Over the past six months, Piper Sandler’s shares (currently trading at $310.18) have posted a disappointing 7.3% loss, well below the S&P 500’s 6.2% gain. This may have investors wondering how to approach the situation.

Given the weaker price action, is this a buying opportunity for PIPR? Find out in our full research report, it’s free.

Why Do Investors Watch Piper Sandler?

Tracing its roots back to 1895 and rebranded from Piper Jaffray in 2020, Piper Sandler (NYSE: PIPR) is an investment bank that provides advisory services, capital raising, institutional brokerage, and research for corporations, governments, and institutional investors.

Three Positive Attributes:

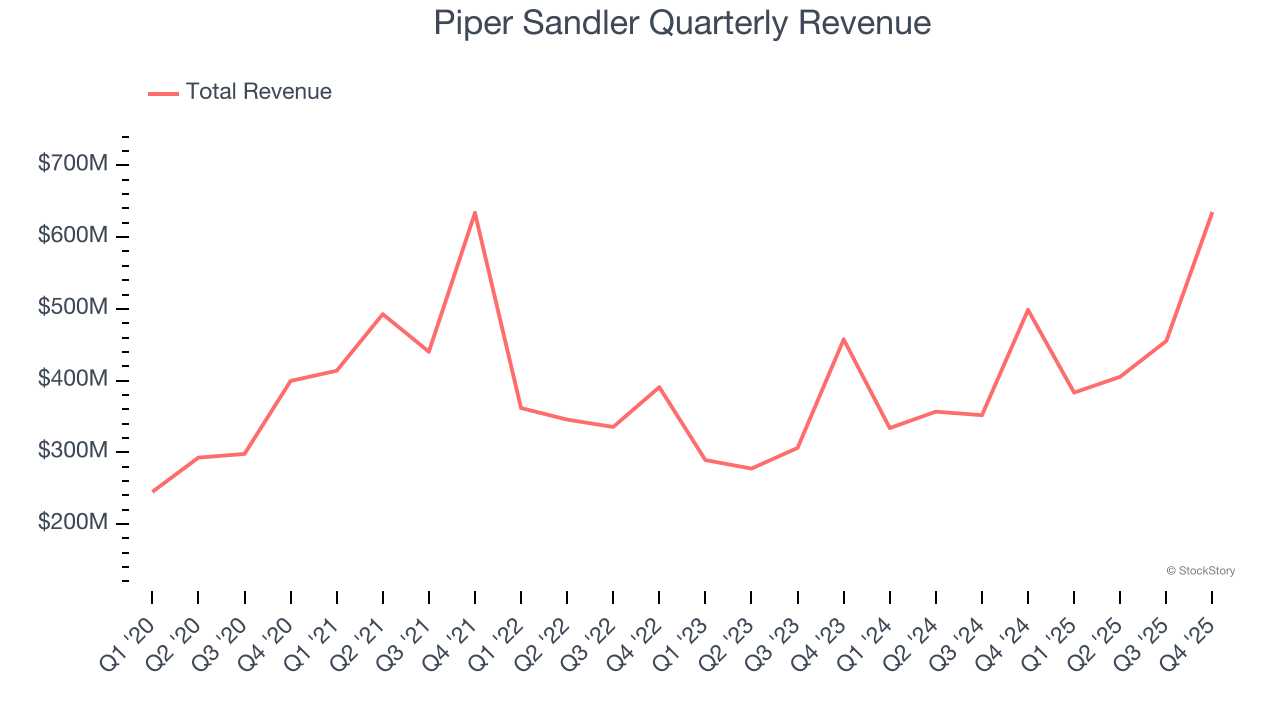

1. Long-Term Revenue Growth Shows Momentum

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

Luckily, Piper Sandler’s revenue grew at a decent 8.8% compounded annual growth rate over the last five years. Its growth was slightly above the average financials company and shows its offerings resonate with customers.

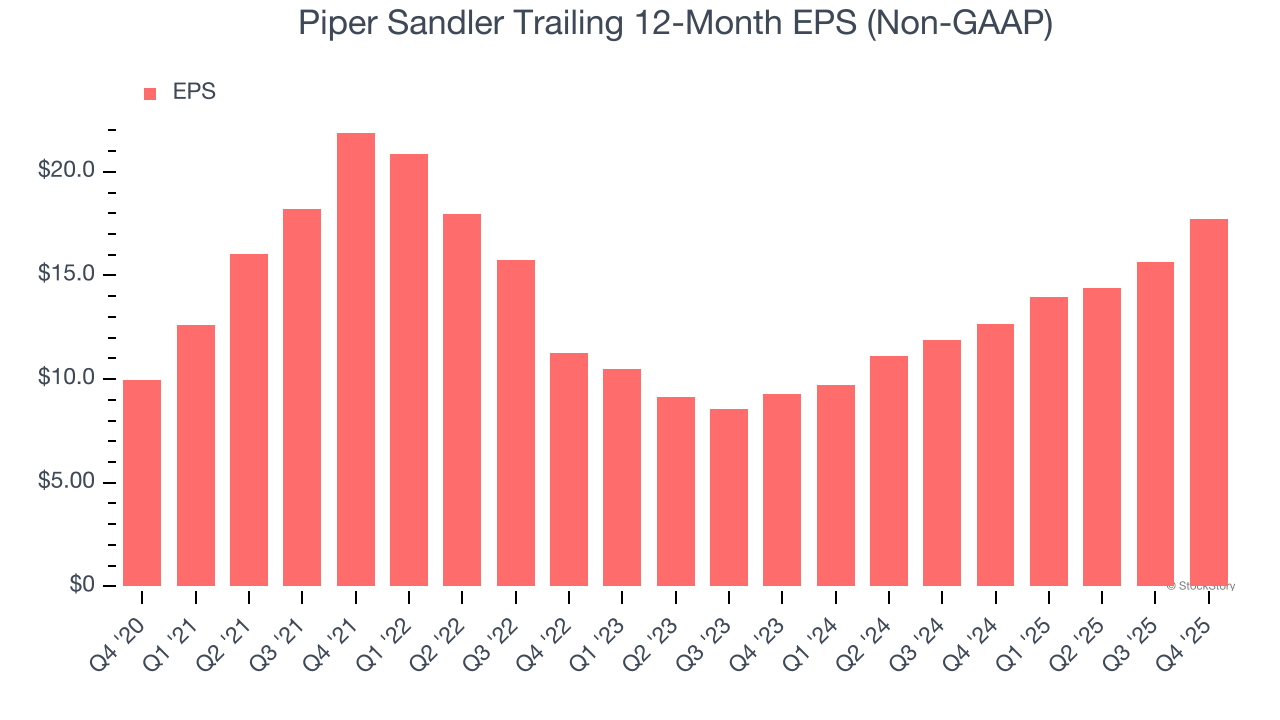

2. EPS Moving Up Steadily

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Piper Sandler’s EPS grew at a decent 12.2% compounded annual growth rate over the last five years, higher than its 8.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

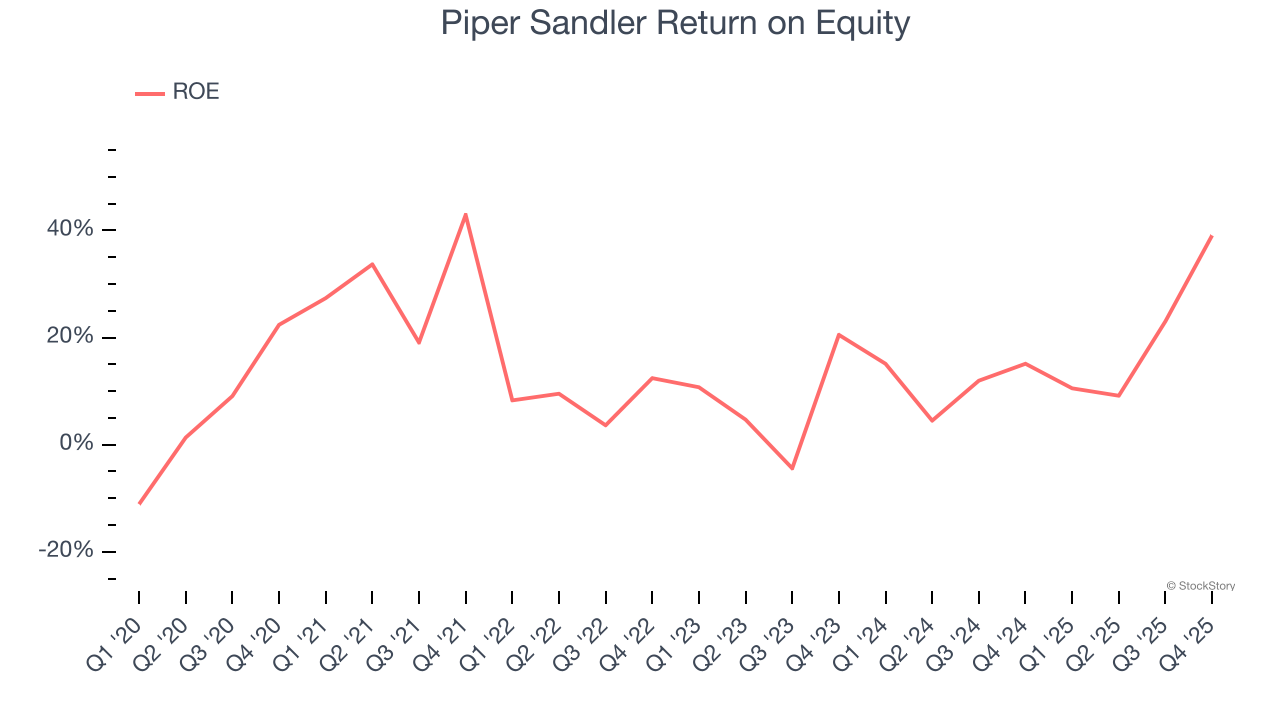

3. Market-Beating ROE Showcases Attractive Growth Opportunities

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, Piper Sandler has averaged an ROE of 15.8%, healthy for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This shows Piper Sandler has a decent competitive moat.

Final Judgment

There are definitely things to like about Piper Sandler. After the recent drawdown, the stock trades at 15.8× forward P/E (or $310.18 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Piper Sandler

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.