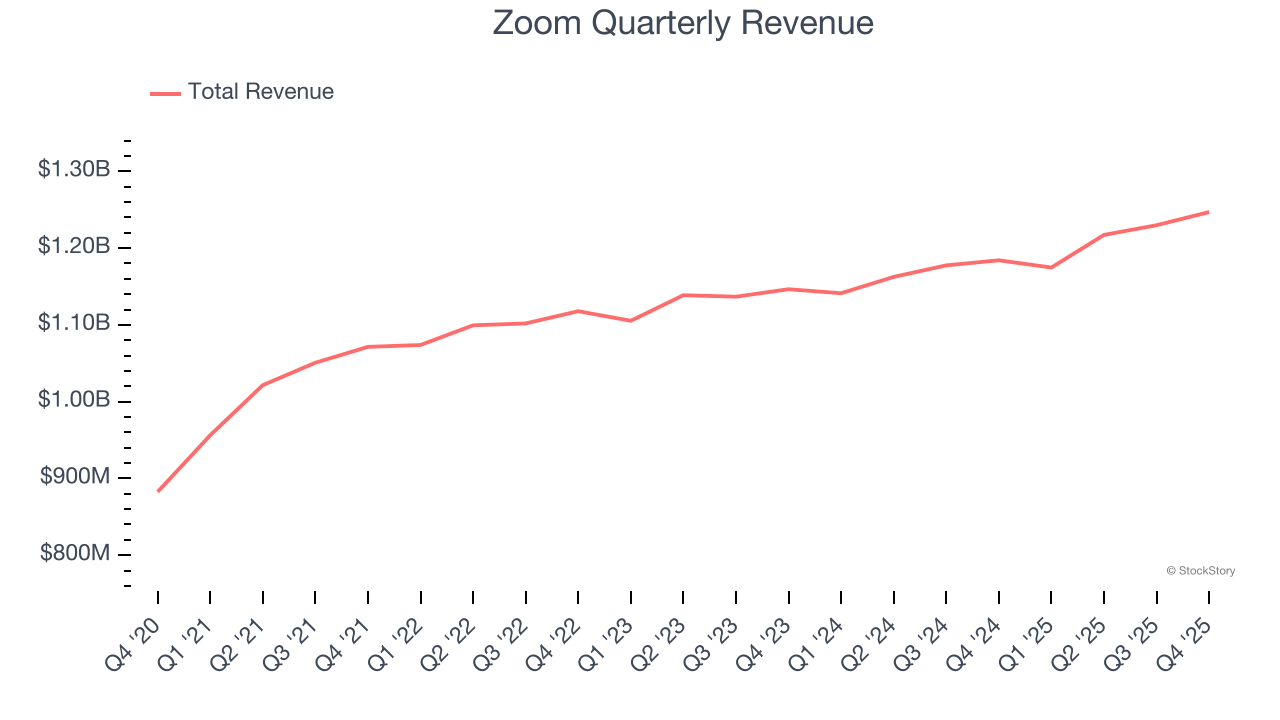

Video communications platform Zoom (NASDAQ: ZM) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 5.3% year on year to $1.25 billion. The company expects next quarter’s revenue to be around $1.22 billion, close to analysts’ estimates. Its non-GAAP profit of $1.44 per share was 3.1% below analysts’ consensus estimates.

Is now the time to buy Zoom? Find out by accessing our full research report, it’s free.

Zoom (ZM) Q4 CY2025 Highlights:

- Revenue: $1.25 billion vs analyst estimates of $1.23 billion (5.3% year-on-year growth, 1.1% beat)

- Adjusted EPS: $1.44 vs analyst expectations of $1.49 (3.1% miss)

- Adjusted Operating Income: $489.7 million vs analyst estimates of $482.1 million (39.3% margin, 1.6% beat)

- Revenue Guidance for Q1 CY2026 is $1.22 billion at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for the upcoming financial year 2027 is $5.79 at the midpoint, missing analyst estimates by 4.5%

- Operating Margin: 20%, up from 19% in the same quarter last year

- Free Cash Flow Margin: 27.1%, down from 50% in the previous quarter

- Customers: 4,468 customers paying more than $100,000 annually

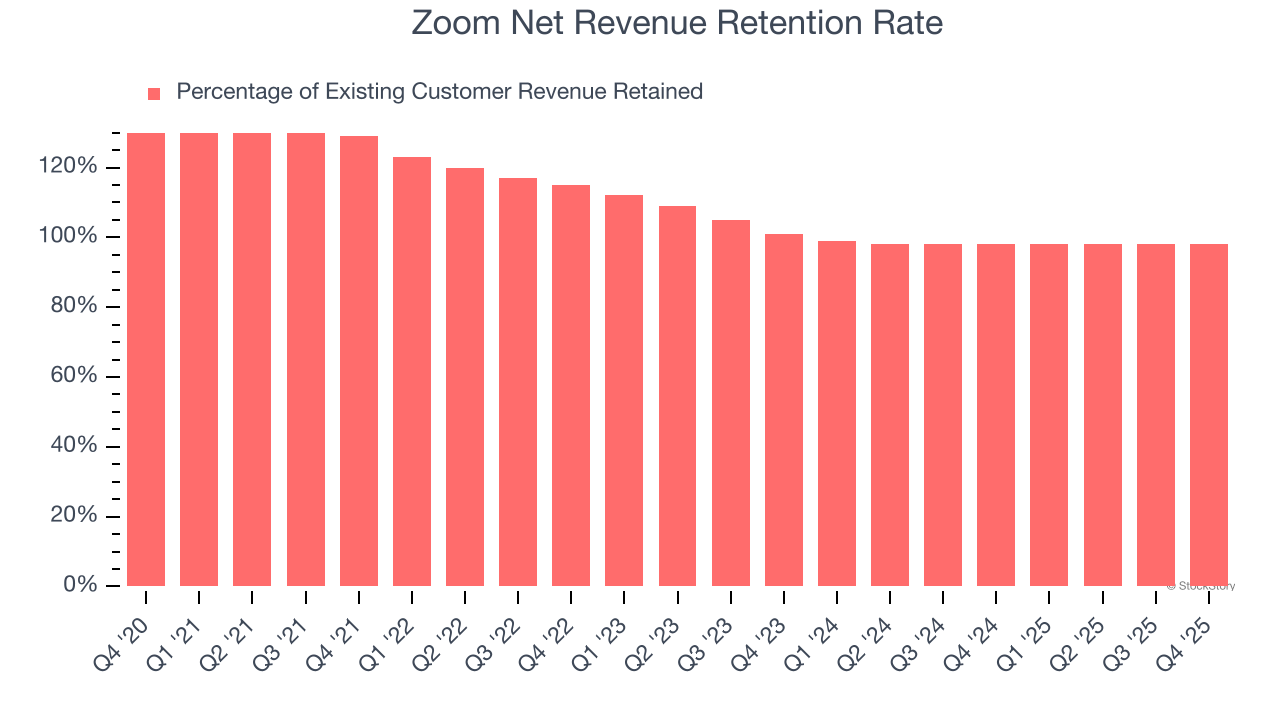

- Net Revenue Retention Rate: 98%, in line with the previous quarter

- Market Capitalization: $25.91 billion

“In FY26, revenue growth accelerated 130 basis points to 4.4%, reflecting the growing adoption of Zoom as a system of action for modern work,” said Eric S. Yuan, Zoom’s founder and CEO.

Company Overview

Once the verb that defined remote work during the pandemic ("let's Zoom later"), Zoom (NASDAQ: ZM) provides a cloud-based platform for video meetings, phone calls, team chat, and collaboration tools that helps businesses and individuals connect virtually.

Revenue Growth

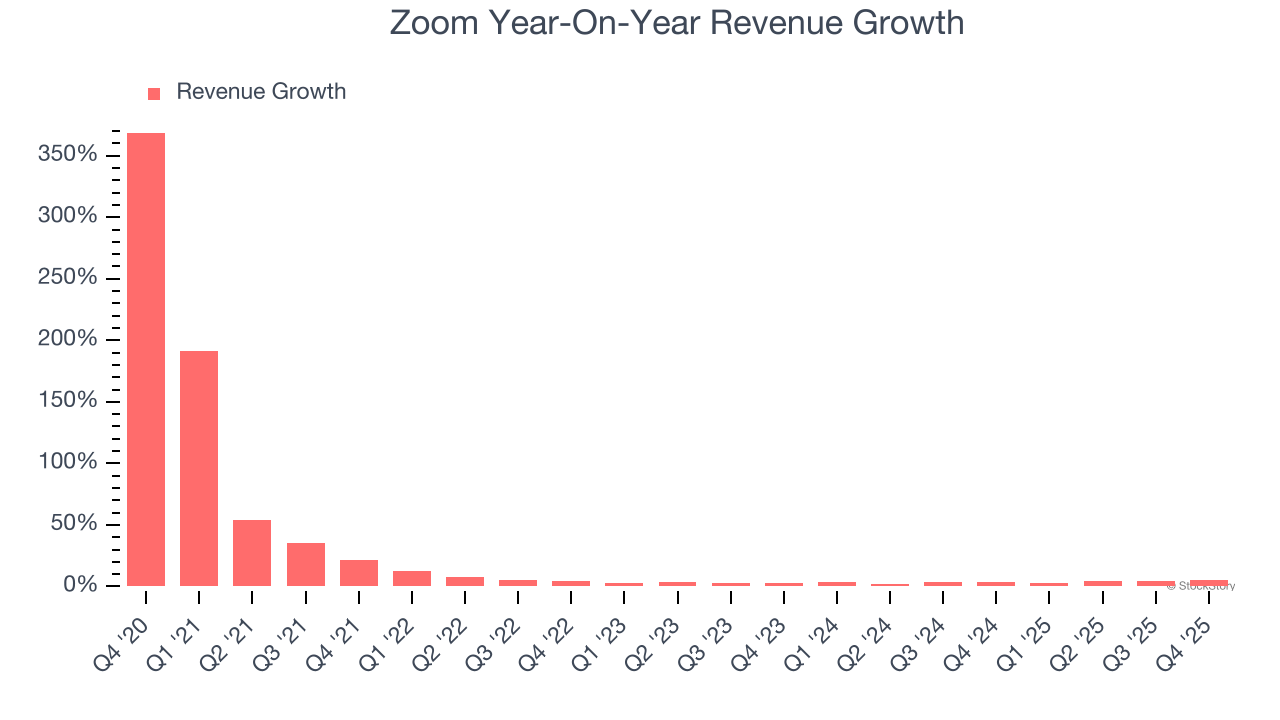

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Zoom grew its sales at a 12.9% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Zoom’s recent performance shows its demand has slowed as its annualized revenue growth of 3.7% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Zoom reported year-on-year revenue growth of 5.3%, and its $1.25 billion of revenue exceeded Wall Street’s estimates by 1.1%. Company management is currently guiding for a 4.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 3.2% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not accelerate its top-line performance yet.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Customer Retention

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Zoom’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 98% in Q4. This means Zoom’s revenue would’ve decreased by 2% over the last 12 months if it didn’t win any new customers.

Zoom has a weak net retention rate, signaling that some customers aren’t satisfied with its products, leading to lost contracts and revenue streams.

Key Takeaways from Zoom’s Q4 Results

We enjoyed seeing Zoom’s optimistic revenue guidance for next year. We were also glad it had many new large contract wins. On the other hand, its full-year EPS guidance missed. Overall, this was a weaker quarter. The stock traded down 3.6% to $84 immediately after reporting.

Big picture, is Zoom a buy here and now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).