Over the last six months, GE HealthCare’s shares have sunk to $69.75, producing a disappointing 12.1% loss while the S&P 500 was flat. This might have investors contemplating their next move.

Is there a buying opportunity in GE HealthCare, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is GE HealthCare Not Exciting?

Despite the more favorable entry price, we're swiping left on GE HealthCare for now. Here are three reasons why there are better opportunities than GEHC and a stock we'd rather own.

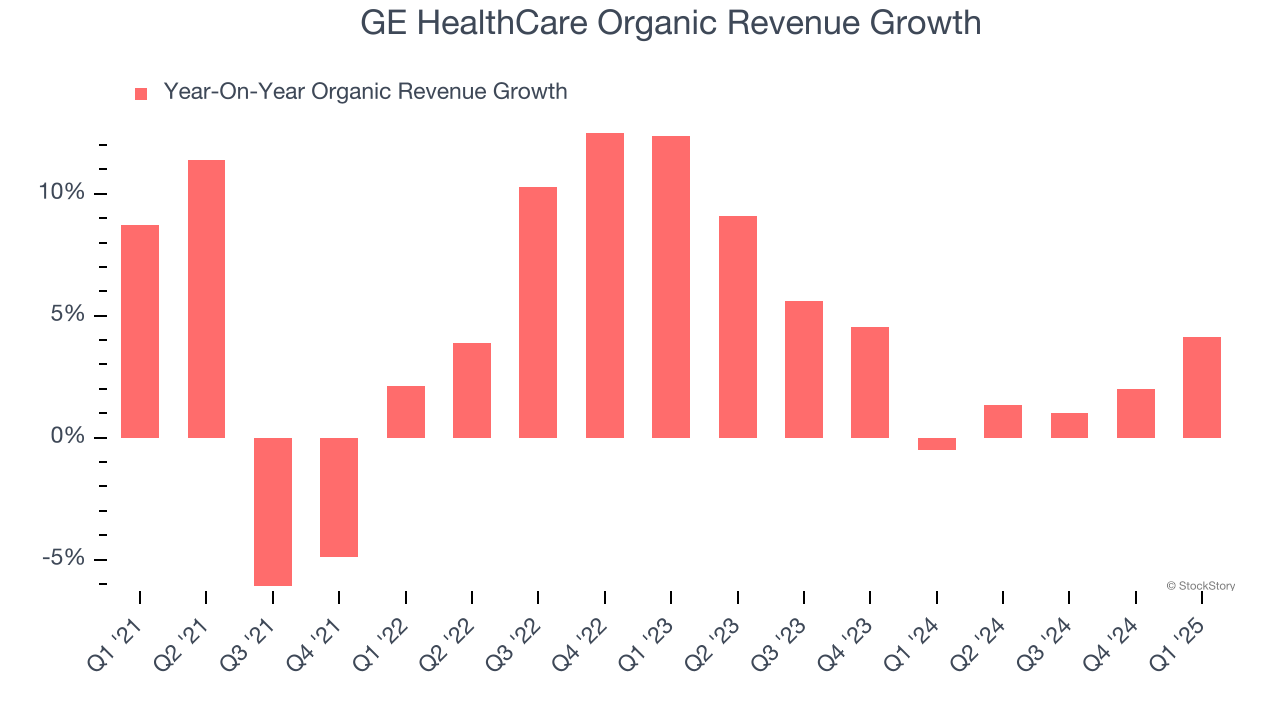

1. Slow Organic Growth Suggests Waning Demand In Core Business

In addition to reported revenue, organic revenue is a useful data point for analyzing Medical Devices & Supplies - Imaging, Diagnostics companies. This metric gives visibility into GE HealthCare’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, GE HealthCare’s organic revenue averaged 3.4% year-on-year growth. This performance slightly lagged the sector and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect GE HealthCare’s revenue to rise by 3.7%, close to its 3.9% annualized growth for the past three years. This projection doesn't excite us and indicates its newer products and services will not lead to better top-line performance yet.

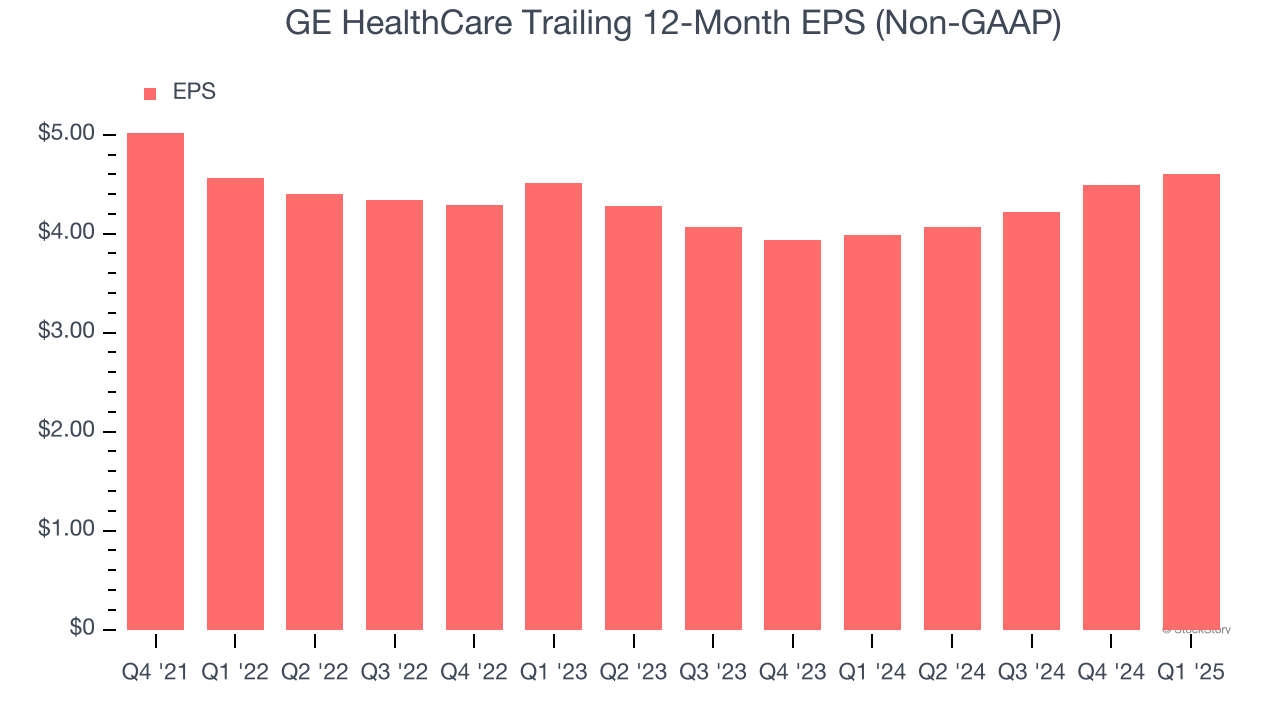

3. EPS Growth Has Stalled

We track the change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

GE HealthCare’s flat EPS over the last three years was below its 3.9% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

GE HealthCare isn’t a terrible business, but it doesn’t pass our bar. After the recent drawdown, the stock trades at 14.7× forward P/E (or $69.75 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. We’d suggest looking at the most entrenched endpoint security platform on the market.

Stocks We Like More Than GE HealthCare

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.