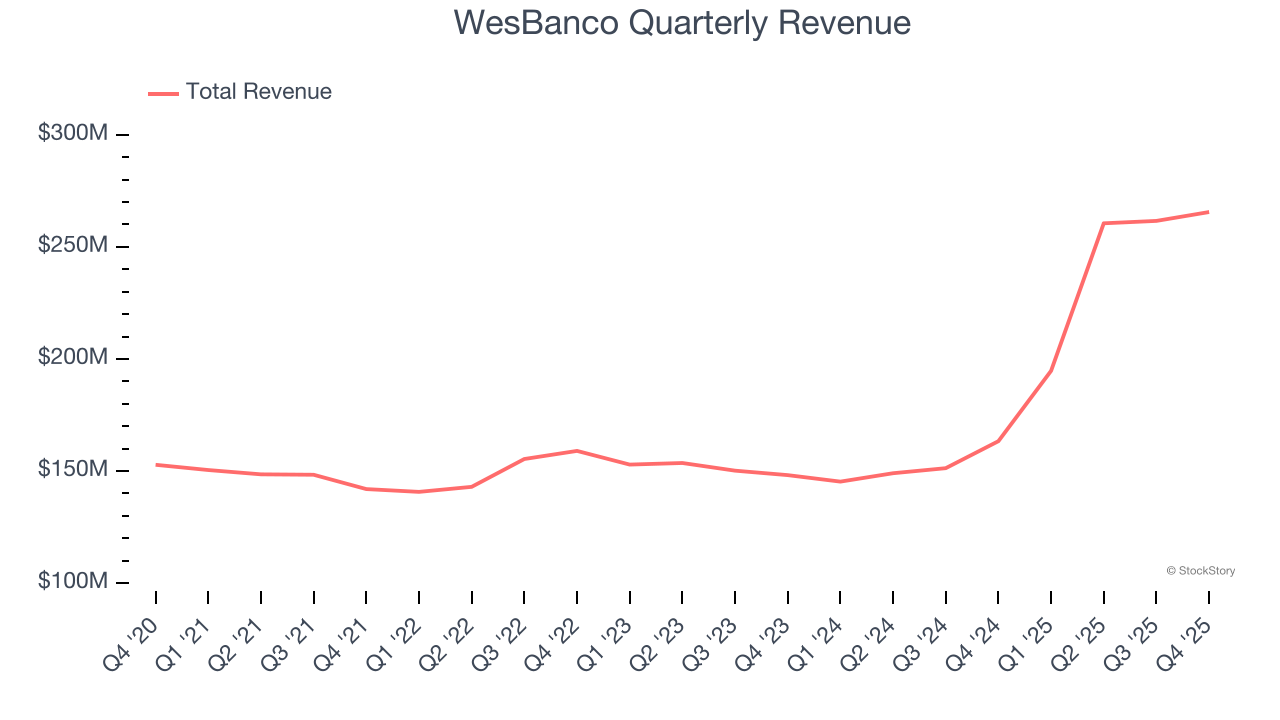

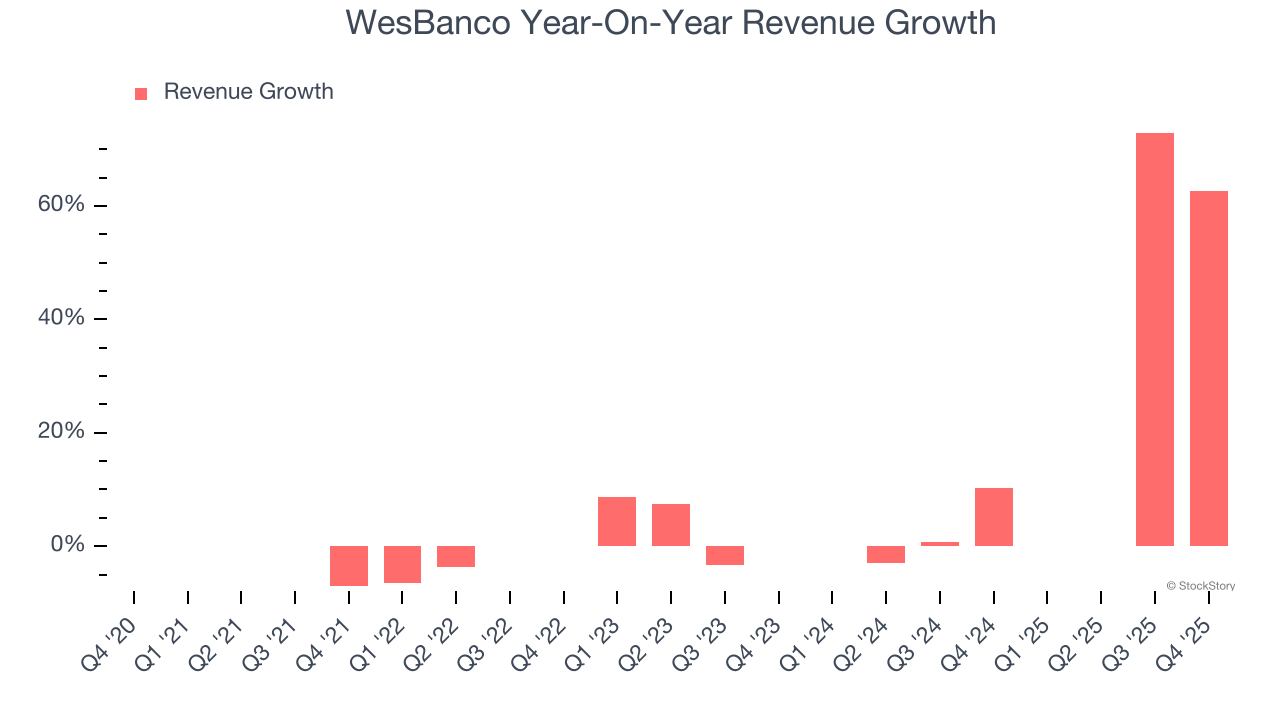

Regional banking company WesBanco (NASDAQ: WSBC) met Wall Streets revenue expectations in Q4 CY2025, with sales up 62.6% year on year to $265.6 million. Its non-GAAP profit of $0.84 per share was 1.2% below analysts’ consensus estimates.

Is now the time to buy WesBanco? Find out by accessing our full research report, it’s free.

WesBanco (WSBC) Q4 CY2025 Highlights:

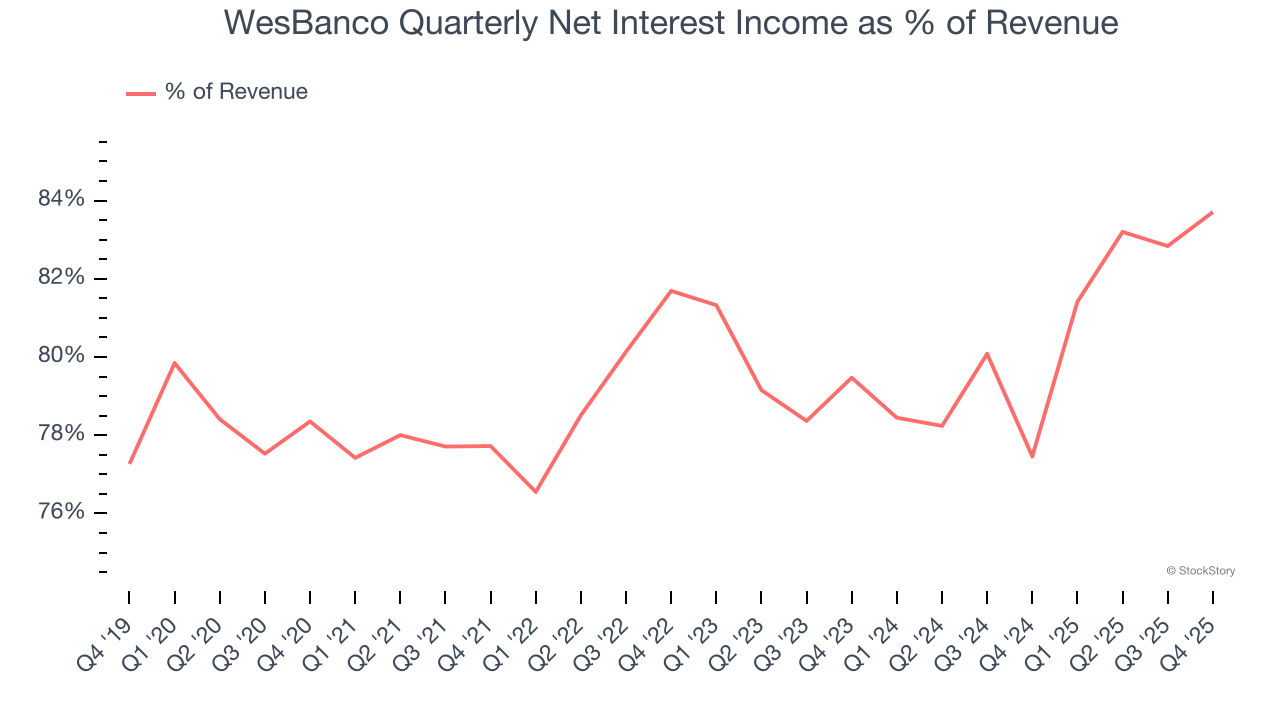

- Net Interest Income: $222.3 million vs analyst estimates of $221.7 million (75.7% year-on-year growth, in line)

- Net Interest Margin: 3.6% vs analyst estimates of 3.6% (3.6 basis point beat)

- Revenue: $265.6 million vs analyst estimates of $265.8 million (62.6% year-on-year growth, in line)

- Efficiency Ratio: 51.6% vs analyst estimates of 54.6% (295.5 basis point beat)

- Adjusted EPS: $0.84 vs analyst expectations of $0.85 (1.2% miss)

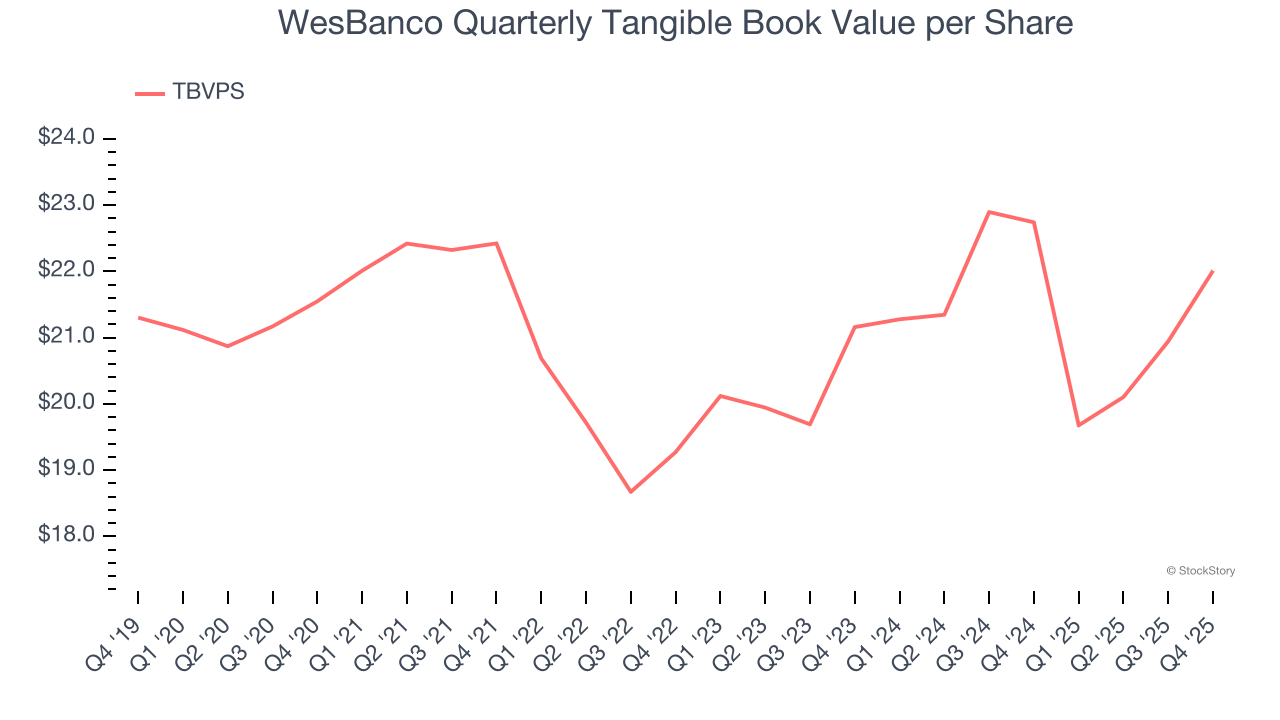

- Tangible Book Value per Share: $22.01 vs analyst estimates of $21.70 (3.2% year-on-year decline, 1.4% beat)

- Market Capitalization: $3.35 billion

"2025 was another year of disciplined growth and strong execution for WesBanco as we continued our transformation into a regional financial services partner through our successful acquisition and integration of Premier Financial and its customers," said Jeff Jackson, President and Chief Executive Officer.

Company Overview

Tracing its roots back to 1870 in West Virginia, WesBanco (NASDAQ: WSBC) is a bank holding company that provides retail and commercial banking, trust services, insurance, and investment products through its subsidiaries across several Midwestern and Mid-Atlantic states.

Sales Growth

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions. Over the last five years, WesBanco grew its revenue at a mediocre 10% compounded annual growth rate. This was below our standard for the banking sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. WesBanco’s annualized revenue growth of 27.4% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, WesBanco’s year-on-year revenue growth of 62.6% was magnificent, and its $265.6 million of revenue was in line with Wall Street’s estimates.

Net interest income made up 79.6% of the company’s total revenue during the last five years, meaning lending operations are WesBanco’s largest source of revenue.

While banks generate revenue from multiple sources, investors view net interest income as the cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of non-interest income.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Tangible Book Value Per Share (TBVPS)

Banks profit by intermediating between depositors and borrowers, making them fundamentally balance sheet-driven enterprises. Market participants emphasize balance sheet quality and sustained book value growth when evaluating these institutions.

When analyzing banks, tangible book value per share (TBVPS) takes precedence over many other metrics. This measure isolates genuine per-share value by removing intangible assets of debatable liquidation worth. On the other hand, EPS is often distorted by mergers and flexible loan loss accounting. TBVPS provides clearer performance insights.

WesBanco’s TBVPS was flat over the last five years. However, TBVPS growth has accelerated recently, growing by 2% annually over the last two years from $21.16 to $22.01 per share.

Over the next 12 months, Consensus estimates call for WesBanco’s TBVPS to grow by 10% to $24.22, mediocre growth rate.

Key Takeaways from WesBanco’s Q4 Results

It was good to see WesBanco narrowly top analysts’ tangible book value per share expectations this quarter. On the other hand, its EPS slightly missed. Overall, this was a softer quarter. The stock remained flat at $35.23 immediately after reporting.

So should you invest in WesBanco right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).