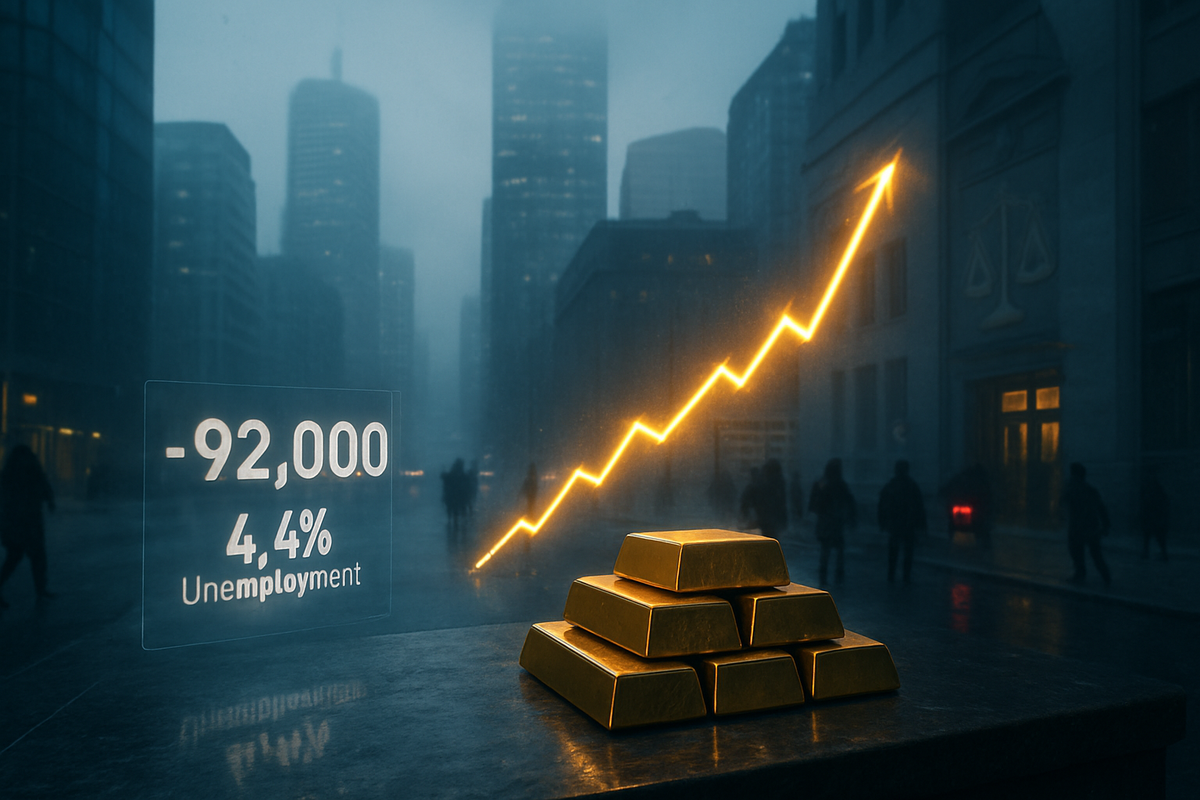

The United States economy was sent into a tailspin this past week following the release of a devastating February jobs report that has shattered the prevailing "soft landing" narrative. On March 6, 2026, the Bureau of Labor Statistics revealed an unexpected contraction of 92,000 jobs, a stark reversal from economist projections of a 50,000-job gain. This sudden cooling of the labor market pushed the national unemployment rate up to 4.4%, its highest level in years, signaling a significant shift in the economic landscape as of March 9, 2026.

The immediate market reaction was a frantic "flight to safety," catapulting spot gold prices to a historic peak of $5,174.59 per ounce as investors initially bet on aggressive interest rate cuts from the Federal Reserve. However, the optimism for a quick policy pivot has been swiftly tempered by "stagflation" concerns. Despite the job losses, wage growth remains stubbornly high and energy prices are surging, leaving the Federal Reserve trapped between a weakening economy and persistent inflationary pressures.

A "February Freeze" Shatters Economic Optimism

The labor data released on Friday, March 6, has been dubbed the "February Freeze" by Wall Street analysts. The loss of 92,000 positions represents the sharpest monthly decline since the early post-pandemic era. The weakness was surprisingly broad-based, with the Healthcare sector losing 28,000 jobs—exacerbated by a massive strike of mental health workers at Kaiser Permanente—and the Manufacturing sector shedding 12,000 positions. Even the historically resilient Information and Leisure sectors saw declines ranging from 11,000 to 27,000 jobs.

This timeline of deterioration began in late 2025, but the February data acted as the catalyst for a major market repricing. Leading up to the report, the Federal Reserve, led by Chair Jerome Powell, had maintained a cautious stance, but the sudden jump in the unemployment rate to 4.4% has forced a re-evaluation of the entire fiscal outlook. Initial reactions on Friday saw the S&P 500 (NYSEARCA: SPY) drop by 1.6% in a matter of hours as the reality of a contracting labor market set in.

Winners and Losers in the Wake of the Jobs Shock

In the current environment of high volatility, a clear divide has emerged between the beneficiaries of economic uncertainty and those tethered to growth. The primary winners have been precious metal producers. Newmont (NYSE: NEM), Agnico Eagle Mines (NYSE: AEM), and Barrick Gold (NYSE: GOLD) have seen their stock prices surge alongside the record-breaking gold rally. Newmont, in particular, reported record free cash flow as the price of bullion crossed the $5,100 threshold, making it a standout performer on the S&P 500.

Conversely, the technology and banking sectors are facing significant headwinds. NVIDIA (NASDAQ: NVDA) saw shares slide 3.2% following the report, as investors feared that a broader economic slowdown would lead to reduced capital expenditures on AI infrastructure. Similarly, Apple (NASDAQ: AAPL) has come under pressure as rising unemployment threatens consumer purchasing power, particularly for high-end electronics. In the financial sector, JPMorgan Chase (NYSE: JPM) and other major lenders are grappling with a flattening yield curve and the increased risk of loan defaults as the labor market softens.

The Stagflation Trap: Rising Wages and Energy Spikes

The current crisis is not a typical recessionary threat; it is increasingly looking like a return of "stagflation." While job losses are mounting, wage growth has remained unexpectedly resilient, with average hourly earnings growing at an annualized rate of 4.5%. This creates a nightmare scenario for the Federal Reserve: they cannot easily cut rates to stimulate the job market without risking a "wage-price spiral" that would further entrench inflation.

This situation is further complicated by geopolitical instability in the Middle East, which has pushed oil prices (WTI) above $110 per barrel. This "energy tax" on households is dampening growth while keeping the Consumer Price Index (CPI) elevated. Federal Reserve Governor Christopher Waller recently noted that these twin pressures—rising energy costs and a cooling labor market—act as a pincer movement on the U.S. consumer. This mirrors historical precedents from the 1970s, where traditional monetary tools became less effective against cost-push inflation.

The Road Ahead: A Critical March Meeting

As we look toward the next two weeks, all eyes are on the Federal Open Market Committee (FOMC) meeting scheduled for March 17–18. The market is currently divided on what the Fed will do. Before the jobs report, a "hold" was the consensus; immediately after the -92,000 figure, futures markets briefly priced in a 50-basis-point cut. However, as of March 9, that probability has faded as stagflation fears take hold.

The short-term outlook suggests the Fed may be forced to maintain current interest rates to combat inflation, even if it means allowing the unemployment rate to drift higher toward 4.6% or 4.7%. Investors should prepare for continued volatility in "long-duration" assets like tech stocks and keep a close watch on the U.S. Dollar Index (DXY), which has shown signs of weakening as central banks in emerging markets pivot toward gold reserves.

Assessing the Market Moving Forward

The February 2026 jobs report marks a definitive turning point for the markets. The "Goldilocks" era of moderate growth and falling inflation appears to be over, replaced by a more complex and dangerous environment where traditional economic correlations are breaking down. The record gold price of $5,174.59 is not just a milestone; it is a signal that institutional investors are hedging against a systemic shift in the global economy.

For investors, the key takeaways are clear: diversification into defensive assets and commodities is becoming a necessity rather than a luxury. While the headline job loss of 92,000 is alarming, the real story is the Fed's dwindling list of options. In the coming months, the focus will shift from "when will they cut?" to "can they cut at all?" Monitoring wage growth and oil prices will be just as critical as tracking unemployment numbers in the volatile quarter ahead.

This content is intended for informational purposes only and is not financial advice