Customer experience solutions provider Concentrix (NASDAQ: CNXC) met Wall Street’s revenue expectations in Q1 CY2025, but sales fell by 1.3% year on year to $2.37 billion. The company expects next quarter’s revenue to be around $2.38 billion, coming in 0.6% above analysts’ estimates. Its non-GAAP profit of $2.79 per share was 7.8% above analysts’ consensus estimates.

Is now the time to buy Concentrix? Find out by accessing our full research report, it’s free.

Concentrix (CNXC) Q1 CY2025 Highlights:

- Revenue: $2.37 billion vs analyst estimates of $2.36 billion (1.3% year-on-year decline, in line)

- Adjusted EPS: $2.79 vs analyst estimates of $2.59 (7.8% beat)

- Adjusted EBITDA: $374.2 million vs analyst estimates of $372.3 million (15.8% margin, 0.5% beat)

- The company slightly lifted its revenue guidance for the full year to $9.56 billion at the midpoint from $9.54 billion

- Management reiterated its full-year Adjusted EPS guidance of $11.48 at the midpoint

- Operating Margin: 7.1%, in line with the same quarter last year

- Free Cash Flow was -$49.21 million compared to -$102.9 million in the same quarter last year

- Market Capitalization: $2.91 billion

“Our first quarter results demonstrate our progress as we win quality business and take advantage of GenAI opportunities, leveraging our unique technology and service capabilities to drive our clients’ success,” said Chris Caldwell, President and CEO of Concentrix.

Company Overview

With a team of approximately 450,000 employees across 75 countries, Concentrix (NASDAQ: CNXC) designs and delivers customer experience solutions that help global brands manage their customer interactions across digital channels and contact centers.

Business Process Outsourcing & Consulting

The sector stands to benefit from ongoing digital transformation, increasing corporate demand for cost efficiencies, and the growing complexity of regulatory and cybersecurity landscapes. For those that invest wisely, AI and automation capabilities could emerge as competitive advantages, enhancing process efficiencies for the companies themselves as well as their clients. On the flip side, AI could be a headwind as well as the technology could lower the barrier to entry in the space and give rise to more self-service solutions. Additional challenges in the years ahead could include wage inflation for highly skilled consultants and potential regulatory scrutiny on outsourcing practices—especially in industries like finance and healthcare where who has access to certain data matters greatly.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $9.59 billion in revenue over the past 12 months, Concentrix is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions.

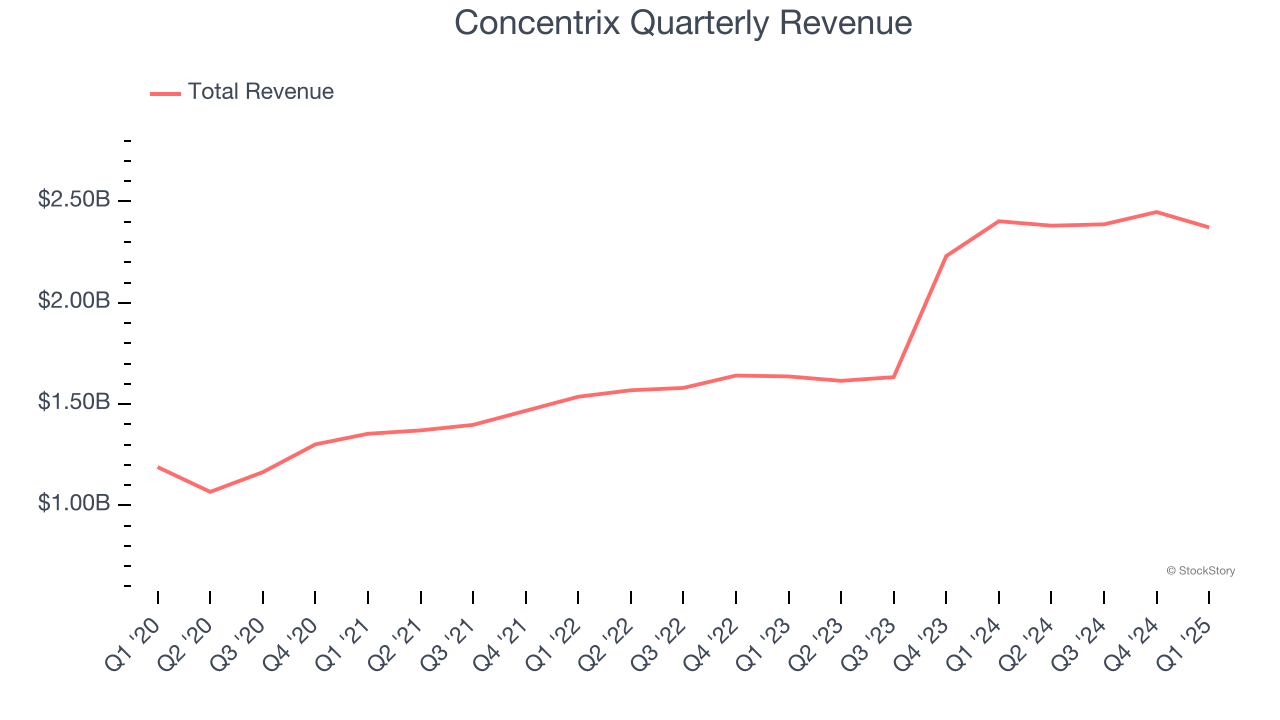

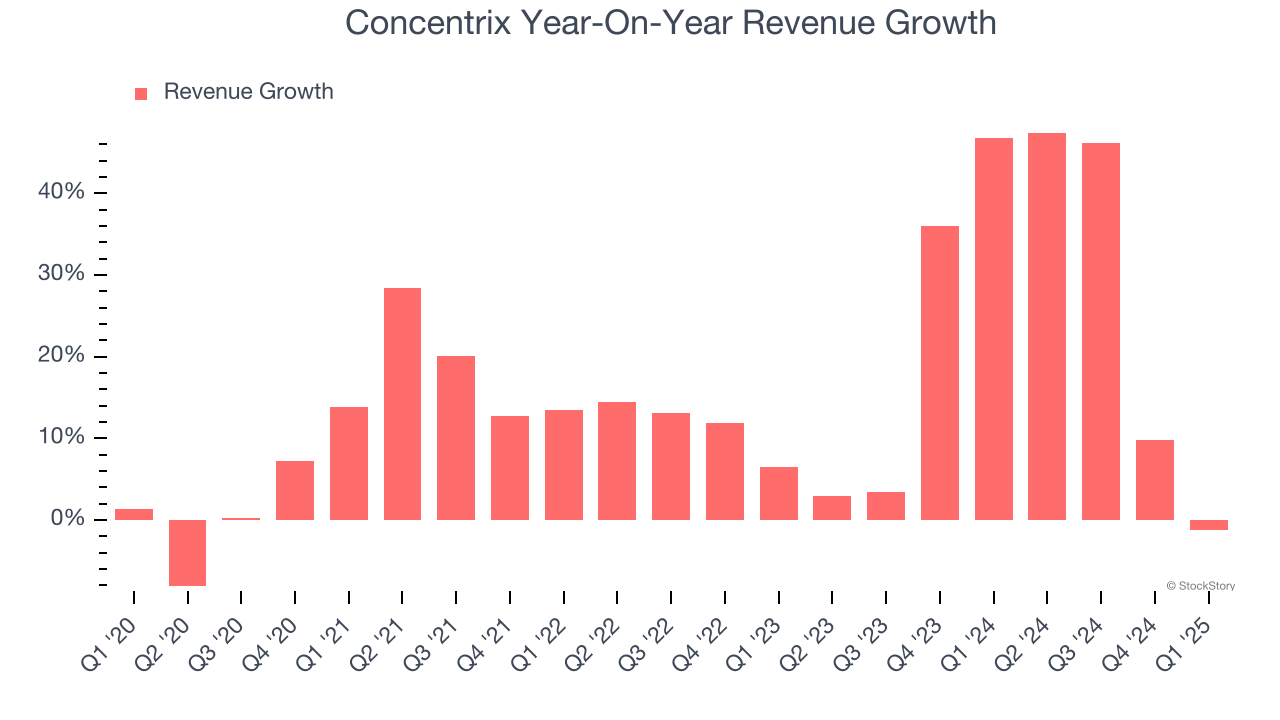

As you can see below, Concentrix’s sales grew at an incredible 15.2% compounded annual growth rate over the last five years. This shows it had high demand, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Concentrix’s annualized revenue growth of 22.2% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Concentrix reported a rather uninspiring 1.3% year-on-year revenue decline to $2.37 billion of revenue, in line with Wall Street’s estimates. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

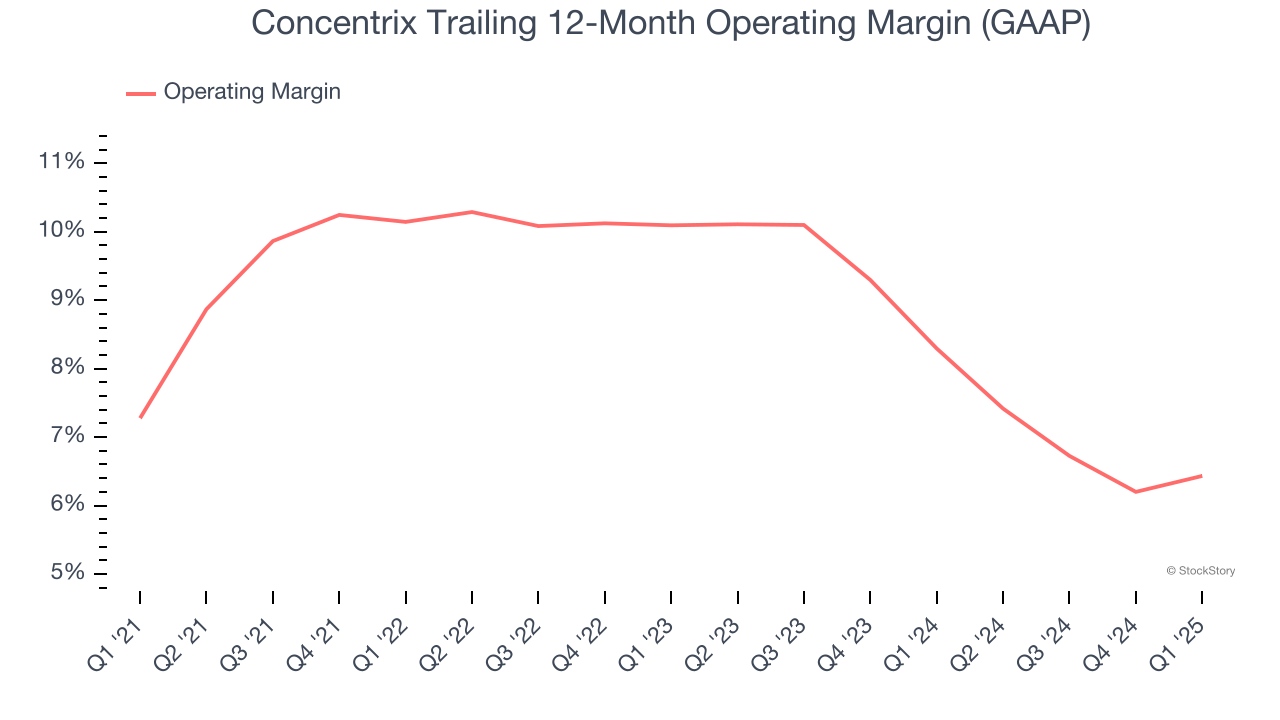

Concentrix was profitable over the last five years but held back by its large cost base. Its average operating margin of 8.3% was weak for a business services business.

Looking at the trend in its profitability, Concentrix’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q1, Concentrix generated an operating profit margin of 7.1%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

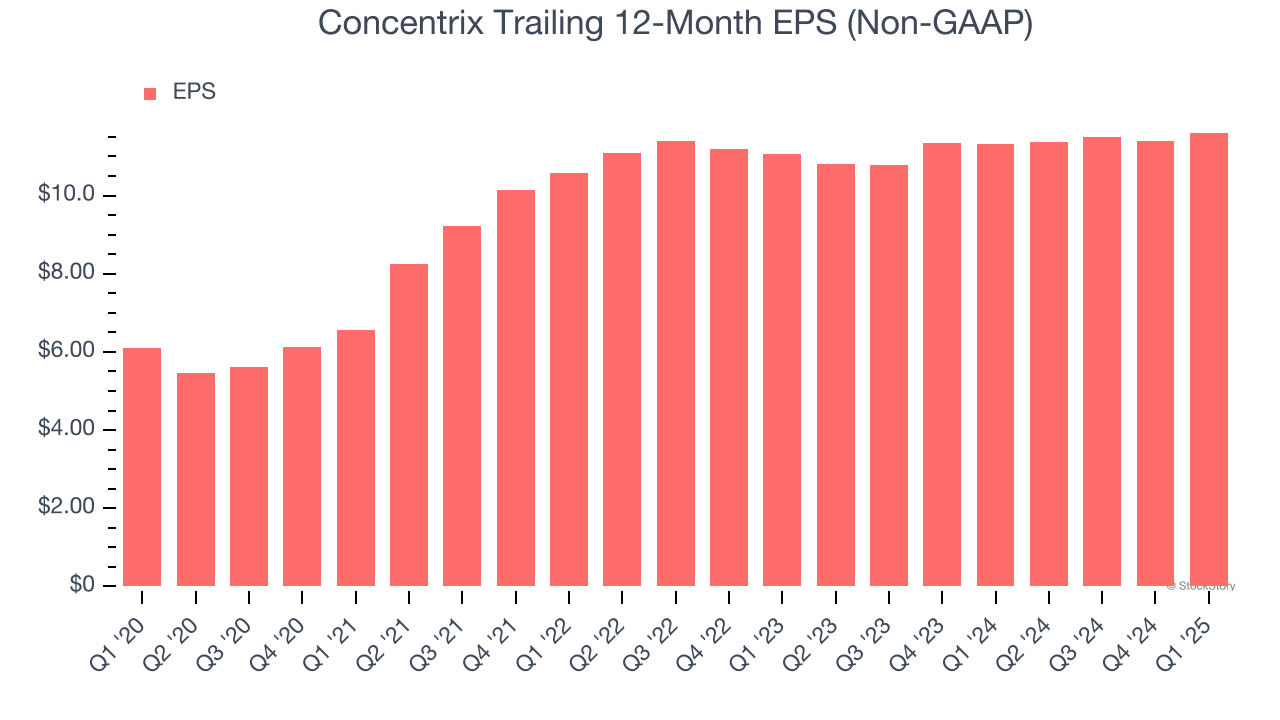

Concentrix’s EPS grew at a spectacular 13.8% compounded annual growth rate over the last five years. However, this performance was lower than its 15.2% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded.

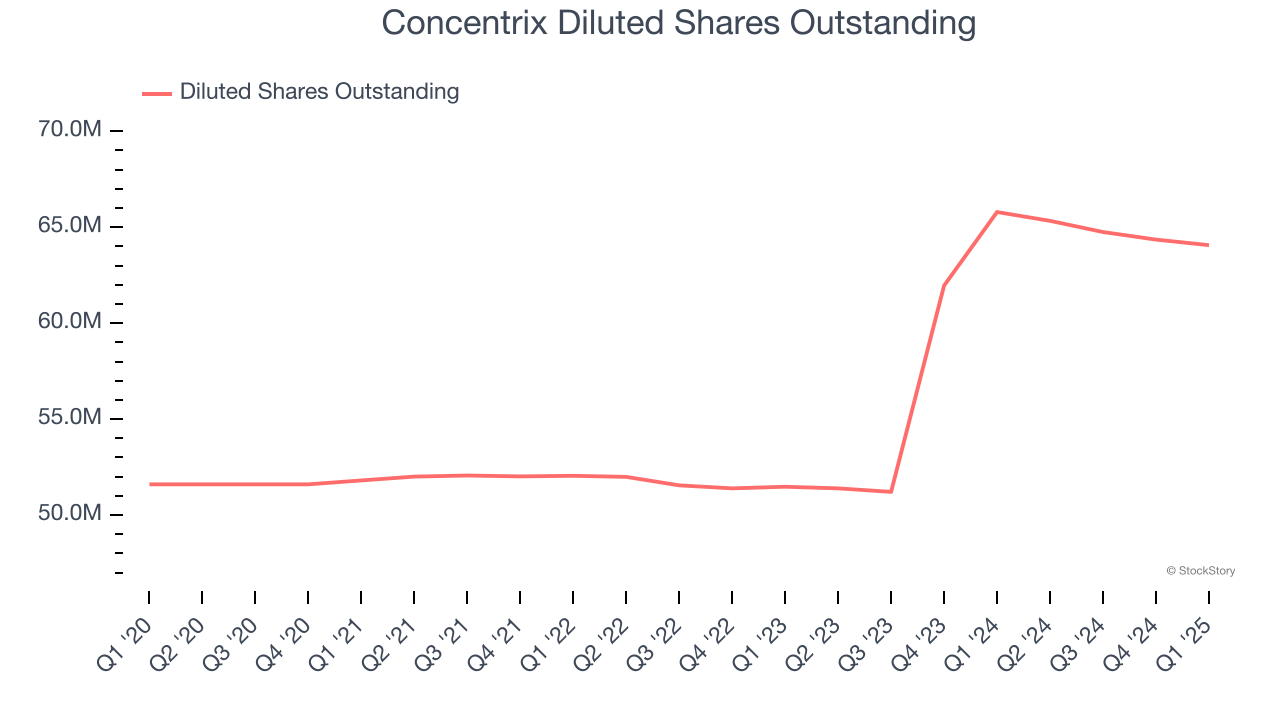

Diving into Concentrix’s quality of earnings can give us a better understanding of its performance. Concentrix recently raised equity capital, and in the process, grew its share count by 24.2% over the last five years. This has resulted in muted earnings per share growth but doesn’t tell us as much about its future. We prefer to look at operating and free cash flow margins in these situations.

In Q1, Concentrix reported EPS at $2.79, up from $2.57 in the same quarter last year. This print beat analysts’ estimates by 7.8%. Over the next 12 months, Wall Street expects Concentrix’s full-year EPS of $11.61 to grow 2.2%.

Key Takeaways from Concentrix’s Q1 Results

We enjoyed seeing Concentrix beat analysts’ EPS and EBITDA expectations this quarter. We were also glad it slightly lifted its revenue guidance for next quarter. Overall, this quarter had some key positives. The stock traded up 8.2% to $49.45 immediately following the results.

Sure, Concentrix had a solid quarter, but if we look at the bigger picture, is this stock a buy? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.