As the Q4 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the data & business process services industry, including Broadridge (NYSE: BR) and its peers.

A combination of increasing reliance on data and analytics across various industries and the desire for cost efficiency through outsourcing could mean that companies in this space gain. As functions such as payroll, HR, and credit risk assessment rely on more digitization, key players in the data & business process services industry could be increased demand. On the other hand, the sector faces headwinds from growing regulatory scrutiny on data privacy and security, with laws like GDPR and evolving U.S. regulations potentially limiting data collection and monetization strategies. Additionally, rising cyber threats pose risks to firms handling sensitive personal and financial information, creating outsized headline risk when things go wrong in this area.

The 11 data & business process services stocks we track reported a mixed Q4. As a group, revenues along with next quarter’s revenue guidance were in line with analysts’ consensus estimates.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 9.3% since the latest earnings results.

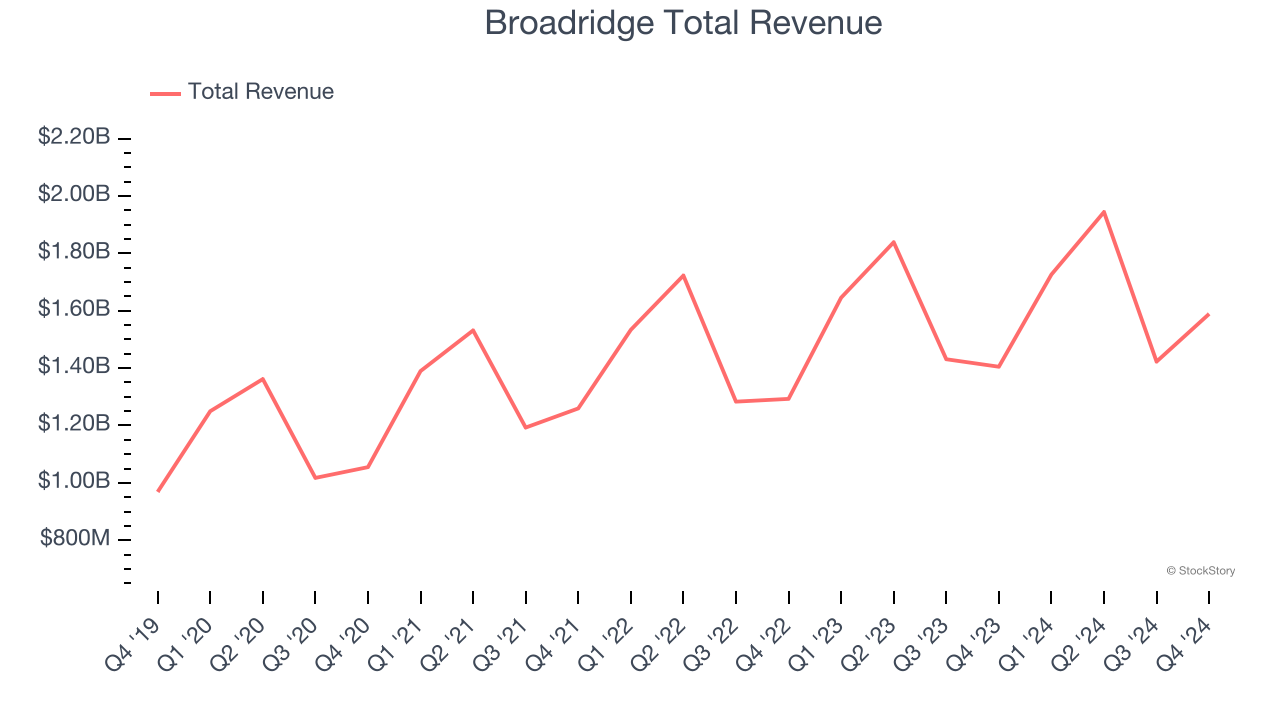

Broadridge (NYSE: BR)

Processing over $10 trillion in equity and fixed income trades daily and managing proxy voting for over 800 million equity positions, Broadridge Financial Solutions (NYSE: BR) provides technology-driven solutions that power investing, governance, and communications for banks, broker-dealers, asset managers, and public companies.

Broadridge reported revenues of $1.59 billion, up 13.1% year on year. This print exceeded analysts’ expectations by 2.7%. Overall, it was a satisfactory quarter for the company with a decent beat of analysts’ EPS estimates but revenue guidance for next quarter slightly missing analysts’ expectations.

The stock is down 5% since reporting and currently trades at $227.29.

Is now the time to buy Broadridge? Access our full analysis of the earnings results here, it’s free.

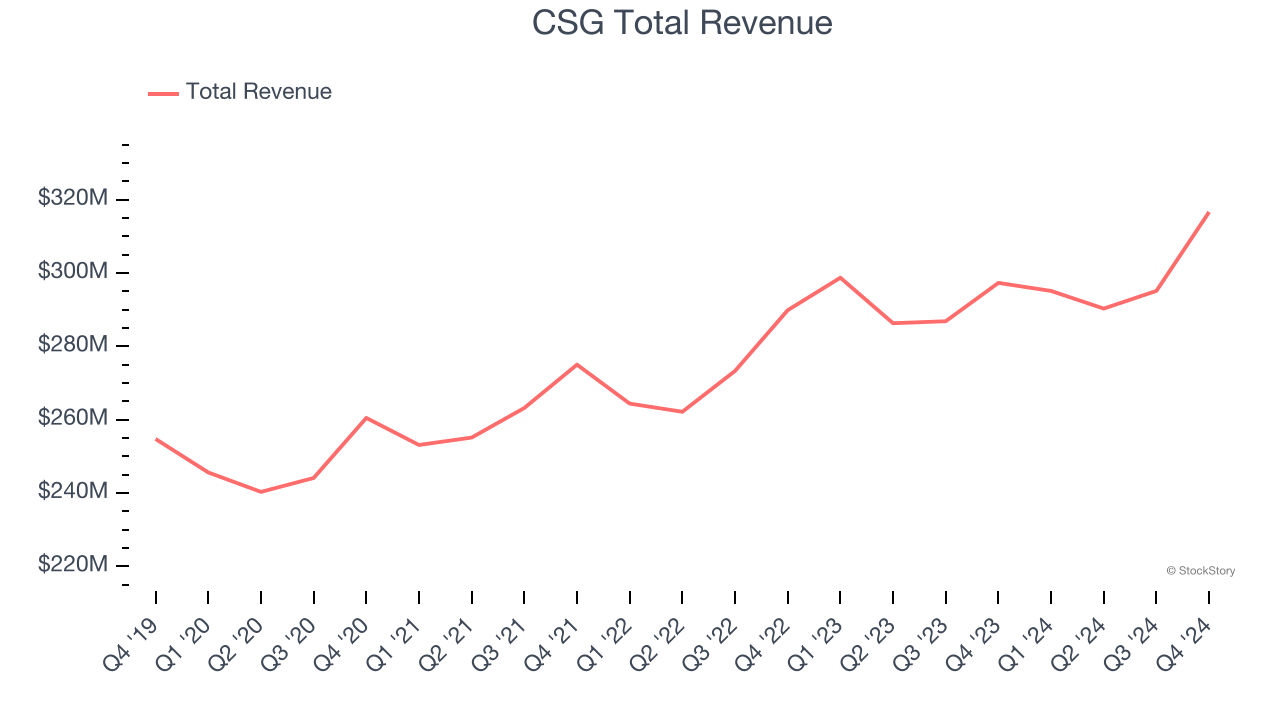

Best Q4: CSG (NASDAQ: CSGS)

Powering billions of critical customer interactions annually, CSG Systems (NASDAQ: CSGS) provides cloud-based software platforms that help companies manage customer interactions, process payments, and monetize their services.

CSG reported revenues of $316.7 million, up 6.5% year on year, in line with analysts’ expectations. The business had an exceptional quarter with a solid beat of analysts’ EPS estimates and full-year revenue guidance exceeding analysts’ expectations.

CSG scored the highest full-year guidance raise among its peers. The stock is down 4% since reporting. It currently trades at $58.44.

Is now the time to buy CSG? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Dun & Bradstreet (NYSE: DNB)

Known for its proprietary D-U-N-S Number that serves as a unique identifier for businesses worldwide, Dun & Bradstreet (NYSE: DNB) provides business decisioning data and analytics that help companies evaluate credit risks, verify suppliers, enhance sales productivity, and gain market visibility.

Dun & Bradstreet reported revenues of $631.9 million, flat year on year, falling short of analysts’ expectations by 4%. It was a disappointing quarter as it posted a significant miss of analysts’ full-year EPS guidance estimates.

Dun & Bradstreet delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 17.9% since the results and currently trades at $8.62.

Read our full analysis of Dun & Bradstreet’s results here.

TransUnion (NYSE: TRU)

One of the three major credit bureaus in the United States alongside Equifax and Experian, TransUnion (NYSE: TRU) is a global information and insights company that provides credit reports, fraud prevention tools, and data analytics to help businesses make decisions and consumers manage their financial health.

TransUnion reported revenues of $1.04 billion, up 8.6% year on year. This print beat analysts’ expectations by 1%. Taking a step back, it was a softer quarter with EPS guidance for the next quarter missing analysts’ expectations.

The stock is down 16% since reporting and currently trades at $78.56.

Read our full, actionable report on TransUnion here, it’s free.

EXL (NASDAQ: EXLS)

Originally founded as an outsourcing company in 1999 before evolving into a technology-focused enterprise, EXL (NASDAQ: EXLS) provides data analytics and AI-powered digital operations solutions that help businesses transform their operations and make better decisions.

EXL reported revenues of $481.4 million, up 16.3% year on year. This number surpassed analysts’ expectations by 1.1%. Zooming out, it was a slower quarter as it produced a miss of analysts’ full-year EPS guidance estimates.

EXL pulled off the fastest revenue growth among its peers. The stock is down 10.8% since reporting and currently trades at $43.40.

Read our full, actionable report on EXL here, it’s free.

Market Update

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty for 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.