Shareholders of Insight Enterprises would probably like to forget the past six months even happened. The stock dropped 39.4% and now trades at $83.67. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Insight Enterprises, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free for active Edge members.

Why Do We Think Insight Enterprises Will Underperform?

Even with the cheaper entry price, we don't have much confidence in Insight Enterprises. Here are three reasons why NSIT doesn't excite us and a stock we'd rather own.

1. Long-Term Revenue Growth Flatter Than a Pancake

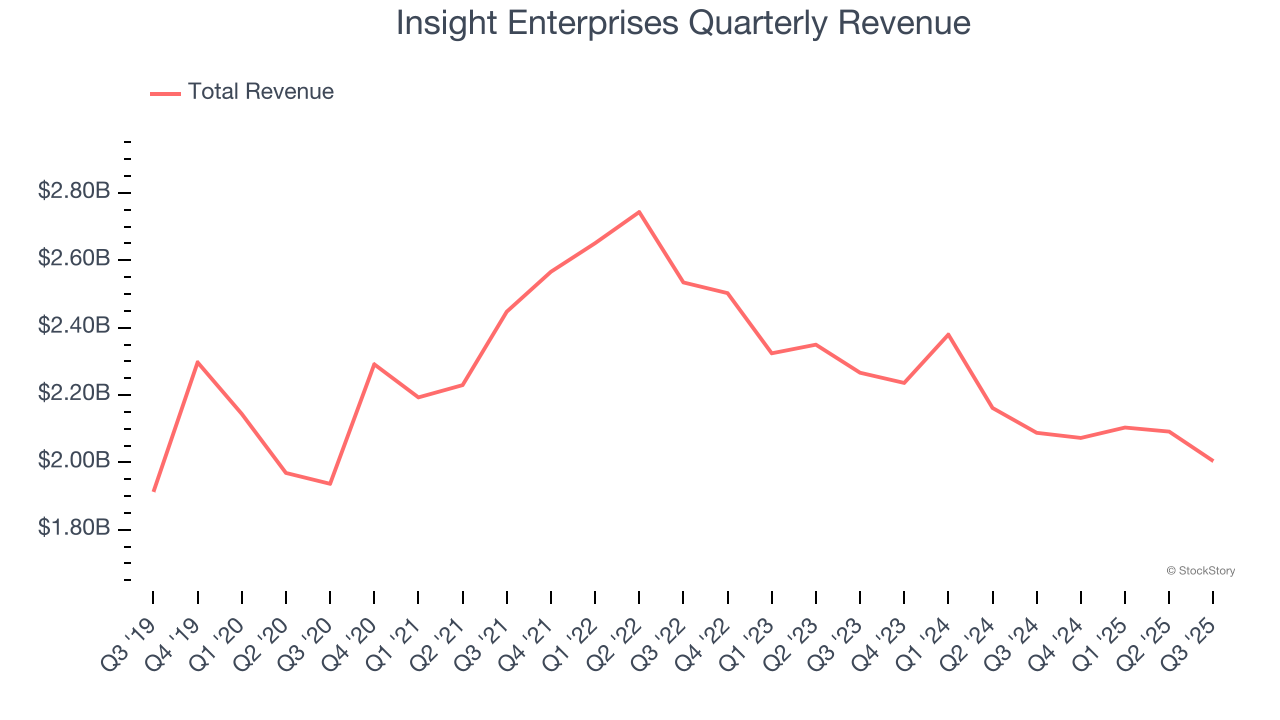

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Insight Enterprises struggled to consistently increase demand as its $8.27 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and is a sign of poor business quality.

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Insight Enterprises’s revenue to stall. While this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

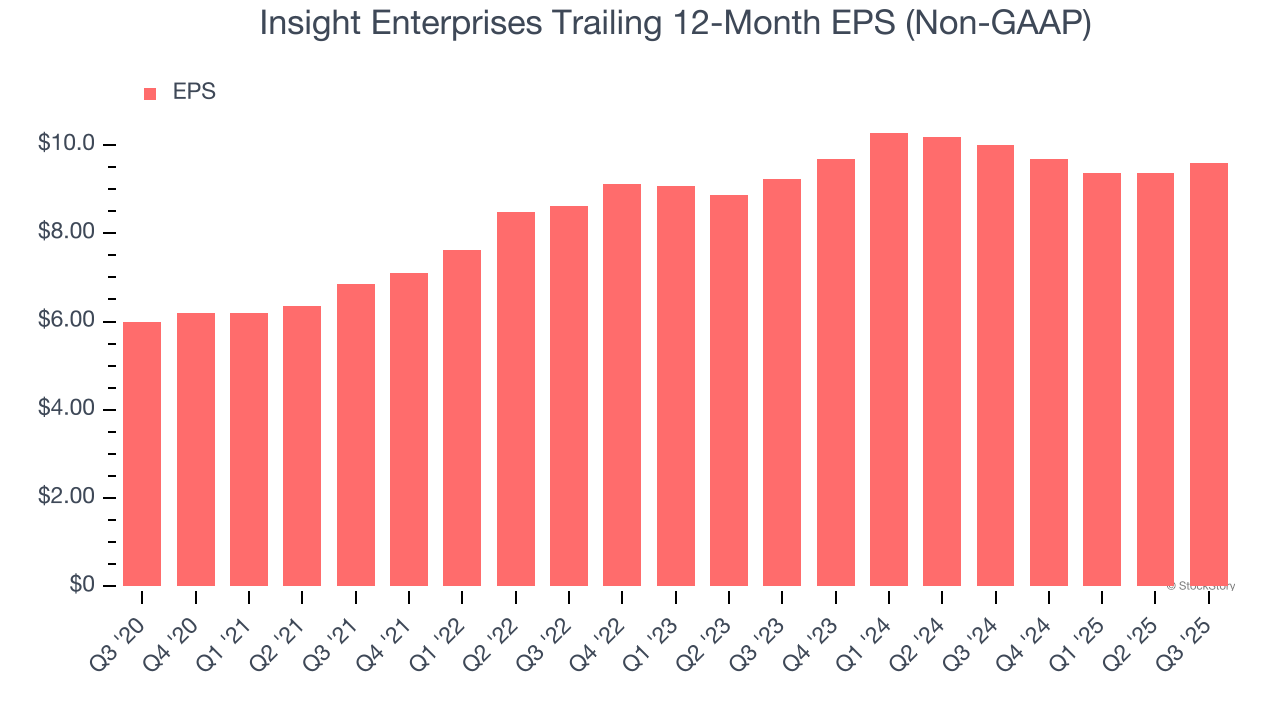

3. Recent EPS Growth Below Our Standards

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Insight Enterprises’s EPS grew at a weak 1.9% compounded annual growth rate over the last two years. On the bright side, this performance was higher than its 6.4% annualized revenue declines and tells us management adapted its cost structure in response to a challenging demand environment.

Final Judgment

We cheer for all companies making their customers lives easier, but in the case of Insight Enterprises, we’ll be cheering from the sidelines. Following the recent decline, the stock trades at 8.3× forward P/E (or $83.67 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere. Let us point you toward the most entrenched endpoint security platform on the market.

High-Quality Stocks for All Market Conditions

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.