Over the past six months, ServiceNow’s shares (currently trading at $1,003) have posted a disappointing 5.5% loss, well below the S&P 500’s 1.7% gain. This might have investors contemplating their next move.

Given the weaker price action, is now a good time to buy NOW? Find out in our full research report, it’s free.

Why Are We Positive On NOW?

Founded by Fred Luddy, who coded the company's initial prototype on a flight from San Francisco to London, ServiceNow (NYSE: NOW) is a software provider helping companies automate workflows across IT, HR, and customer service.

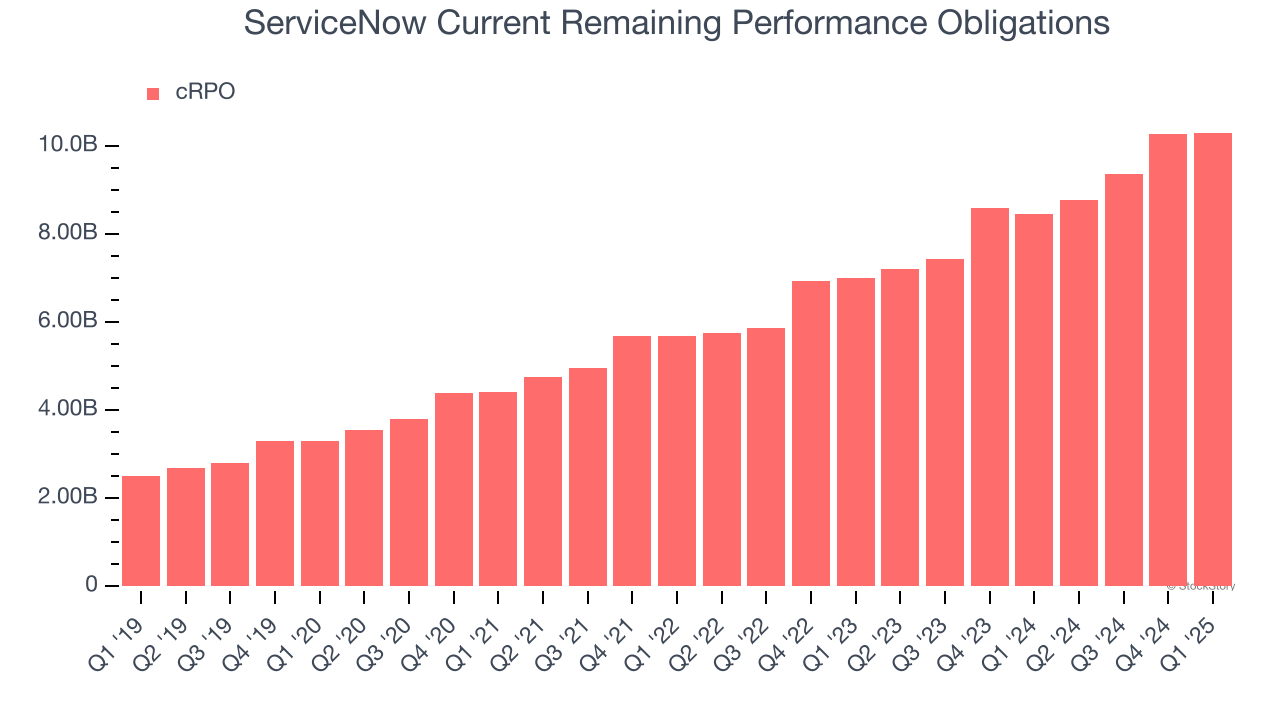

1. Surging cRPO Locks In Future Sales

In addition to reported revenue, it is useful to analyze cRPO, or current remaining performance obligations, for ServiceNow because it shows the value of contracted services to be delivered over the next year. It therefore gives visibility into future revenue.

ServiceNow’s cRPO punched in at $10.31 billion in Q1, and over the last four quarters, its year-on-year growth averaged 22.3%. This performance was impressive and shows the company has a robust pipeline of undelivered services. Its growth also suggests that customers are committing to long-term contracts, enhancing ServiceNow’s predictability and providing a tailwind to its valuation.

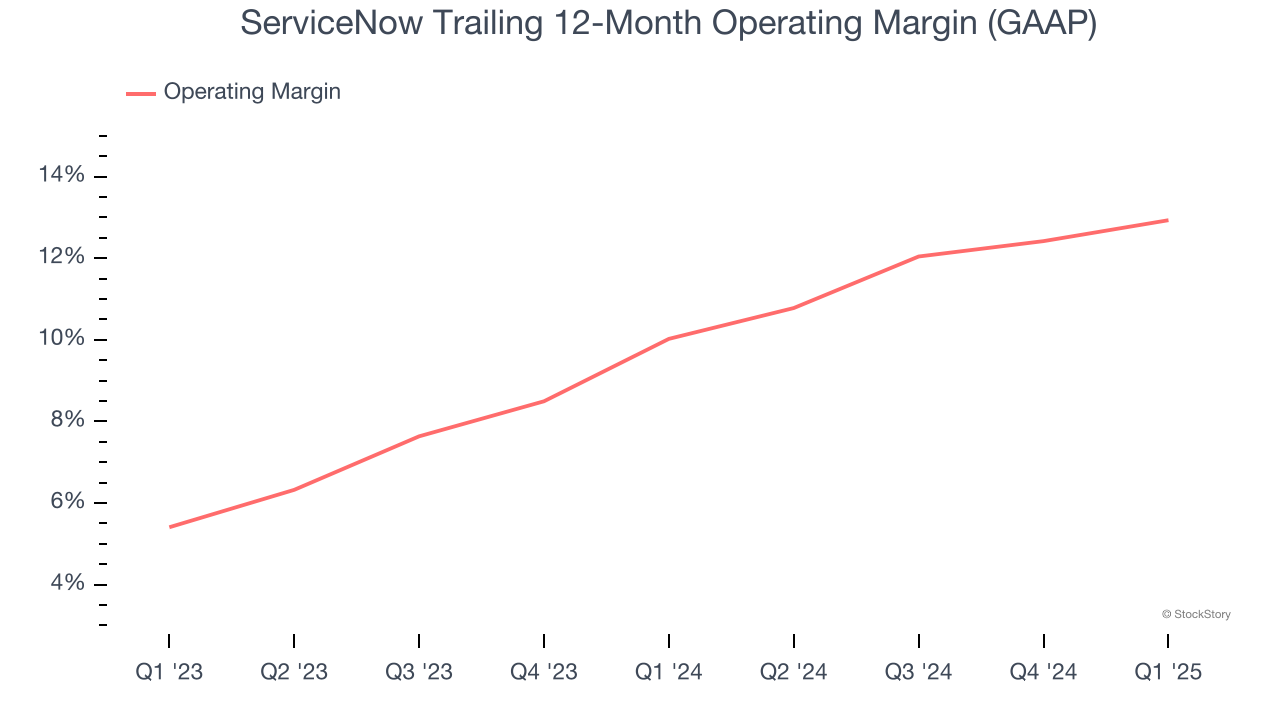

2. Operating Margin Reveals a Well-Run Organization

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

ServiceNow has been a well-oiled machine over the last year. It demonstrated elite profitability for a software business, boasting an average operating margin of 12.9%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

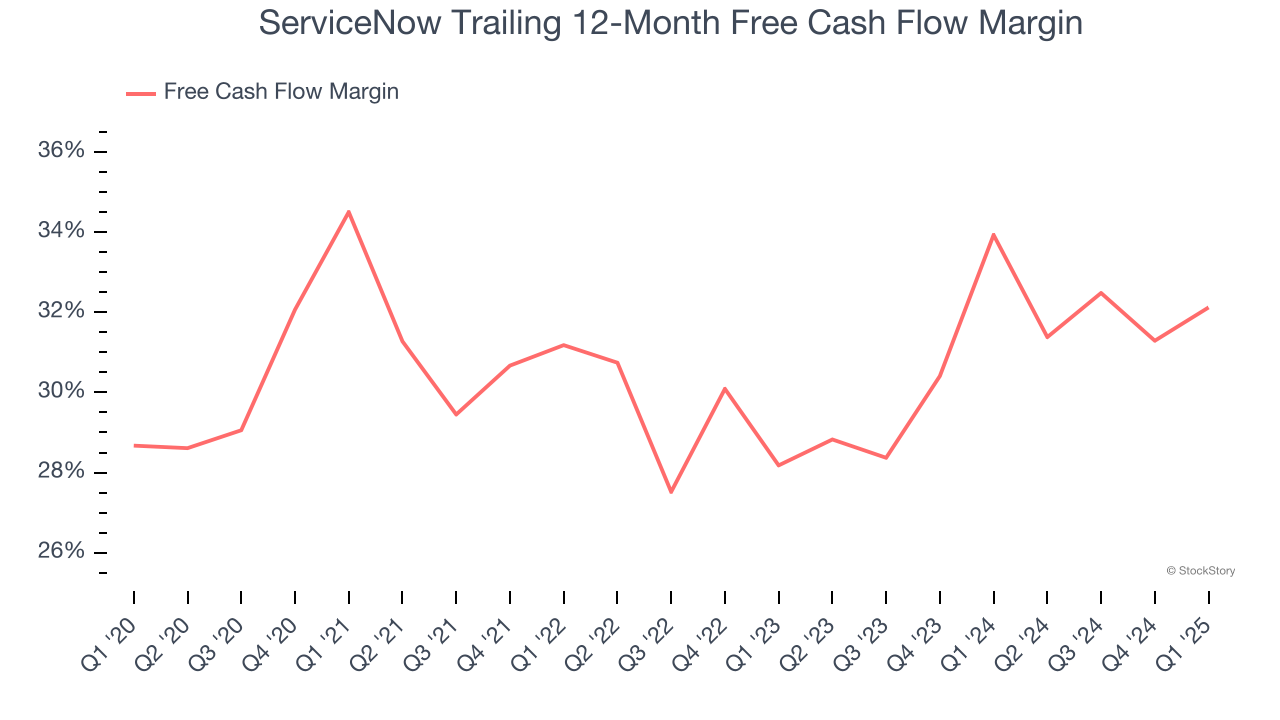

3. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

ServiceNow has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the software sector, averaging an eye-popping 32.1% over the last year.

Final Judgment

These are just a few reasons why we think ServiceNow is a high-quality business. With the recent decline, the stock trades at 15.5× forward price-to-sales (or $1,003 per share). Is now a good time to buy? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than ServiceNow

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.