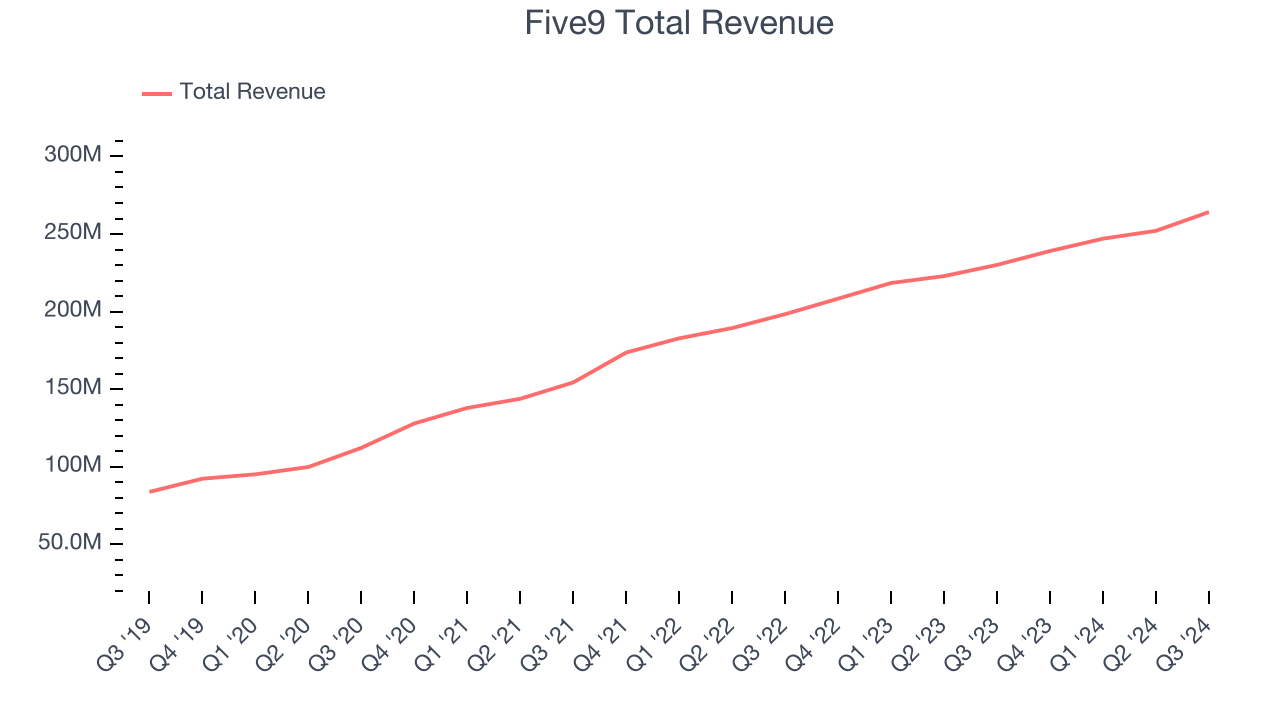

Call center software provider Five9 (NASDAQ: FIVN) reported revenue ahead of Wall Street’s expectations in Q3 CY2024, with sales up 14.8% year on year to $264.2 million. Guidance for next quarter’s revenue was optimistic at $267.5 million at the midpoint, 2.4% above analysts’ estimates. Its non-GAAP profit of $0.67 per share was also 15.1% above analysts’ consensus estimates.

Is now the time to buy Five9? Find out by accessing our full research report, it’s free.

Five9 (FIVN) Q3 CY2024 Highlights:

- Revenue: $264.2 million vs analyst estimates of $255.1 million (3.6% beat)

- Adjusted EPS: $0.67 vs analyst estimates of $0.58 (15.1% beat)

- EBITDA: $52.36 million vs analyst estimates of $46.74 million (12% beat)

- Revenue Guidance for Q4 CY2024 is $267.5 million at the midpoint, above analyst estimates of $261.3 million

- Adjusted EPS guidance for the full year is $2.37 at the midpoint, beating analyst estimates by 4.6%

- Gross Margin (GAAP): 53.8%, up from 51.7% in the same quarter last year

- Operating Margin: -5.8%, up from -11.2% in the same quarter last year

- EBITDA Margin: 19.8%, up from 17.9% in the same quarter last year

- Free Cash Flow Margin: 7.9%, up from 3.2% in the previous quarter

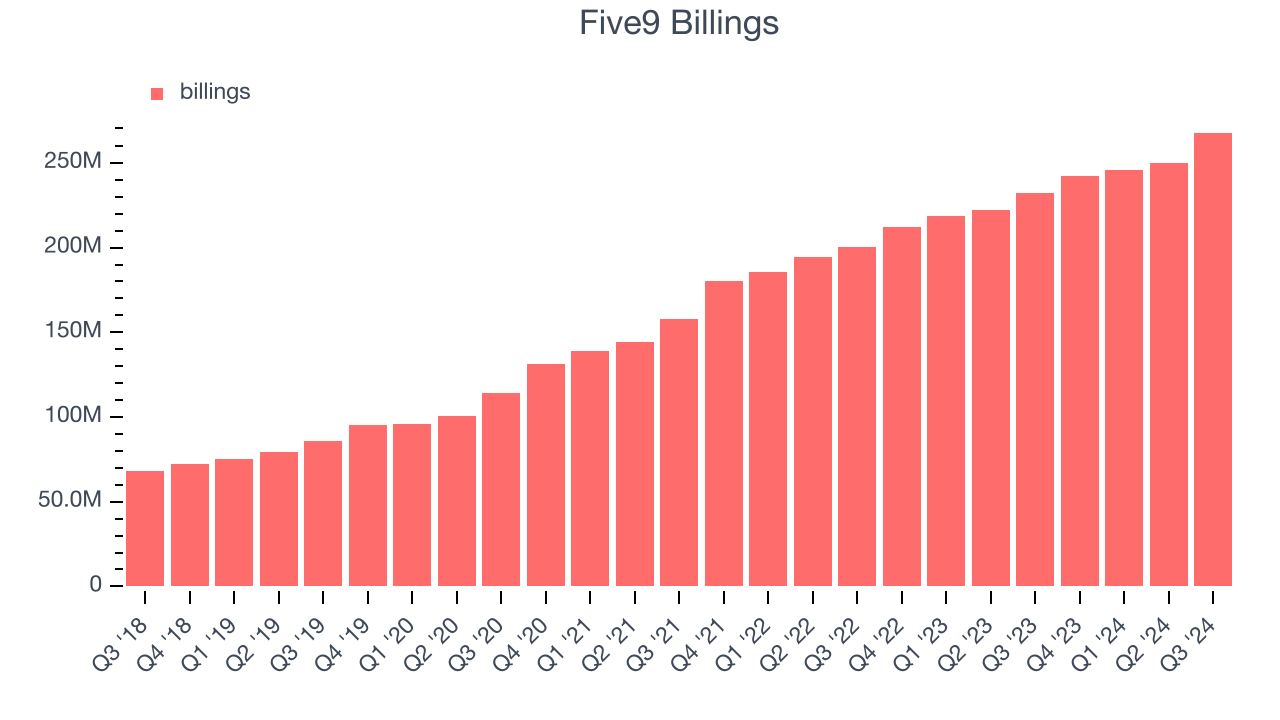

- Billings: $267.9 million at quarter end, up 15.3% year on year

- Market Capitalization: $2.35 billion

“We are very pleased to report strong third quarter results, which exceeded our guidance across all key metrics. Subscription revenue grew 20% year-over-year, and we achieved an adjusted EBITDA margin of 20%, helping drive robust operating cash flow of $41 million. With the acceleration of AI, CX is at an inflection point. We believe our AI-powered platform is at the forefront of enabling a hyper-personalized experience, continuous engagement, and seamless customer journeys, all while creating a pathway for durable growth.” - Mike Burkland, Chairman and CEO, Five9.

Company Overview

Started in 2001, Five9 (NASDAQ: FIVN) offers software as a service that makes it easier for companies to set up and efficiently run call centers, and offer more tailored customer support.

Video Conferencing

Work is becoming more distributed, both across geographies and devices. In order for businesses to keep functioning efficiently, they need to be able to communicate as well as they did when the teams were co-located, which drives the demand for integrated communication platforms.

Sales Growth

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Luckily, Five9’s sales grew at a decent 21.1% compounded annual growth rate over the last three years. This is a useful starting point for our analysis.

This quarter, Five9 reported year-on-year revenue growth of 14.8%, and its $264.2 million of revenue exceeded Wall Street’s estimates by 3.6%. Management is currently guiding for a 11.9% year-on-year increase next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9.4% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and indicates the market believes its products and services will face some demand challenges.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Billings

In addition to revenue, billings is a non-GAAP metric that sheds additional light on Five9’s business quality. Billings is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Over the last year, Five9’s billings growth has slightly outpaced the sector, averaging 13.7% year-on-year increases and punching in at $267.9 million in the latest quarter. This performance was in line with its revenue growthand shows the company is successfully converting sales into cash. Its growth also enhances liquidity and provides a solid foundation for future investments.

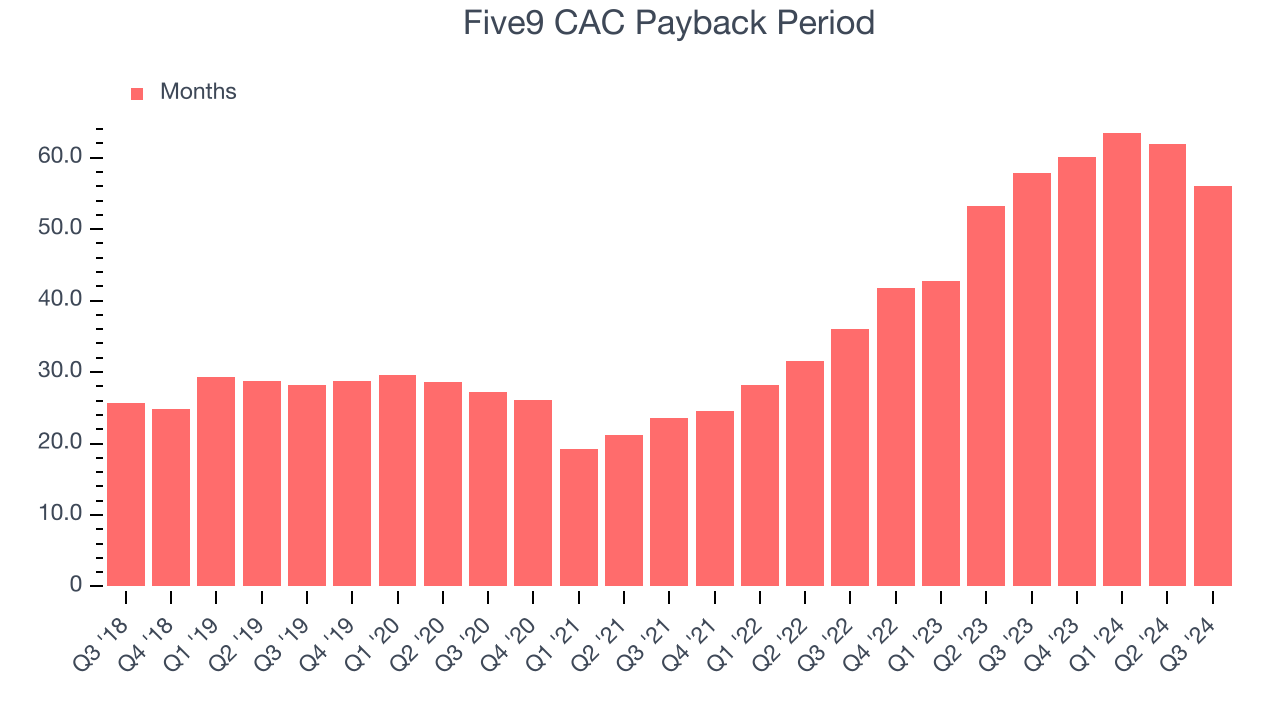

Customer Acquisition Efficiency

Customer acquisition cost (CAC) payback represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for marketing and sales investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

It’s relatively expensive for Five9 to acquire new customers as its CAC payback period checked in at 56.1 months this quarter. The company’s performance indicates that it operates in a competitive market and must continue investing to maintain its growth trajectory.

Key Takeaways from Five9’s Q3 Results

We were impressed by how significantly Five9 blew past analysts’ EBITDA expectations this quarter. We were also glad its full-year EPS guidance exceeded Wall Street’s estimates. Zooming out, we think this was a solid quarter. The stock traded up 23.3% to $40.47 immediately following the results.

Indeed, Five9 had a rock-solid quarterly earnings result, but is this stock a good investment here? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.