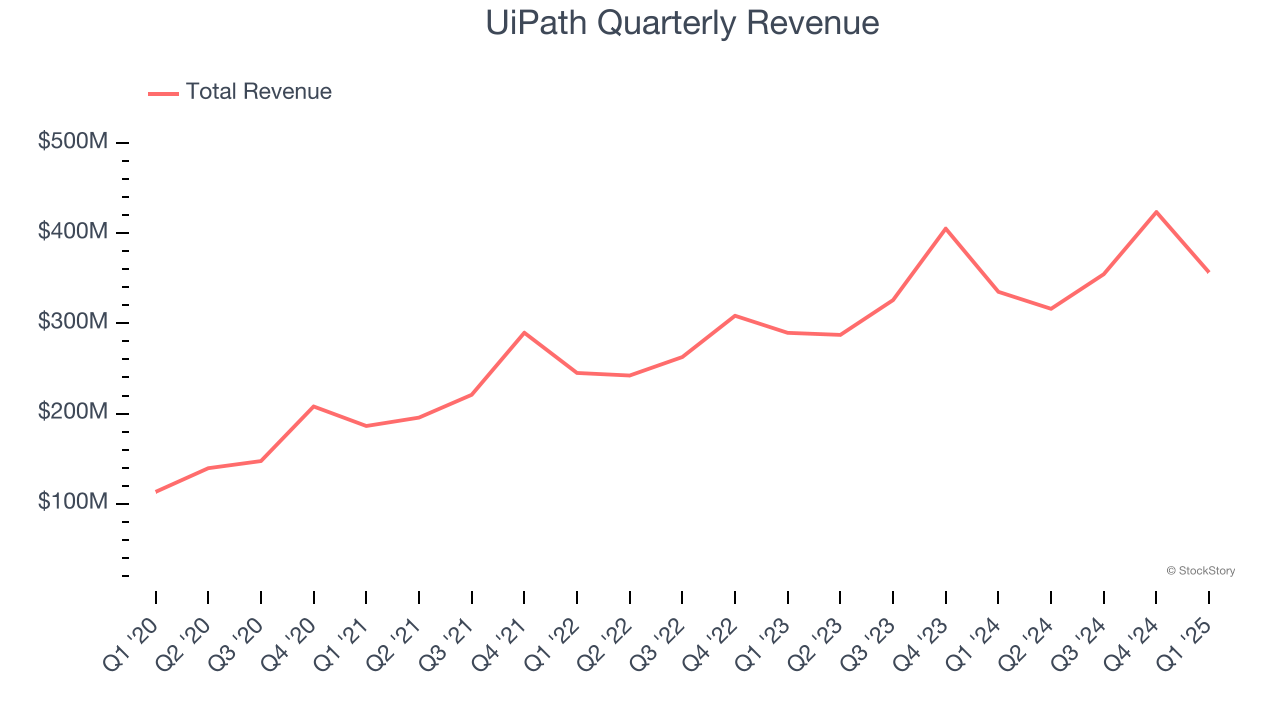

Automation software company UiPath (NYSE: PATH) beat Wall Street’s revenue expectations in Q1 CY2025, with sales up 6.4% year on year to $356.6 million. On top of that, next quarter’s revenue guidance ($347.5 million at the midpoint) was surprisingly good and 5% above what analysts were expecting. Its non-GAAP profit of $0.11 per share was in line with analysts’ consensus estimates.

Is now the time to buy UiPath? Find out by accessing our full research report, it’s free.

UiPath (PATH) Q1 CY2025 Highlights:

- Revenue: $356.6 million vs analyst estimates of $332 million (6.4% year-on-year growth, 7.4% beat)

- Adjusted EPS: $0.11 vs analyst estimates of $0.10 (in line)

- Adjusted Operating Income: $69.62 million vs analyst estimates of $45 million (19.5% margin, 54.7% beat)

- The company lifted its revenue guidance for the full year to $1.55 billion at the midpoint from $1.53 billion, a 1.6% increase

- Operating Margin: -4.6%, up from -14.8% in the same quarter last year

- Free Cash Flow Margin: 29.8%, down from 34.2% in the previous quarter

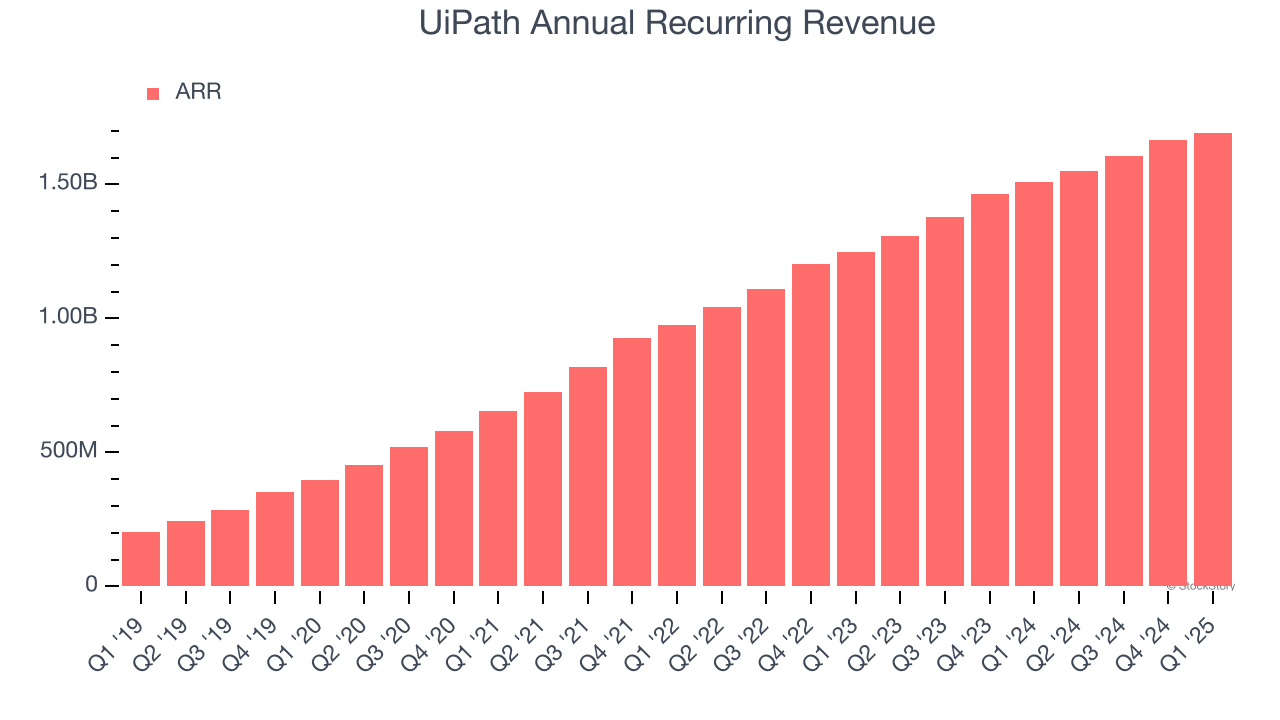

- Annual Recurring Revenue: $1.69 billion at quarter end, up 12.3% year on year

- Market Capitalization: $6.92 billion

“I'm pleased with our first quarter results, highlighted by ARR of $1.693 billion, up 12 percent year-over-year, a reflection of our improved execution and the meaningful ROI our customers are realizing through our automation platform,” said Daniel Dines, UiPath Founder and Chief Executive Officer.

Company Overview

Started in 2005 in Romania as a tech outsourcing company, UiPath (NYSE: PATH) makes software that helps companies automate repetitive computer tasks.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last three years, UiPath grew its sales at a 15.1% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our standards for the software sector, which enjoys a number of secular tailwinds.

This quarter, UiPath reported year-on-year revenue growth of 6.4%, and its $356.6 million of revenue exceeded Wall Street’s estimates by 7.4%. Company management is currently guiding for a 9.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 7.1% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and indicates its products and services will face some demand challenges.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

UiPath’s ARR punched in at $1.69 billion in Q1, and over the last four quarters, its growth was solid as it averaged 15.3% year-on-year increases. This alternate topline metric grew faster than total sales, which likely means that the recurring portions of the business are growing faster than less predictable, choppier ones such as implementation fees. That could be a good sign for future revenue growth.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

UiPath’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a competitive market and must continue investing to grow.

Key Takeaways from UiPath’s Q1 Results

It was great to see UiPath’s revenue and adjusted operating income trump analysts’ expectations. We were also glad it lifted its full-year revenue guidance. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 9.9% to $14.24 immediately following the results.

UiPath may have had a good quarter, but does that mean you should invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.