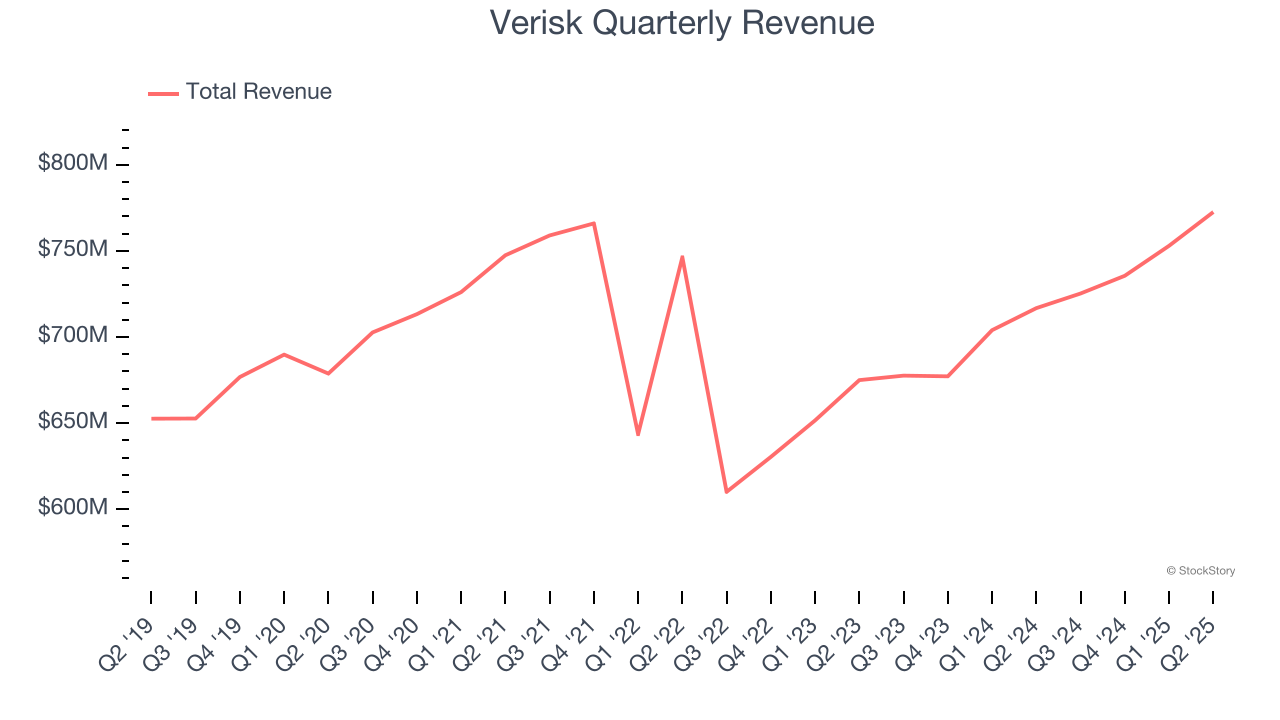

Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality.

Any business can put up a good quarter or two, but many enduring ones grow for years.

Over the last five years, Verisk grew its sales at a sluggish 2.1% compounded annual growth rate. This wasn’t a great result, but there are still things to like about Verisk.

Final Judgment

Verisk’s positive characteristics outweigh the negatives. After the recent drawdown, the stock trades at 35.8× forward P/E (or $265.69 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Verisk

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.