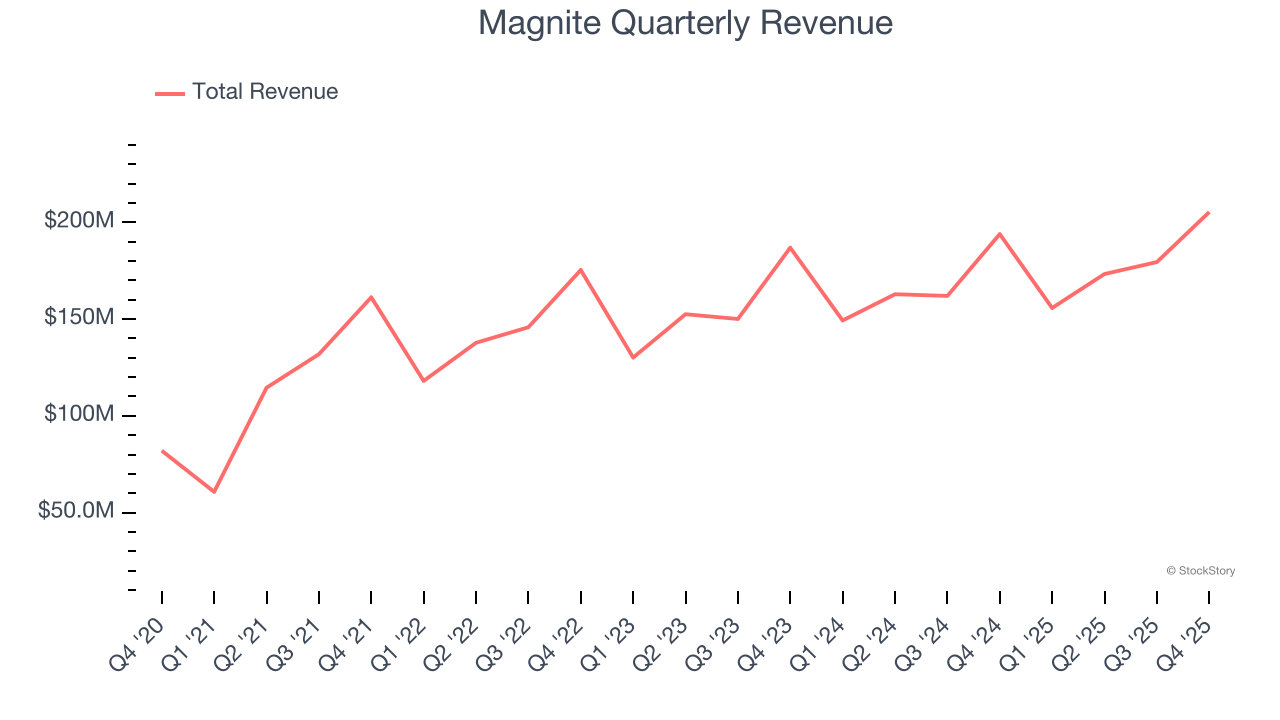

Digital advertising platform Magnite (NASDAQ: MGNI) missed Wall Street’s revenue expectations in Q4 CY2025, but sales rose 5.9% year on year to $205.4 million. Its non-GAAP profit of $0.34 per share was 3.9% below analysts’ consensus estimates.

Is now the time to buy Magnite? Find out by accessing our full research report, it’s free.

Magnite (MGNI) Q4 CY2025 Highlights:

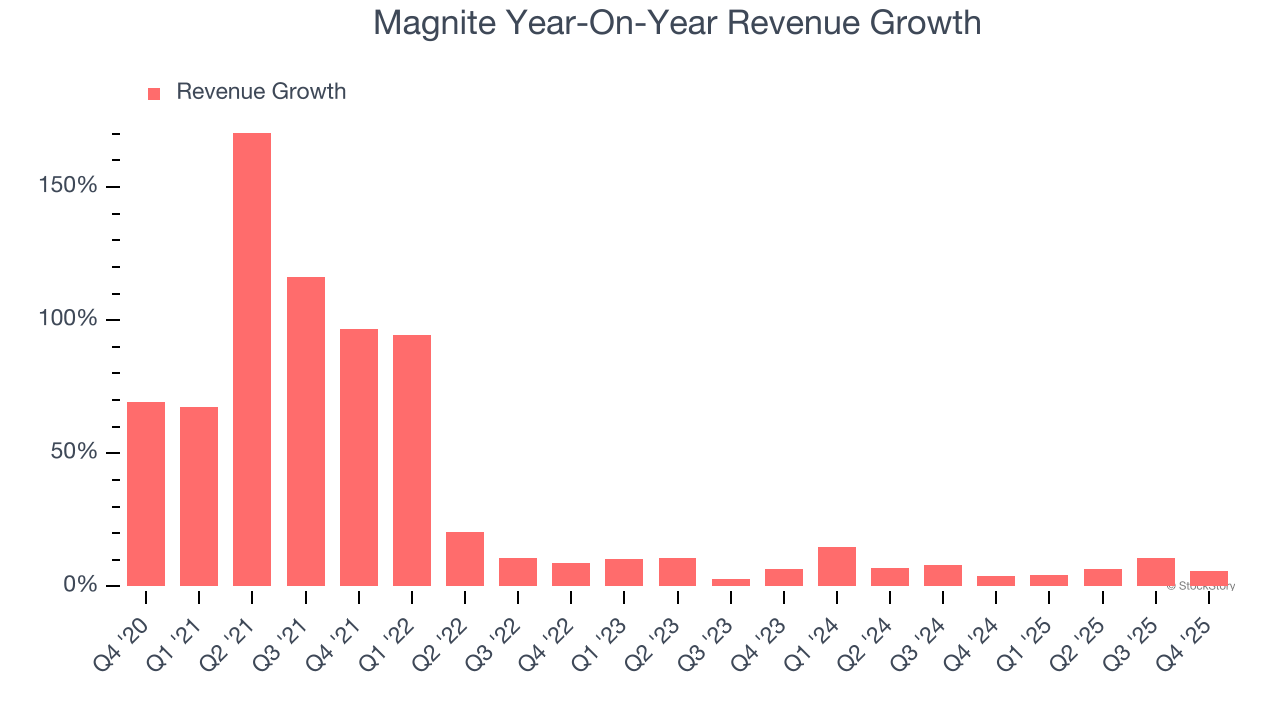

- Revenue: $205.4 million vs analyst estimates of $211.2 million (5.9% year-on-year growth, 2.8% miss)

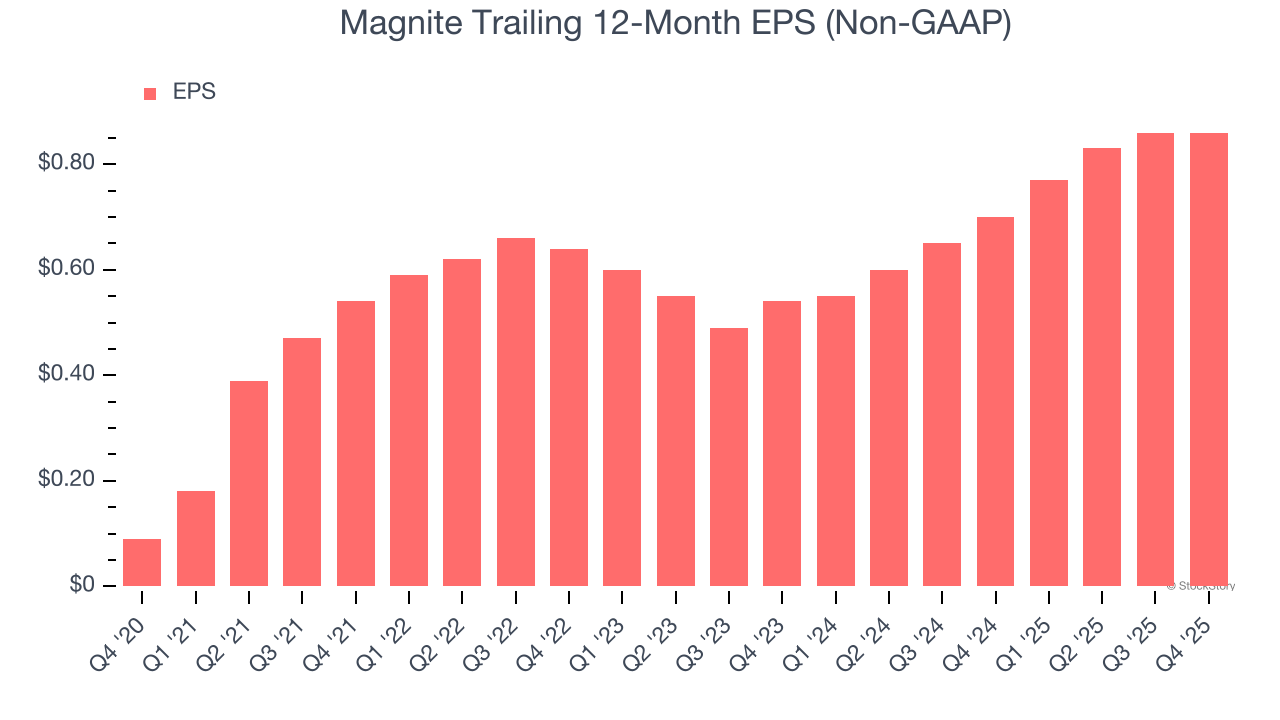

- Adjusted EPS: $0.34 vs analyst expectations of $0.35 (3.9% miss)

- Adjusted EBITDA: $52.93 million vs analyst estimates of $80.88 million (25.8% margin, 34.6% miss)

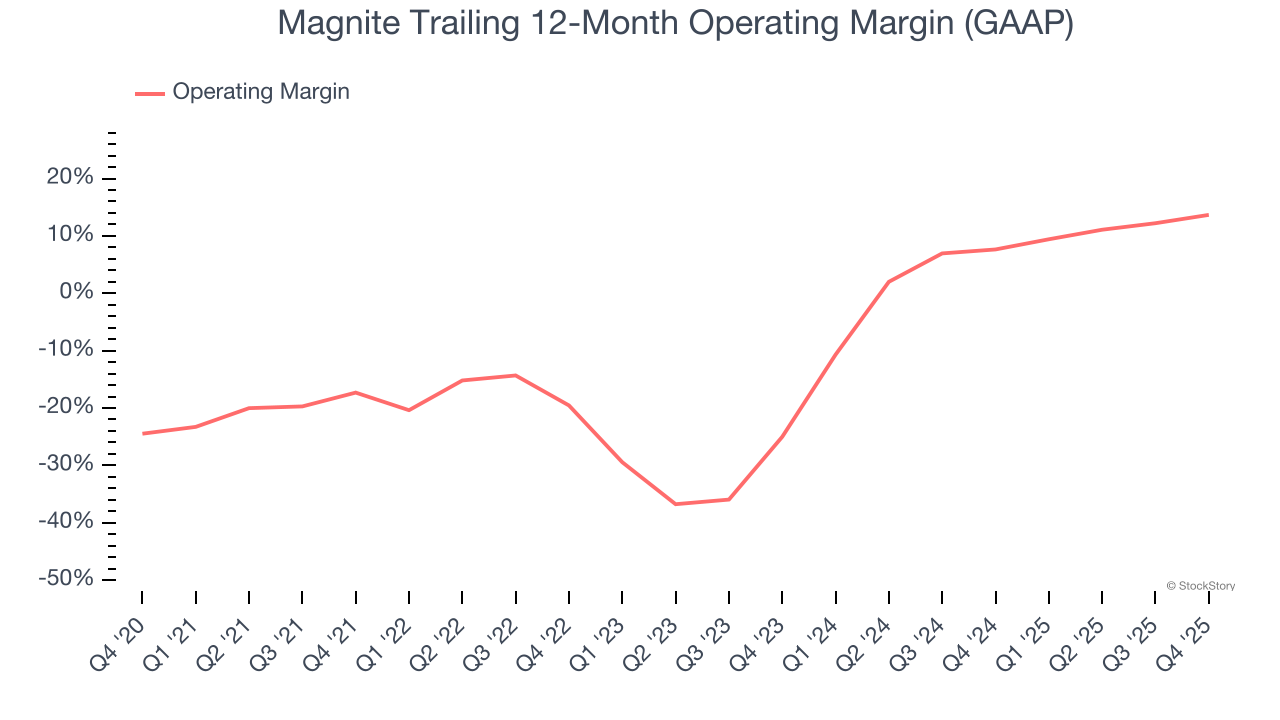

- Operating Margin: 25.3%, up from 20.7% in the same quarter last year

- Free Cash Flow Margin: 50.2%, down from 57.2% in the same quarter last year

- Market Capitalization: $1.68 billion

“We are extremely pleased to see a significant inflection in the growth of the programmatic CTV market, evidenced by our 32% top-line growth excluding political, in the fourth quarter, as well as strength into Q1. We are witnessing spend shift into CTV from various areas of digital advertising, including from DV+. Magnite has the core technology, partnerships, trust, and team to emerge as the most valued player in CTV, which now in Q1 makes up more than 50% of our business,” said Michael G. Barrett, CEO of Magnite.

Company Overview

Born from the 2020 merger of Rubicon Project and Telaria, Magnite (NASDAQ: MGNI) operates the world's largest independent sell-side advertising platform that automates the buying and selling of digital advertising inventory across all channels and formats.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $714 million in revenue over the past 12 months, Magnite is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

As you can see below, Magnite’s 26.4% annualized revenue growth over the last five years was incredible. This is a great starting point for our analysis because it shows Magnite’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Magnite’s annualized revenue growth of 7.3% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Magnite’s revenue grew by 5.9% year on year to $205.4 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 14.3% over the next 12 months, an improvement versus the last two years. This projection is noteworthy and suggests its newer products and services will catalyze better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Although Magnite was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 6.6% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Magnite’s operating margin rose by 31 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to show consistent profitability.

In Q4, Magnite generated an operating margin profit margin of 25.3%, up 4.6 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Magnite’s EPS grew at an astounding 57.1% compounded annual growth rate over the last five years, higher than its 26.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into the nuances of Magnite’s earnings can give us a better understanding of its performance. As we mentioned earlier, Magnite’s operating margin expanded by 31 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Magnite, its two-year annual EPS growth of 26.2% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Magnite reported adjusted EPS of $0.34, in line with the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Magnite’s full-year EPS of $0.86 to grow 28.3%.

Key Takeaways from Magnite’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 2.1% to $11.72 immediately after reporting.

Magnite didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).