Shareholders of GEO Group would probably like to forget the past six months even happened. The stock dropped 31.5% and now trades at $17.05. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in GEO Group, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members.

Why Do We Think GEO Group Will Underperform?

Even with the cheaper entry price, we don't have much confidence in GEO Group. Here are three reasons there are better opportunities than GEO and a stock we'd rather own.

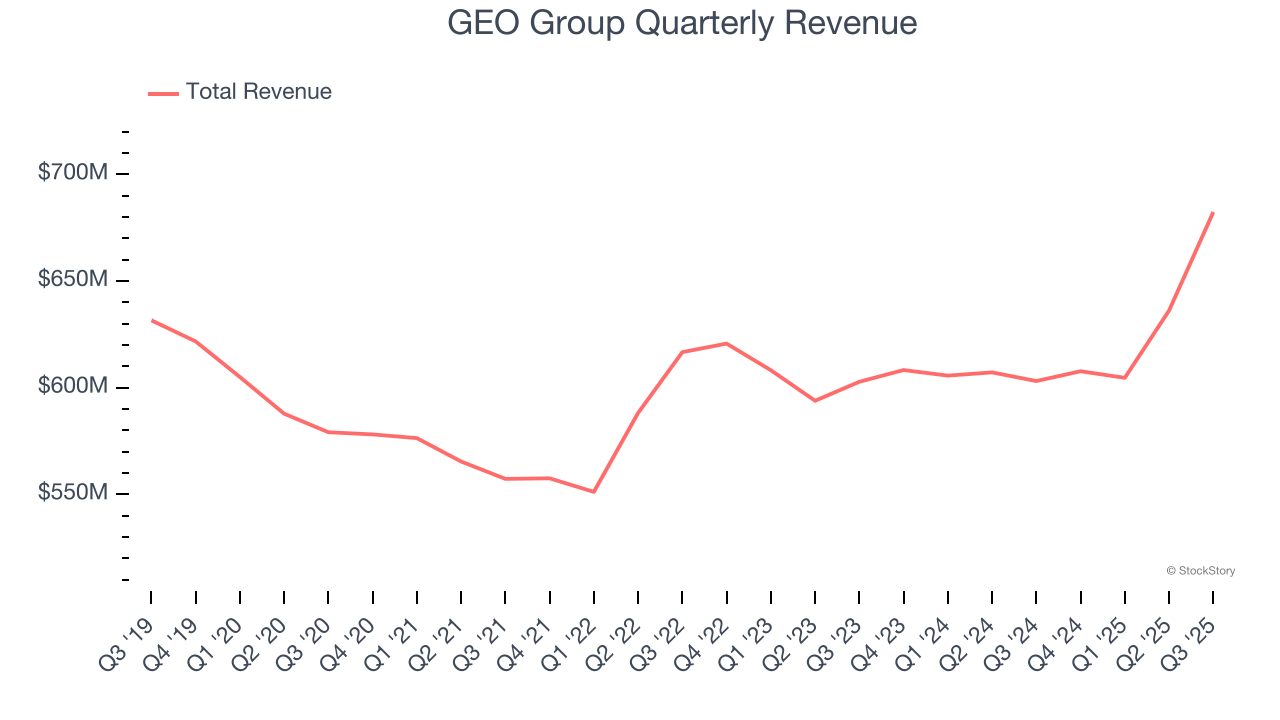

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, GEO Group grew its sales at a sluggish 1.1% compounded annual growth rate. This fell short of our benchmarks.

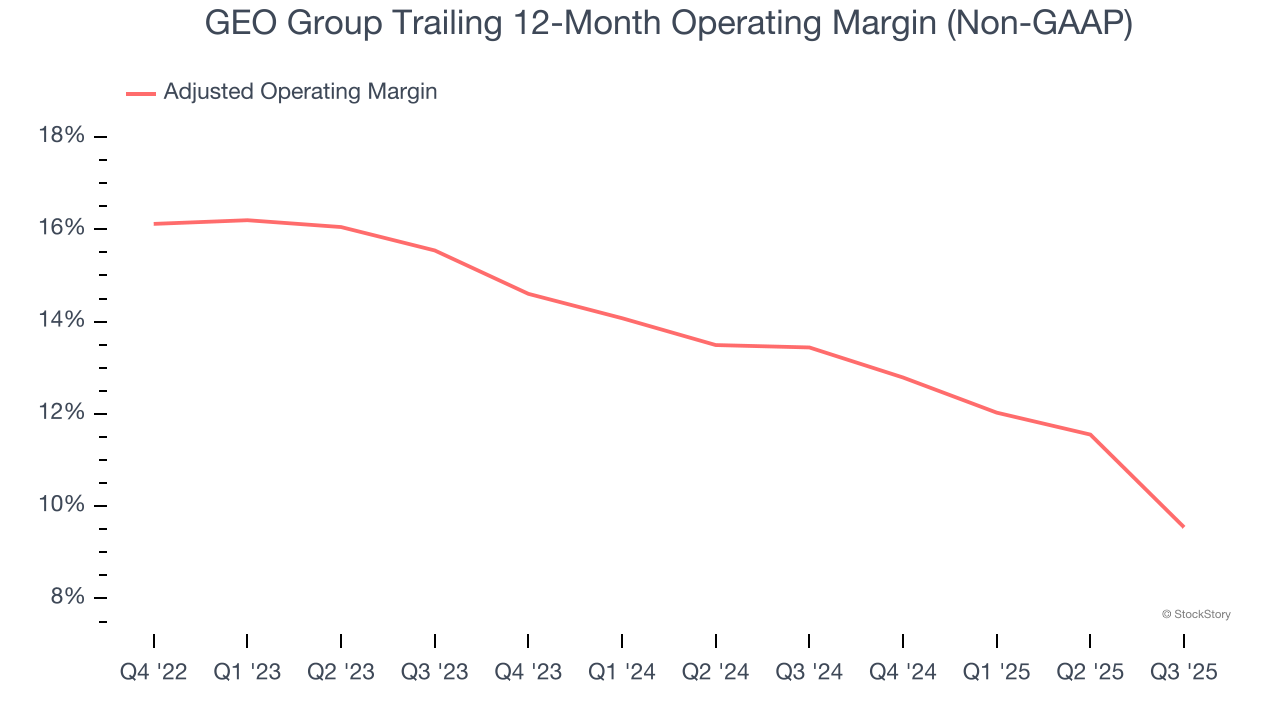

2. Shrinking Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

Looking at the trend in its profitability, GEO Group’s adjusted operating margin decreased by 6.6 percentage points over the last four years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its adjusted operating margin for the trailing 12 months was 9.5%.

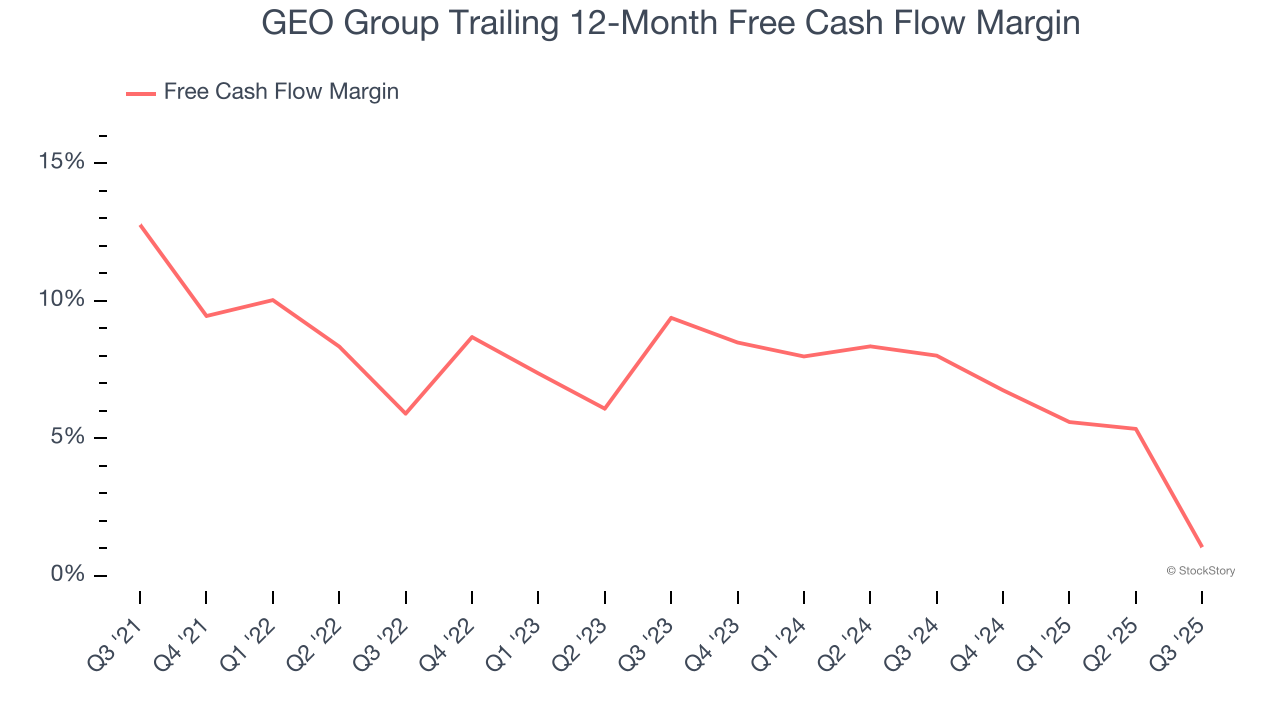

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, GEO Group’s margin dropped by 11.7 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. GEO Group’s free cash flow margin for the trailing 12 months was 1%.

Final Judgment

GEO Group doesn’t pass our quality test. Following the recent decline, the stock trades at 14.8× forward P/E (or $17.05 per share). This valuation tells us a lot of optimism is priced in - we think other companies feature superior fundamentals at the moment. We’d suggest looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

High-Quality Stocks for All Market Conditions

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.