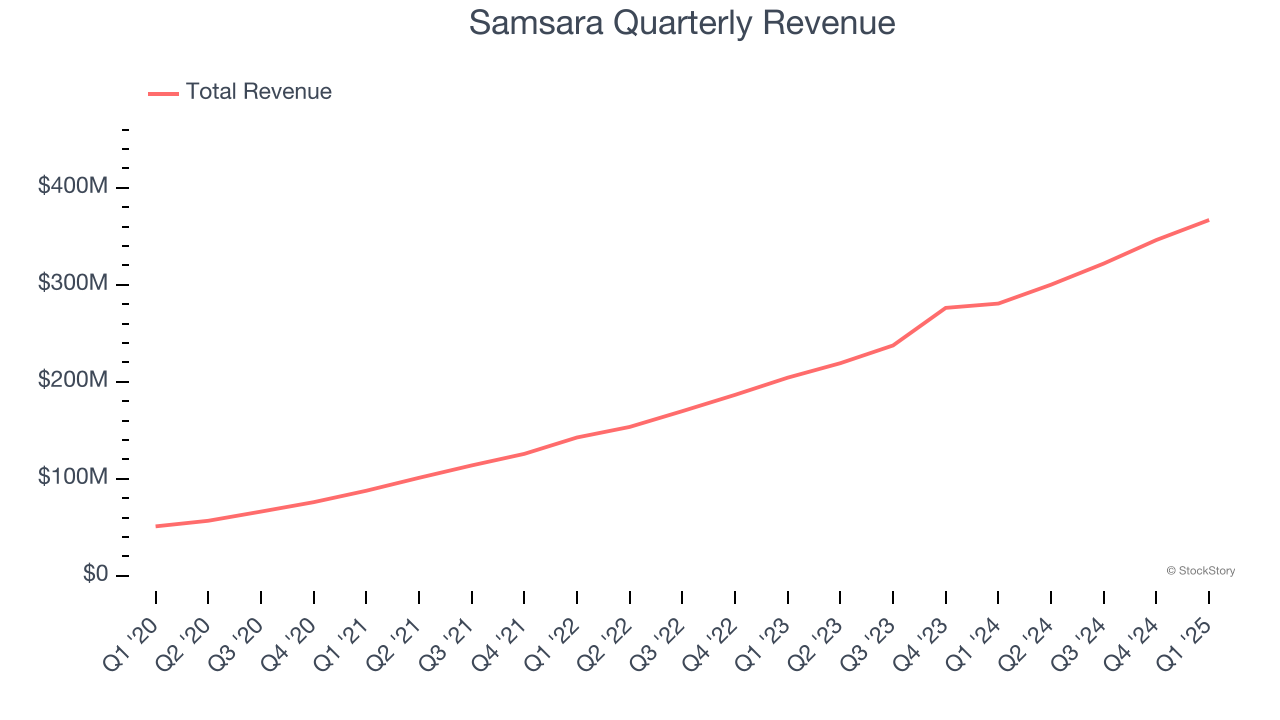

Internet of Things company Samsara (NYSE: IOT) announced better-than-expected revenue in Q1 CY2025, with sales up 30.7% year on year to $366.9 million. Guidance for next quarter’s revenue was better than expected at $372 million at the midpoint, 0.7% above analysts’ estimates. Its non-GAAP profit of $0.11 per share was 91.6% above analysts’ consensus estimates.

Is now the time to buy Samsara? Find out by accessing our full research report, it’s free.

Samsara (IOT) Q1 CY2025 Highlights:

- Revenue: $366.9 million vs analyst estimates of $351.5 million (30.7% year-on-year growth, 4.4% beat)

- Adjusted EPS: $0.11 vs analyst estimates of $0.06 (91.6% beat)

- Adjusted Operating Income: $51.07 million vs analyst estimates of $24.93 million (13.9% margin, significant beat)

- The company lifted its revenue guidance for the full year to $1.55 billion at the midpoint from $1.53 billion, a 1.5% increase

- Management raised its full-year Adjusted EPS guidance to $0.40 at the midpoint, a 21.2% increase

- Operating Margin: -9.1%, up from -23.5% in the same quarter last year

- Free Cash Flow Margin: 12.5%, down from 14% in the previous quarter

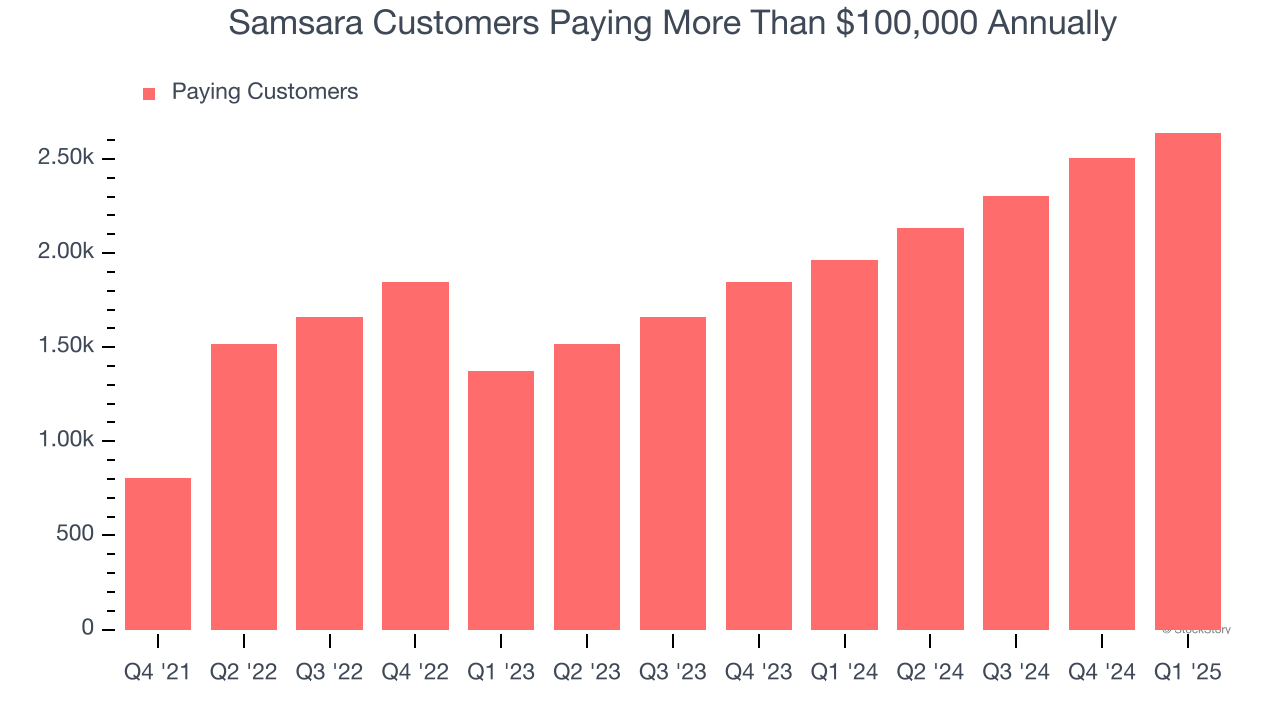

- Customers: 2,638 customers paying more than $100,000 annually

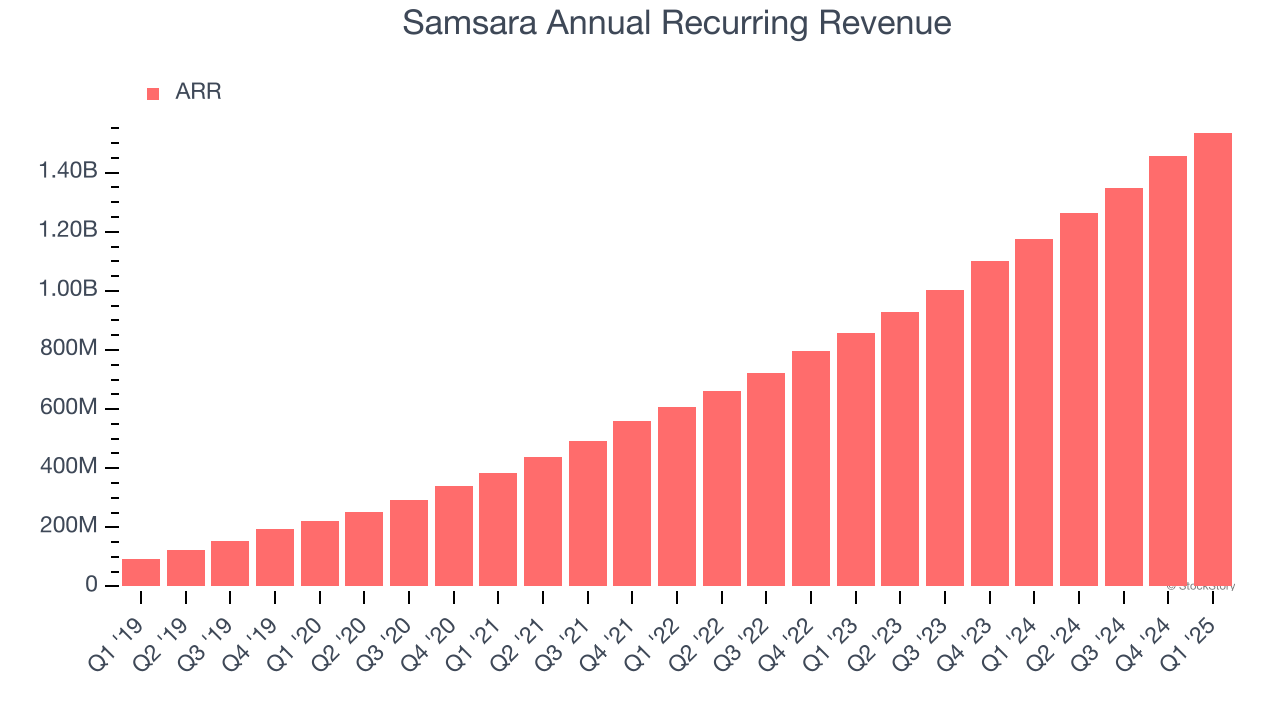

- Annual Recurring Revenue: $1.54 billion at quarter end, up 30.6% year on year

- Billings: $366.9 million at quarter end, up 21% year on year

- Market Capitalization: $26.61 billion

“We delivered a strong first quarter of the new fiscal year with Q1 revenue of $366.9 million, growing 32% year-over-year in constant currency,” said Sanjit Biswas, CEO and co-founder of Samsara.

Company Overview

One of the few public companies where Marc Andreessen is a Board member, Samsara (NYSE: IOT) provides software and hardware to track industrial equipment, assets, and fleets.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Samsara’s 40.3% annualized revenue growth over the last three years was incredible. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Samsara reported wonderful year-on-year revenue growth of 30.7%, and its $366.9 million of revenue exceeded Wall Street’s estimates by 4.4%. Company management is currently guiding for a 23.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 21.1% over the next 12 months, a deceleration versus the last three years. Still, this projection is healthy and suggests the market sees success for its products and services.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Samsara’s ARR punched in at $1.54 billion in Q1, and over the last four quarters, its growth was fantastic as it averaged 33.3% year-on-year increases. This performance aligned with its total sales growth and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes Samsara a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

Enterprise Customer Base

This quarter, Samsara reported 2,638 enterprise customers paying more than $100,000 annually, an increase of 132 from the previous quarter. That’s a bit fewer contract wins than last quarter but quite a bit above what we’ve seen over the last 12 months, suggesting its recent sales momentum is still healthy but softening after a tough comp quarter from the prior year.

Key Takeaways from Samsara’s Q1 Results

We were impressed by Samsara’s optimistic EPS guidance for next quarter, which beat analysts’ expectations. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its billings missed. Overall, we think this was still a mixed quarter. The market seemed to be hoping for more, and the stock traded down 12% to $41.69 immediately following the results.

So should you invest in Samsara right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.