As 2025 draws to a close, the global mining sector is basking in the glow of a historic bull market that has defied conventional economic gravity. Driven by a rare alignment of geopolitical volatility, aggressive central bank accumulation, and a structural supply deficit in industrial metals, precious metals have reached levels previously dismissed as hyperbolic. For investors, this "Gilded Age" of mining has translated into massive gains for industry leaders who spent the last two years lean-manufacturing their portfolios for this exact moment.

The immediate implications are profound: major miners are sitting on record-breaking free cash flow, allowing for aggressive debt reduction and the return of significant capital to shareholders. However, the rally has also sparked a frantic wave of consolidation across the sector, as the cost of "buying" production through mergers and acquisitions has become more attractive than the decade-long slog of "building" new greenfield projects in an increasingly complex regulatory environment.

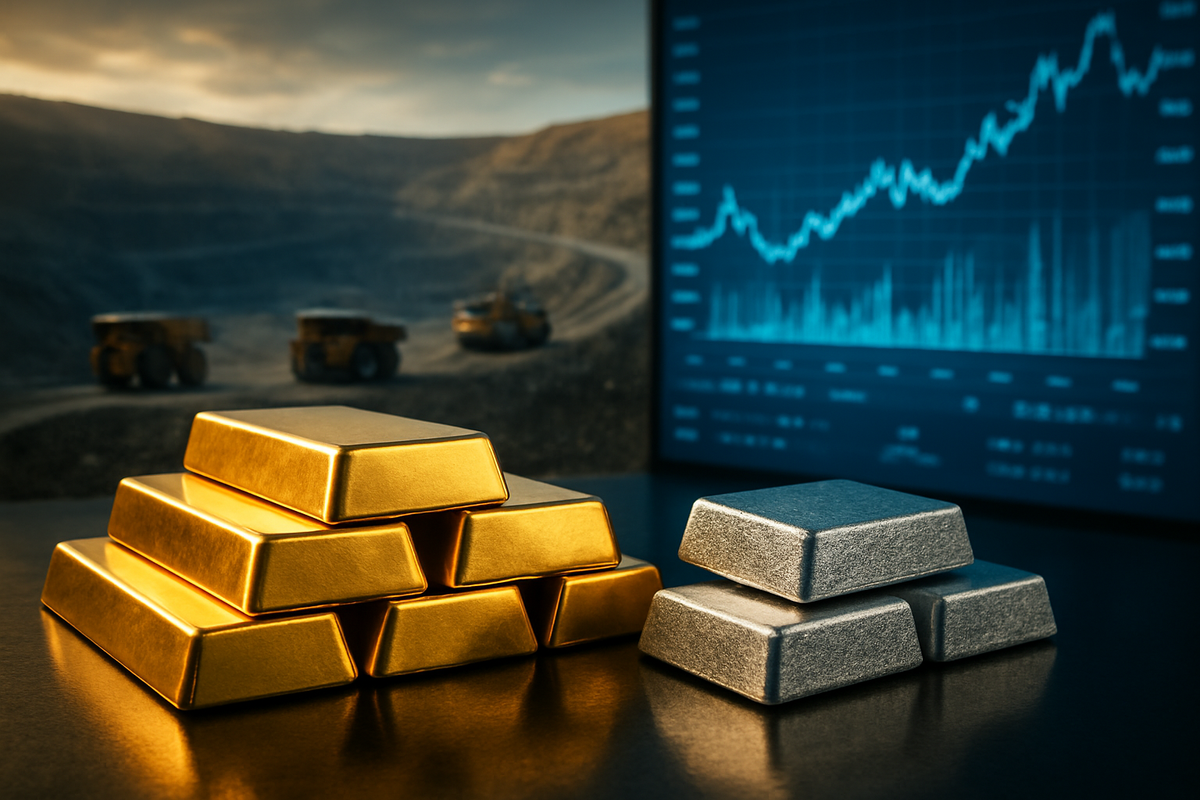

The Path to $4,400 Gold and the Silver Squeeze

The ascent of precious metals in 2025 has been nothing short of parabolic. Gold prices, which began the year with steady momentum, shattered multiple resistance levels to peak near $4,460 per ounce in late December. This represents a staggering 70% annual gain, the metal’s strongest performance since the inflationary shocks of 1979. The timeline leading to this peak was marked by a series of Federal Reserve rate cuts and a persistent "sticky" inflation narrative that forced institutional investors back into hard assets.

Simultaneously, silver has emerged as the year’s ultimate "high-beta" play, outperforming gold with a 135% appreciation. After breaching the psychologically critical $80 per ounce mark in mid-December, silver has stabilized near $75, driven by a "perfect storm" of investment demand and a chronic structural supply deficit. The initial market reaction was one of disbelief, but as central banks in Poland, Brazil, and Kazakhstan continued to report massive monthly bullion additions, the skepticism turned into a "fear of missing out" (FOMO) rally that swept up both retail and institutional desks.

By late 2025, a fundamental shift in the global financial architecture became undeniable. Gold officially surpassed the Euro to become the world’s second-largest reserve asset, trailing only the U.S. Dollar. This "de-dollarization" trend, accelerated by nations seeking assets immune to Western sanctions, has provided a permanent floor for prices, insulating the mining sector from the typical cyclical downturns of the past.

Titans of the Tunnels: Newmont and Hecla Lead the Charge

In this high-price environment, Newmont Corporation (NYSE: NEM) has emerged as the blueprint for corporate efficiency. Throughout 2025, Newmont focused on its "Tier 1" strategy, successfully completing a multi-billion dollar divestiture program. By October, the company had offloaded non-core assets like the Akyem mine in Ghana and the Porcupine mine in Canada, generating over $4.3 billion in gross proceeds. This streamlined focus allowed Newmont to report a staggering $1.6 billion in free cash flow in the third quarter alone—its fourth consecutive quarter exceeding the billion-dollar mark.

While Newmont dominates the gold landscape, Hecla Mining Company (NYSE: HL) has become the primary vehicle for silver exposure. Hecla’s stock has surged approximately 80% year-to-date, buoyed by flawless operational execution at its flagship properties. The Lucky Friday mine in Idaho maintained full-tilt production throughout the year, contributing 1.3 million ounces of silver in Q3. Meanwhile, the Keno Hill project in the Yukon reached a critical milestone, delivering its first positive free cash flow quarters and proving that Hecla can successfully bring high-grade, complex assets online in challenging jurisdictions.

The success of these companies has created a "winner-take-all" dynamic in the sector. While NEM and HL thrive, smaller explorers are struggling to keep pace with rising input costs and labor shortages. Newmont’s impending leadership transition—with Natascha Viljoen set to succeed retiring CEO Tom Palmer in January 2026—is being viewed by the market not as a risk, but as an opportunity to further integrate AI-driven exploration and sustainable energy hubs into their global operations.

Industrial Hunger and the M&A Wave

The wider significance of the 2025 rally extends beyond simple price appreciation; it reflects a fundamental change in how the world values industrial and monetary metals. Silver, in particular, is no longer viewed solely through the lens of jewelry or coins. Despite "thrifting" efforts by solar manufacturers to reduce silver loading in photovoltaic cells, the sheer scale of global solar installations—approaching 1,000 GW—has kept industrial demand at record levels. Furthermore, the explosion of AI data centers and the continued electrification of transport have created a new, price-insensitive buyer for silver and copper.

This demand has triggered a massive wave of industry consolidation. In 2025, M&A activity in the mining sector is projected to surpass $100 billion. Larger players are increasingly choosing to acquire existing production rather than face the 14-year average timeline required to permit and build a new mine. This "buy over build" mentality has led to a flurry of hostile takeovers and strategic mergers, further concentrating power in the hands of the "Big Five" miners.

The regulatory environment is also shifting. As carbon-neutral targets become a "social license" requirement, companies like Newmont are investing heavily in renewable energy to power remote operations. This transition is not just about ESG compliance; it is a strategic hedge against volatile fossil fuel prices. Historical precedents, such as the 2011 gold peak, suggest that such rapid rises often lead to over-leverage, but the 2025 cohort appears more disciplined, using their windfalls to repair balance sheets rather than chasing low-quality ounces.

Looking Ahead: 2026 and the Digital Frontier

As we look toward 2026, the short-term outlook remains bullish, though volatility is expected to increase as the market digests its recent gains. One of the most significant strategic pivots to watch will be the integration of Artificial Intelligence into exploration. Early data from late 2025 suggests that AI-driven exploration has improved discovery success rates by nearly 30%. For companies like Hecla, which recently announced a high-grade gold discovery at its Midas Project using advanced data modeling, this technology could be the key to unlocking "stranded" value in old mining districts.

Potential challenges remain, however. The "Gold Coming Home" trend—where central banks like the Reserve Bank of India repatriate their reserves—could lead to localized liquidity crunches in Western bullion markets. Additionally, if silver prices remain above $75 for an extended period, the pressure on the electronics and solar industries to find substitutes will intensify, potentially creating a "demand cliff" in the late 2020s.

The most likely scenario for the coming year is a period of consolidation where the "quality" of an ounce becomes more important than the quantity. Investors will likely shift their focus from top-line growth to margin preservation, rewarding companies that can keep their All-In Sustaining Costs (AISC) below the industry average despite inflationary pressures on labor and consumables.

A New Benchmark for the Mining Industry

The events of 2025 have fundamentally rebased the mining sector. Gold and silver are no longer just "crisis hedges"; they have become central pillars of a diversifying global financial system and essential components of the green energy transition. The record-breaking performance of Newmont and Hecla Mining underscores the importance of operational discipline and portfolio high-grading in a high-price environment.

Moving forward, the market will be characterized by a "scarcity premium." With few new major discoveries on the horizon and existing mines aging, the companies that control Tier 1 assets will hold immense leverage. For investors, the takeaway is clear: the mining sector has moved from a peripheral "alternative" investment to a core strategic holding.

In the coming months, market participants should closely watch the quarterly production reports from Keno Hill and the progress of Newmont’s new leadership. If these titans can maintain their current margins while navigating the geopolitical shifts of 2026, the current rally may not be a peak, but rather the base of a new, even higher plateau for the precious metals industry.

This content is intended for informational purposes only and is not financial advice.