IT services provider DXC Technology (NYSE: DXC) beat Wall Street’s revenue expectations in Q1 CY2025, but sales fell by 6.4% year on year to $3.17 billion. On the other hand, next quarter’s revenue guidance of $3.07 billion was less impressive, coming in 1.4% below analysts’ estimates. Its non-GAAP profit of $0.84 per share was 8.6% above analysts’ consensus estimates.

Is now the time to buy DXC? Find out by accessing our full research report, it’s free.

DXC (DXC) Q1 CY2025 Highlights:

- Revenue: $3.17 billion vs analyst estimates of $3.14 billion (6.4% year-on-year decline, 0.9% beat)

- Adjusted EPS: $0.84 vs analyst estimates of $0.77 (8.6% beat)

- Adjusted EBITDA: $741 million vs analyst estimates of $458.1 million (23.4% margin, 61.7% beat)

- Management’s revenue guidance for the upcoming financial year 2026 is $12.31 billion at the midpoint, missing analyst estimates by 0.8% and implying -4.4% growth (vs -5.8% in FY2025)

- Adjusted EPS guidance for the upcoming financial year 2026 is $3 at the midpoint, missing analyst estimates by 12%

- Operating Margin: 11%, up from -7% in the same quarter last year

- Free Cash Flow Margin: 3.5%, down from 4.6% in the same quarter last year

- Organic Revenue fell 4.2% year on year, in line with the same quarter last year

- Market Capitalization: $3.07 billion

Company Overview

Born from the 2017 merger of Computer Sciences Corporation and HP Enterprise's services business, DXC Technology (NYSE: DXC) is a global IT services company that helps businesses transform their technology infrastructure, applications, and operations.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

With $12.87 billion in revenue over the past 12 months, DXC is larger than most business services companies and benefits from economies of scale, enabling it to gain more leverage on its fixed costs than smaller competitors. This also gives it the flexibility to offer lower prices. However, its scale is a double-edged sword because it’s challenging to maintain high growth rates when you’ve already captured a large portion of the addressable market. For DXC to boost its sales, it likely needs to adjust its prices, launch new offerings, or lean into foreign markets.

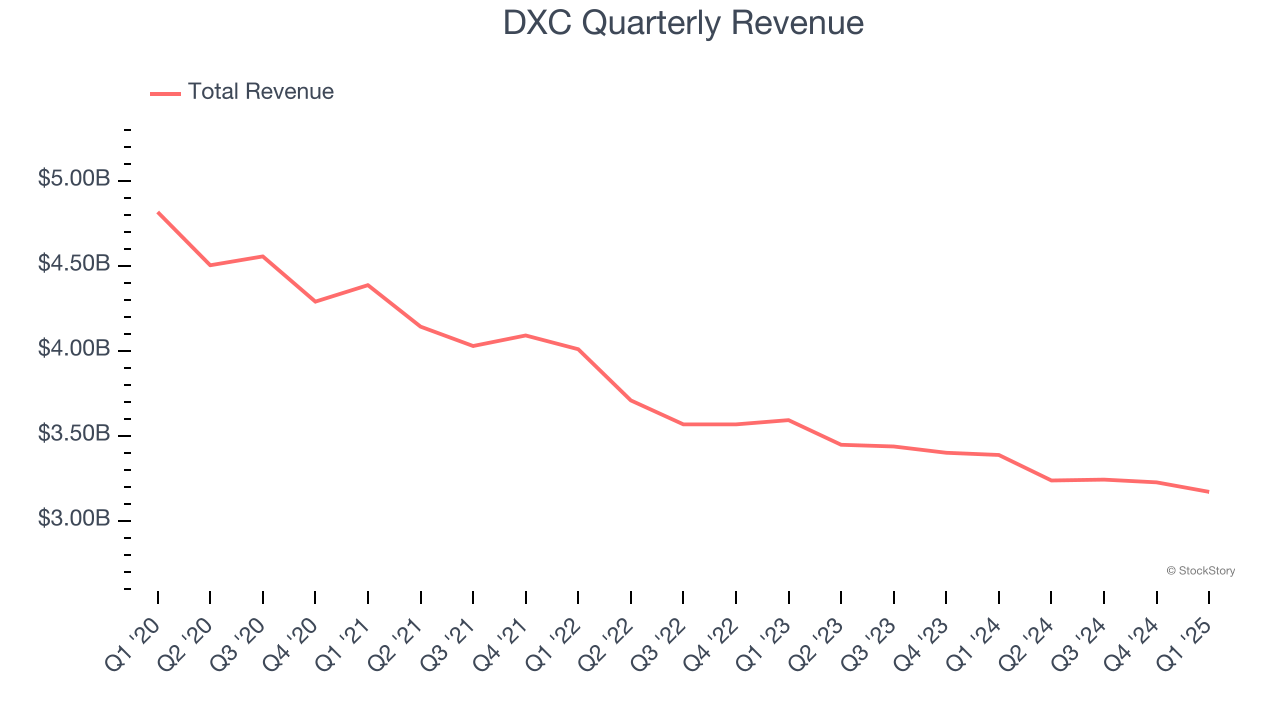

As you can see below, DXC’s demand was weak over the last five years. Its sales fell by 8% annually, a tough starting point for our analysis.

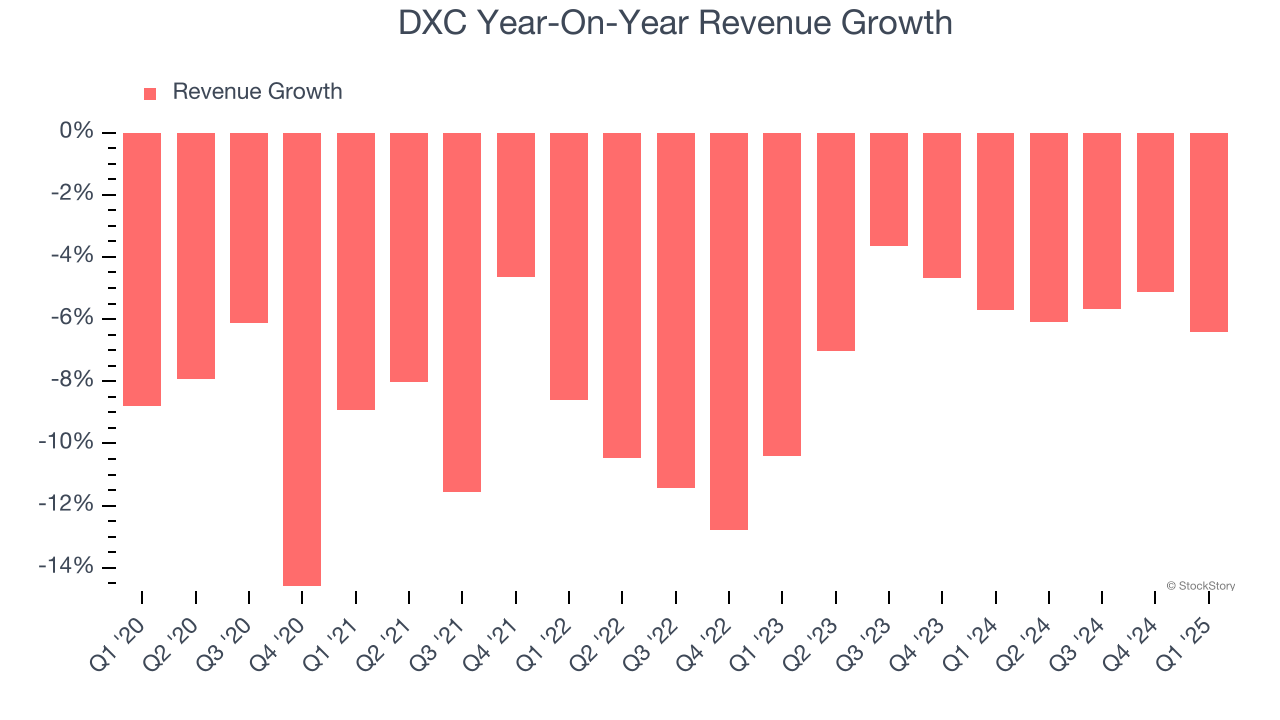

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. DXC’s annualized revenue declines of 5.6% over the last two years suggest its demand continued shrinking.

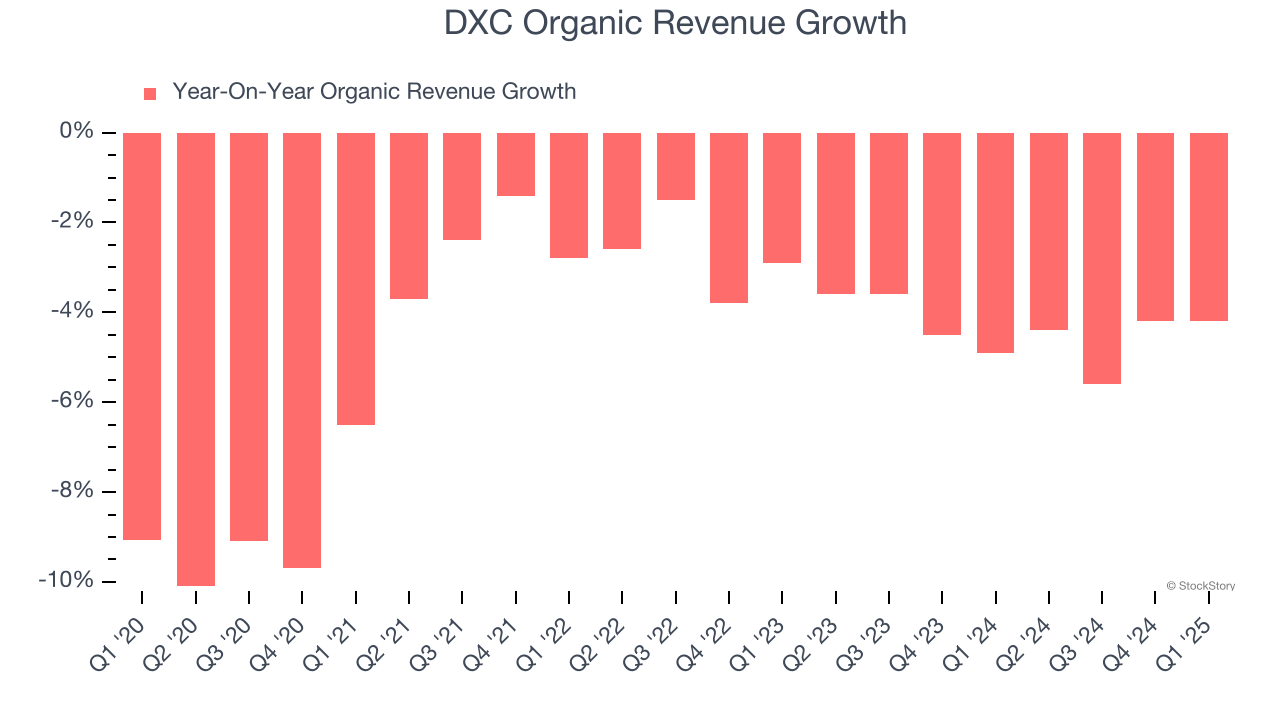

DXC also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, DXC’s organic revenue averaged 4.4% year-on-year declines. Because this number aligns with its normal revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, DXC’s revenue fell by 6.4% year on year to $3.17 billion but beat Wall Street’s estimates by 0.9%. Company management is currently guiding for a 5.3% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 3.4% over the next 12 months. While this projection is better than its two-year trend, it's hard to get excited about a company that is struggling with demand.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

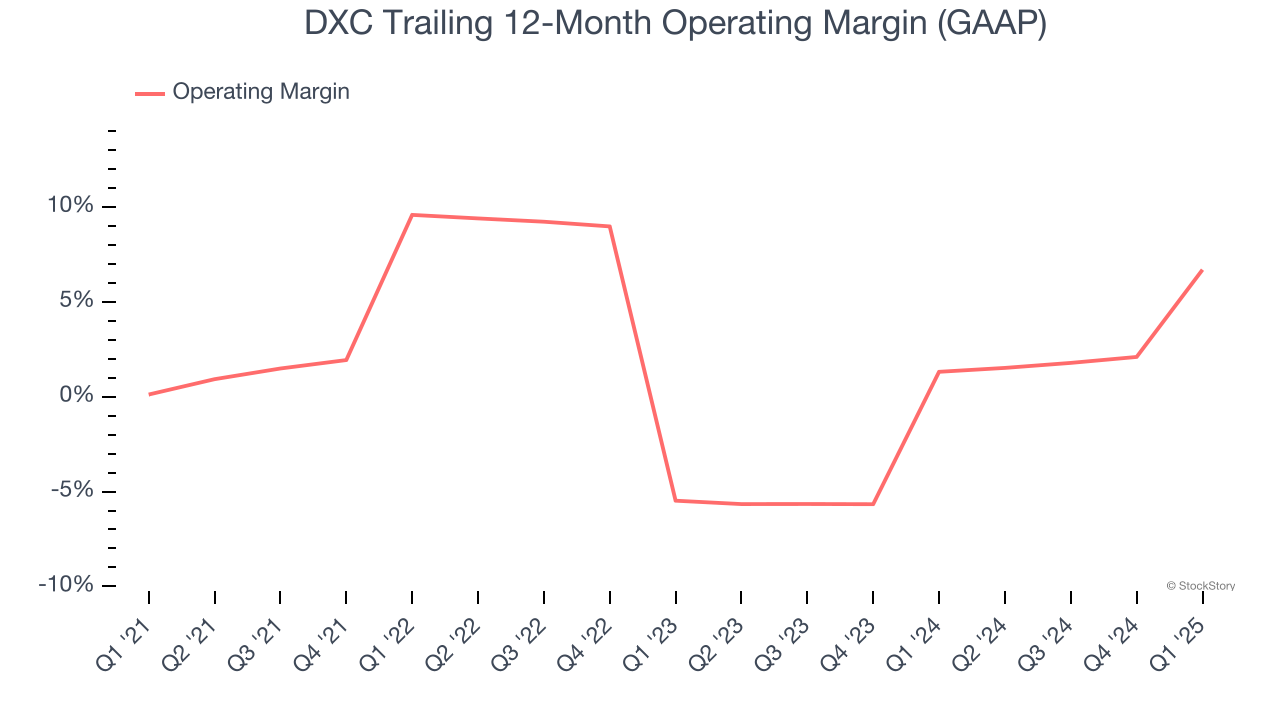

DXC was profitable over the last five years but held back by its large cost base. Its average operating margin of 2.4% was weak for a business services business.

On the plus side, DXC’s operating margin rose by 6.6 percentage points over the last five years.

In Q1, DXC generated an operating profit margin of 11%, up 18 percentage points year on year. This increase was a welcome development, especially since its revenue fell, showing it was more efficient because it scaled down its expenses.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for DXC, its EPS declined by 9.3% annually over the last five years, more than its revenue. We can see the difference stemmed from higher interest expenses or taxes as the company actually grew its operating margin and repurchased its shares during this time.

In Q1, DXC reported EPS at $0.84, down from $0.97 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 8.6%. Over the next 12 months, Wall Street expects DXC’s full-year EPS of $3.43 to stay about the same.

Key Takeaways from DXC’s Q1 Results

We enjoyed seeing DXC beat analysts’ revenue, EPS, and EBITDA expectations this quarter. On the other hand, its full-year revenue and EPS guidance fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 12.5% to $14.50 immediately following the results.

DXC’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.