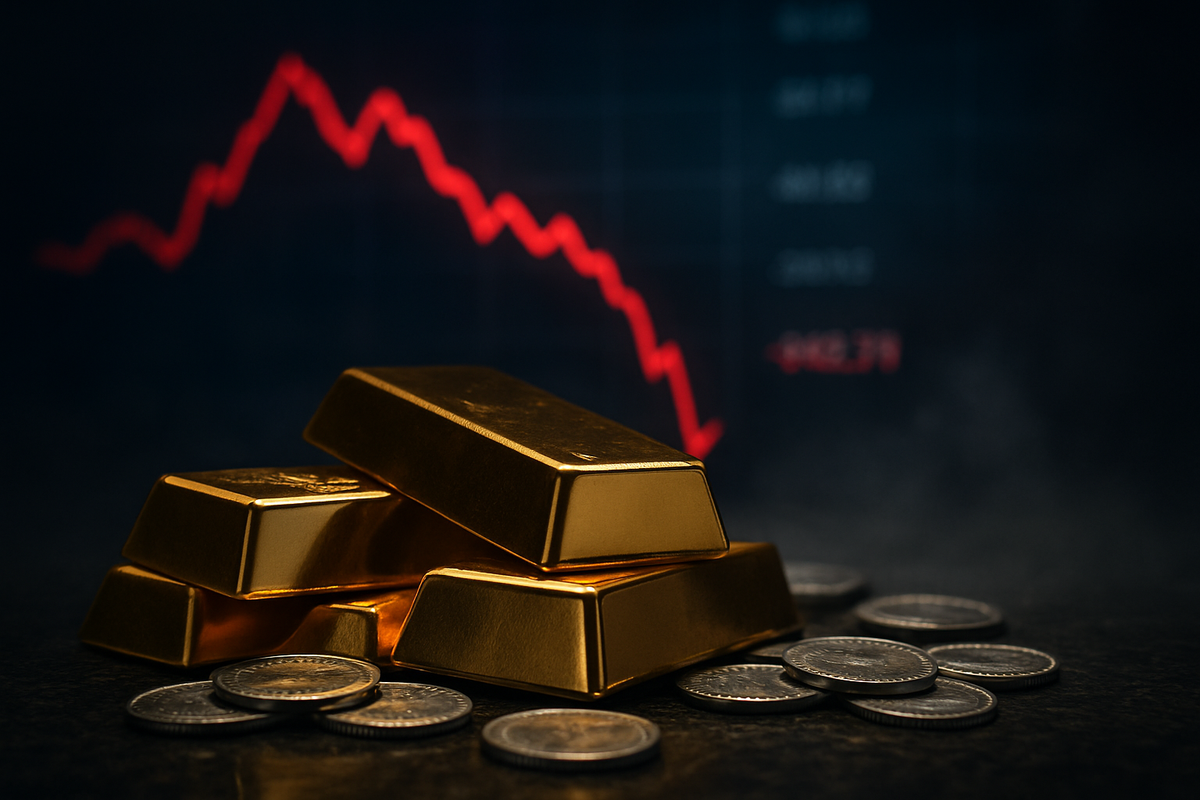

The unprecedented rally that defined the commodities market in 2025 has hit a significant roadblock as the year draws to a close. After reaching breathtaking record highs just days ago, both gold and silver are experiencing a sharp retreat, driven by a wave of aggressive profit-taking and a resurgent U.S. dollar. For a market that spent much of the year in a "parabolic" state, the current pullback represents a sobering moment of reflection for investors who had grown accustomed to daily double-digit gains.

As of December 29, 2025, gold has slipped from its historic peak of $4,565 per ounce, while silver—the year’s standout performer—suffered a dramatic "flash crash" after briefly touching the $84 level. This correction is not merely a technical adjustment; it is a signal that the macroeconomic tailwinds of the past twelve months are shifting. With the Federal Reserve signaling a pause in its easing cycle and a new regulatory landscape for digital safe havens emerging, the precious metals sector is entering 2026 facing a fundamentally different environment than the one it dominated throughout 2025.

A Perfect Storm of Profit-Taking and Policy Shifts

The timeline of this retreat began in earnest on December 26, 2025, when gold (XAU/USD) hit its all-time high of $4,565 per ounce. The surge was the culmination of a year-long flight to safety amid global inflationary pressures and geopolitical tensions. However, the atmosphere changed rapidly on the morning of December 29. Silver (XAG/USD), which had outpaced gold with a 160% year-to-date gain, spiked to an intraday high of $83.62 before tumbling nearly 10% in a matter of hours. The decline was accelerated by the CME Group’s decision to hike margin requirements, a move designed to curb what regulators described as "speculative froth" in the silver pits.

Key stakeholders, including institutional hedge funds and large-scale bullion desks, appear to be the primary drivers of the sell-off. Market data indicates a massive rotation out of long positions as fund managers move to lock in "generational gains" before the year-end reporting deadline. This selling pressure was compounded by a hawkish turn from the Federal Reserve. Although the Fed cut rates to a range of 3.50%–3.75% on December 10, the high level of dissent among board members suggested that the era of "easy money" is reaching its conclusion. This shift has revitalized the U.S. Dollar Index (DXY), which climbed to 98.3, making dollar-denominated metals more expensive for international buyers and further dampening demand.

Mining Giants and the Price of Success

The sudden volatility in spot prices has sent shockwaves through the equities market, particularly for major producers who have enjoyed a banner year. Newmont Corporation (NYSE: NEM), the world’s largest gold miner, saw its shares reach a multi-year high of $102.00 earlier this month. While the company remains highly profitable thanks to its stable All-In Sustaining Costs (AISC), its stock has retreated as investors re-evaluate its valuation. The market is no longer pricing Newmont based on $4,500 gold, but rather a more conservative $4,300 floor, leading to a tactical rotation out of the mining giant.

Similarly, Barrick Gold (NYSE: GOLD) has faced a "repricing" event despite stellar fundamentals. In the third quarter of 2025, Barrick reported a tripling of its free cash flow to $1.5 billion, supported by record prices for both gold and copper. While the company authorized a $1 billion share buyback program in November, the recent retreat in metal prices has stalled its stock's momentum. Conversely, Wheaton Precious Metals (NYSE: WPM) has emerged as a relative winner in terms of resilience. As a streaming and royalty company, Wheaton’s fixed-cost contracts allowed it to capture the silver peak near $80 while its costs remained under $5 per ounce. Although some analysts have downgraded the stock to "Hold" due to "valuation perfection," its business model provides a layer of insulation that pure-play miners lack.

Shifting Sands: The GENIUS Act and Historical Precedents

The current retreat fits into a broader industry trend where traditional safe havens are facing new forms of competition. A critical factor in the late-2025 cooldown is the passage of the GENIUS Act earlier this year. This legislation established a rigorous federal framework for regulated stablecoins, which have begun to siphon off capital that historically would have flowed into physical bullion. By the fourth quarter of 2025, these digital assets became a viable "safe haven" alternative, offering the liquidity of the dollar with the perceived safety of a regulated blockchain, creating a structural headwind for gold and silver.

Historically, this "blow-off top" and subsequent correction mirror the precious metals cycles of the late 1970s and 2011. In both instances, a period of rapid, unsustainable price appreciation was followed by a sharp technical correction as the U.S. dollar stabilized and interest rate expectations shifted. The 2025 retreat is unique, however, because of the speed of the "flash crash" in silver, which highlights the role of high-frequency trading and algorithmic execution in modern commodity markets. This event serves as a reminder that even the most robust bull markets require periods of consolidation to remain healthy in the long term.

The Road to 2026: Pivot or Plunge?

Looking ahead, the market faces two distinct possibilities. In the short term, the primary challenge will be the "digestion" of the 2025 gains. If gold can maintain support at the $4,300 level through the first weeks of January, technical analysts believe the long-term bull case remains intact. However, a breach below that level could trigger a more prolonged correction toward $4,000. Mining companies may need to strategically pivot, focusing on aggressive share buybacks and dividend sustainability to keep shareholders engaged if the era of rapid price appreciation slows down.

Market opportunities may emerge in the "mid-tier" mining space, where companies that were overlooked during the large-cap rally of 2025 may now offer better value. Additionally, the industrial demand for silver—driven by the continued expansion of the green energy sector—is expected to provide a hard floor for prices, regardless of speculative liquidations. The key scenario to watch is the January "rebalancing" period, where institutional investors will decide whether to re-enter the metals market or continue rotating into the strengthening U.S. dollar and the newly regulated digital asset space.

Conclusion: A Necessary Breather for a Record-Breaking Year

The retreat in gold and silver at the end of 2025 marks the end of one of the most remarkable chapters in commodity history. While the sudden drop in prices may be jarring for those who entered the market at the peak, it represents a classic market "reset" driven by profit-taking and a shift in macroeconomic sentiment. The key takeaway for investors is that the fundamental drivers of the 2025 rally—inflationary hedging and geopolitical risk—have not disappeared, but they are now being weighed against a stronger dollar and a more cautious Federal Reserve.

Moving forward, the market will likely trade with heightened volatility as it searches for a new equilibrium. Investors should keep a close eye on the $4,300 support level for gold and the $70 level for silver in the coming months. While the "easy money" of 2025 may be behind us, the underlying strength of the precious metals sector suggests that this retreat is a pause, rather than a permanent reversal, of the long-term trend.

This content is intended for informational purposes only and is not financial advice.