SLB N.V. (SLB), formerly known as Schlumberger Limited, is a leading global oil-field services company that provides technology, drilling, evaluation, well-construction and production systems to upstream oil and gas companies worldwide. The firm is headquartered in Houston, Texas. SLB’s market capitalization stands at $53.9 billion.

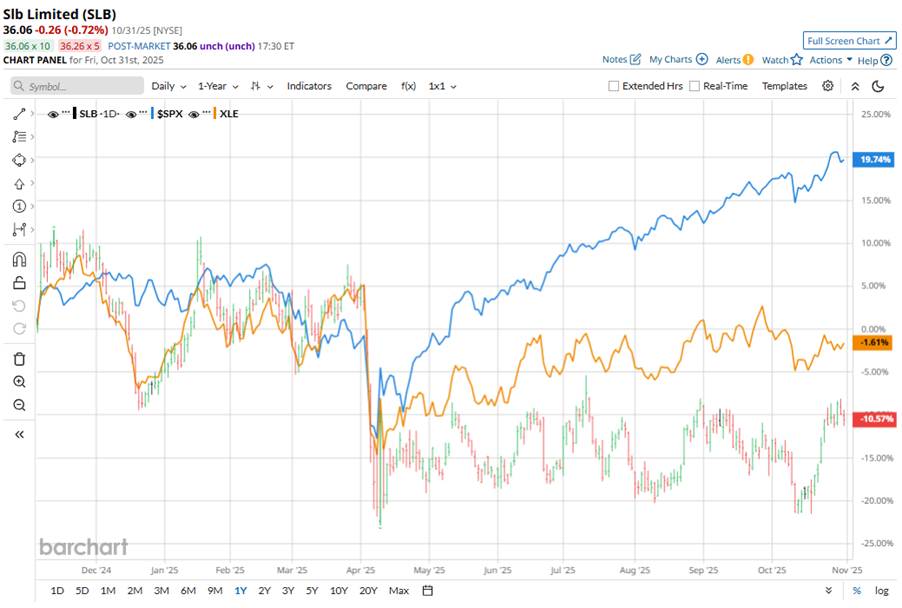

SLB stock has significantly trailed the broader market. The stock has plunged 6% on a year-to-date (YTD) basis and 10.2% over the past 52 weeks, while the S&P 500 Index ($SPX) surged 6.3% in 2025 and gained 17.7% over the past year.

Zooming in further, SLB has also lagged behind the Energy Select Sector SPDR Fund’s (XLE) 2.9% uptick in 2025 and marginal gains over the past 52 weeks.

The company flagged a downturn in upstream spending, particularly in North and Latin America, which weighed heavily on its outlook. More broadly, a still-soft commodity price environment, lingering macroeconomic headwinds, and weak exploration budgets have dampened demand for oil-field services, which is SLB’s core business. These combined factors have contributed to its share price decline despite pockets of business strength.

For the full fiscal 2025, ending in December, analysts expect SLB to deliver an EPS of $2.89, down 15.3% year-over-year. The company has a mixed earnings surprise history. While it missed the Street’s bottom-line estimates once over the past four quarters, it has surpassed the projections on three other occasions.

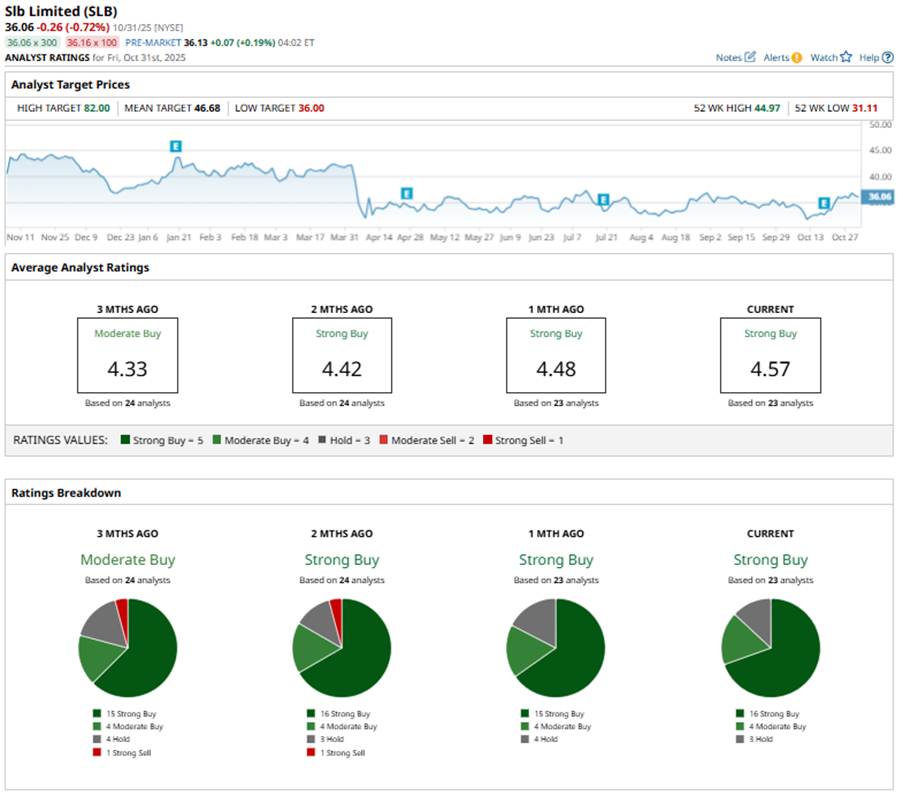

The stock holds a consensus “Strong Buy” rating overall. Of the 23 analysts covering the stock, opinions include 16 “Strong Buys,” four “Moderate Buys,” and three “Holds.”

This configuration is more bullish than three months ago, when the overall rating for the stock was a “Moderate Buy.”

Most recently, Rothschild Redburn initiated coverage on SLB with a “Buy” rating and a $48 price target. It praised SLB’s strategic shift toward less cyclical businesses through the ChampionX acquisition and expects the Production Systems division to outperform consensus forecasts.

SLB’s mean price target of $46.68 represents 29.5% premium to current price levels, while the Street-high target of $82 suggests 127.4% upside potential.

On the date of publication, Sristi Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart