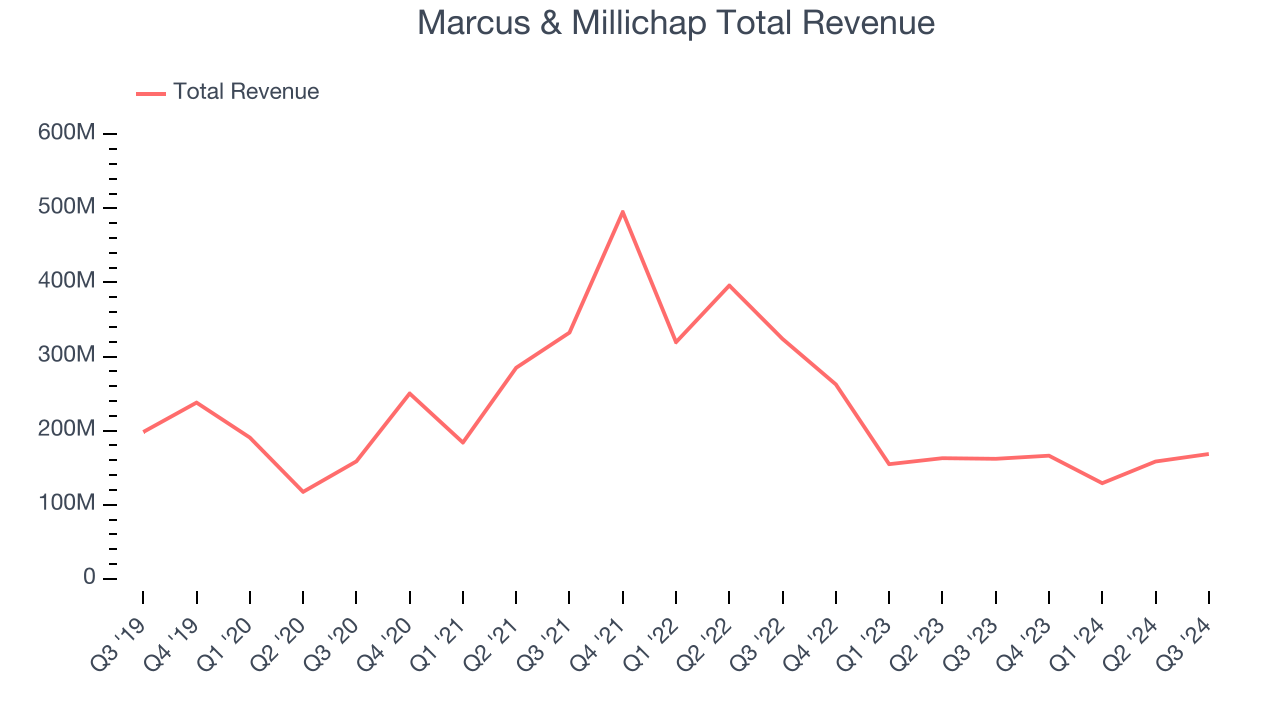

Real estate brokerage and services firm Marcus & Millichap (NYSE: MMI) reported Q3 CY2024 results exceeding the market’s revenue expectations, with sales up 4% year on year to $168.5 million. Its GAAP loss of $0.14 per share was also 26.3% above analysts’ consensus estimates.

Is now the time to buy Marcus & Millichap? Find out by accessing our full research report, it’s free.

Marcus & Millichap (MMI) Q3 CY2024 Highlights:

- Revenue: $168.5 million vs analyst estimates of $160.9 million (4.7% beat)

- EPS: -$0.14 vs analyst estimates of -$0.19 (26.3% beat)

- EBITDA: -$21,000 vs analyst estimates of -$9.8 million (99.8% beat)

- Gross Margin (GAAP): 37.8%, up from 35.4% in the same quarter last year

- Operating Margin: -6.8%, up from -9.5% in the same quarter last year

- EBITDA Margin: 0%, up from -4.1% in the same quarter last year

- Market Capitalization: $1.56 billion

Company Overview

Founded in 1971, Marcus & Millichap (NYSE: MMI) specializes in commercial real estate investment sales, financing, research, and advisory services.

Real Estate Services

Technology has been a double-edged sword in real estate services. On the one hand, internet listings are effective at disseminating information far and wide, casting a wide net for buyers and sellers to increase the chances of transactions. On the other hand, digitization in the real estate market could potentially disintermediate key players like agents who use information asymmetries to their advantage.

Sales Growth

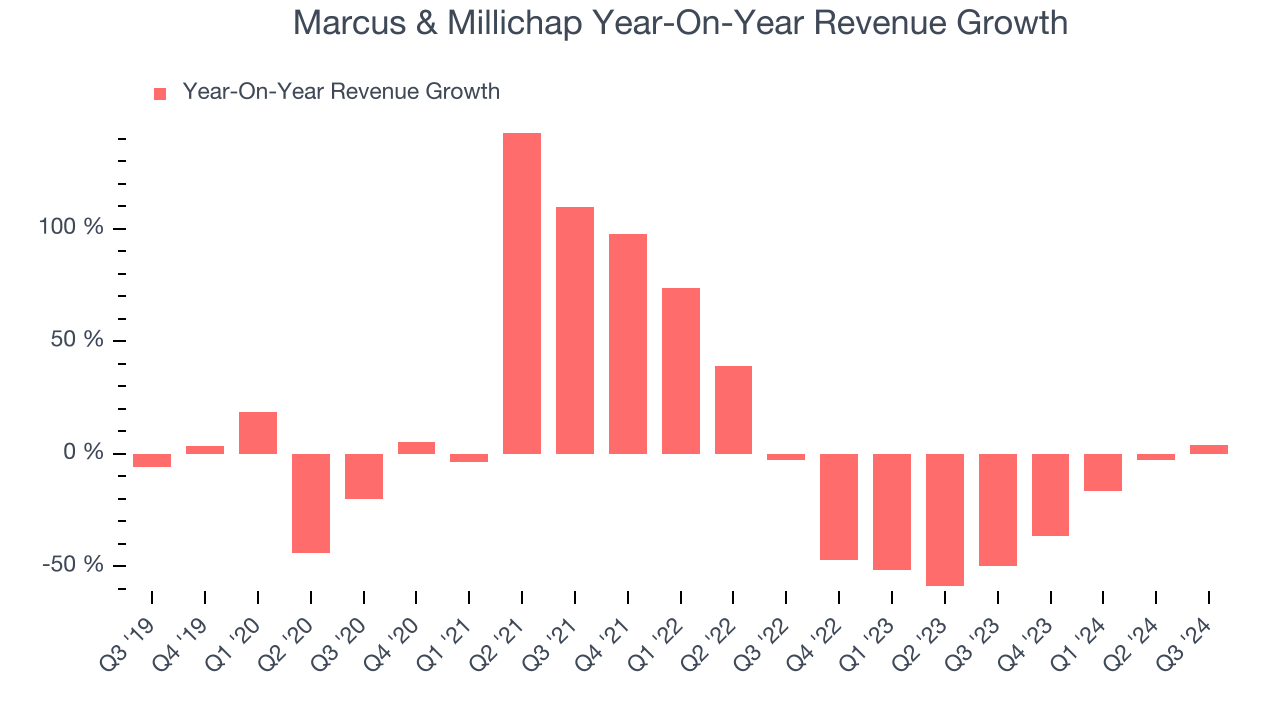

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Marcus & Millichap’s demand was weak over the last five years as its sales fell by 4.9% annually, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. Marcus & Millichap’s recent history shows its demand has stayed suppressed as its revenue has declined by 36.3% annually over the last two years.

This quarter, Marcus & Millichap reported modest year-on-year revenue growth of 4% but beat Wall Street’s estimates by 4.7%.

Looking ahead, sell-side analysts expect revenue to grow 21% over the next 12 months, an improvement versus the last two years. This projection is healthy and indicates the market thinks its newer products and services will fuel higher growth rates.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

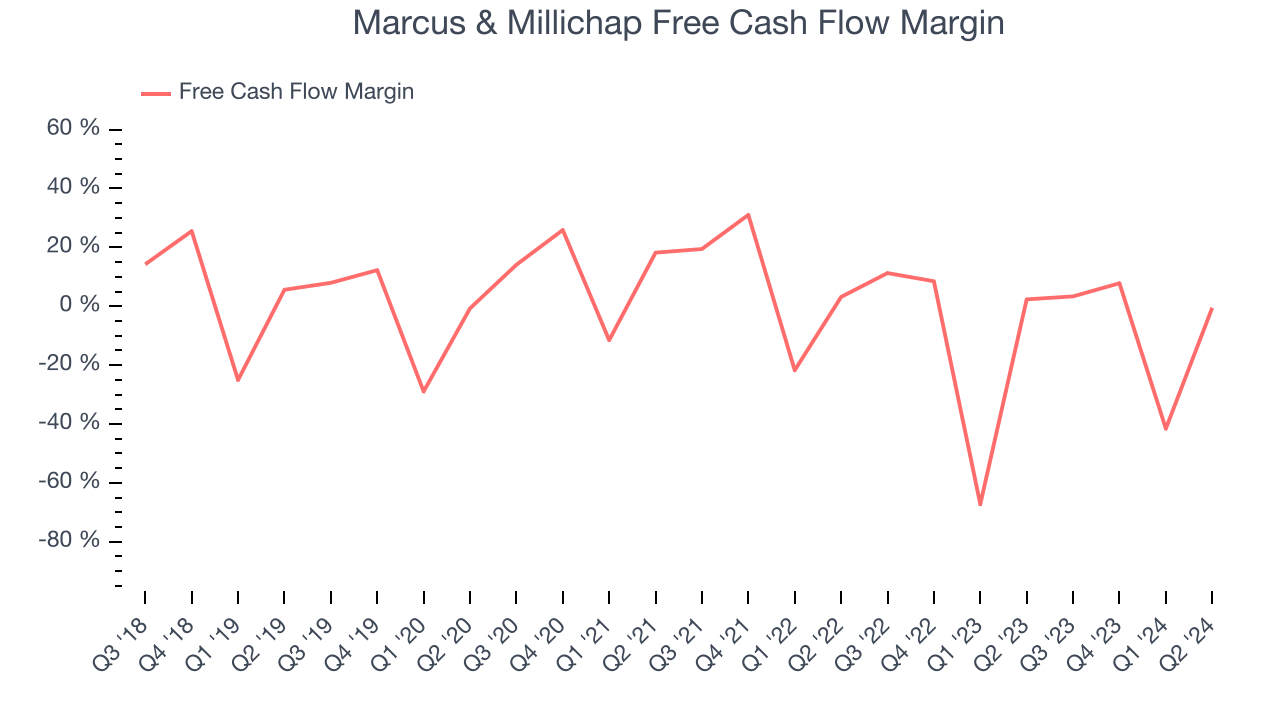

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Over the last two years, Marcus & Millichap’s demanding reinvestments to stay relevant have drained its resources. Its free cash flow margin averaged negative 9.5%, meaning it lit $9.53 of cash on fire for every $100 in revenue.

Key Takeaways from Marcus & Millichap’s Q3 Results

We were impressed by how significantly Marcus & Millichap blew past analysts’ revenue, EBITDA, and EPS expectations in this solid quarter. The stock remained flat at $40.18 immediately after reporting.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.