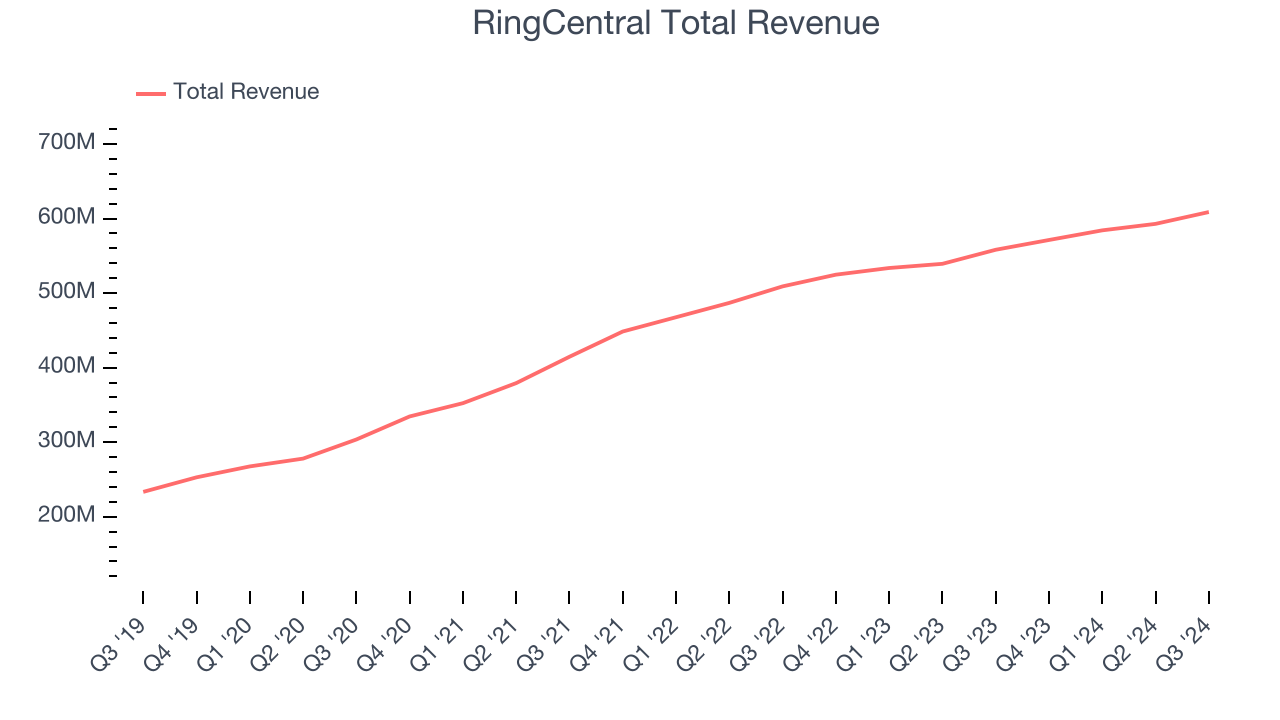

Office and call centre communications software provider RingCentral (NYSE: RNG) reported Q3 CY2024 results topping the market’s revenue expectations, with sales up 9.1% year on year to $608.8 million. On the other hand, the company expects next quarter’s revenue to be around $612 million, slightly below analysts’ estimates. Its non-GAAP profit of $0.95 per share was also 3% above analysts’ consensus estimates.

Is now the time to buy RingCentral? Find out by accessing our full research report, it’s free.

RingCentral (RNG) Q3 CY2024 Highlights:

- Revenue: $608.8 million vs analyst estimates of $602.1 million (1.1% beat)

- Adjusted EPS: $0.95 vs analyst estimates of $0.92 (3% beat)

- EBITDA: $149 million vs analyst estimates of $147.4 million (1.1% beat)

- Revenue Guidance for Q4 CY2024 is $612 million at the midpoint, below analyst estimates of $616 million

- Adjusted EPS guidance for the full year is $3.69 at the midpoint, roughly in line with what analysts were expecting

- Gross Margin (GAAP): 70.4%, in line with the same quarter last year

- Operating Margin: 0%, up from -9.7% in the same quarter last year

- EBITDA Margin: 24.5%, up from 22.9% in the same quarter last year

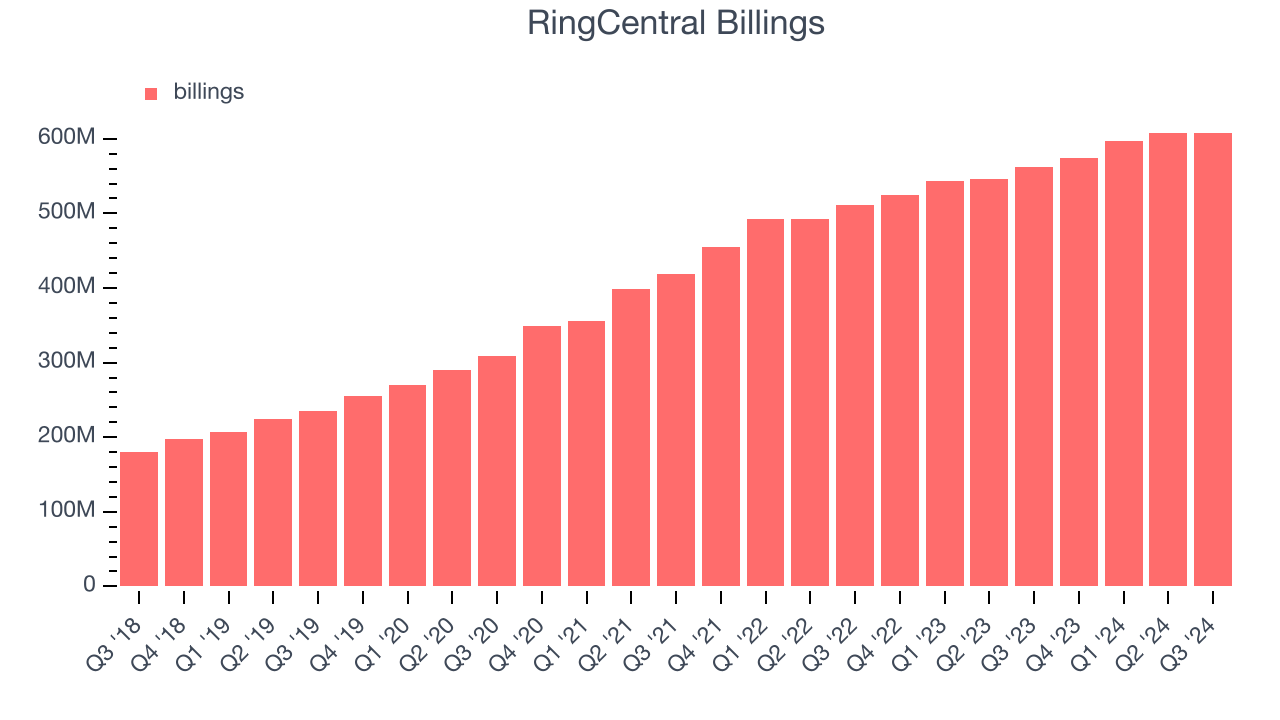

- Billings: $607.7 million at quarter end, up 8.1% year on year

- Market Capitalization: $3.44 billion

“Our strong results were driven by continued momentum with new products, in particular RingCX, and strength in our core UCaaS market,” said Vlad Shmunis, RingCentral’s Founder, Chairman, and CEO.

Company Overview

Founded in 1999 during the dot-com era, RingCentral (NYSE: RNG) provides software as a service that unifies phone, text, fax, video calls and chat in one platform.

Video Conferencing

Work is becoming more distributed, both across geographies and devices. In order for businesses to keep functioning efficiently, they need to be able to communicate as well as they did when the teams were co-located, which drives the demand for integrated communication platforms.

Sales Growth

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Over the last three years, RingCentral grew its sales at a tepid 16.8% compounded annual growth rate. This shows it failed to expand in any major way, a rough starting point for our analysis.

This quarter, RingCentral reported year-on-year revenue growth of 9.1%, and its $608.8 million of revenue exceeded Wall Street’s estimates by 1.1%. Management is currently guiding for a 7.1% year-on-year increase next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 7.6% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and illustrates the market thinks its products and services will face some demand challenges.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Billings

In addition to revenue, billings is a non-GAAP metric that sheds additional light on RingCentral’s business quality. Billings is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Over the last year, RingCentral’s billings growth has slightly underperformed the sector, averaging 9.6% year-on-year increases and coming in at $607.7 million in the latest quarter. This performance mirrored its revenue and suggests there may be increasing competition that is causing challenges in acquiring or retaining customers.

Customer Acquisition Efficiency

Customer acquisition cost (CAC) payback represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for marketing and sales investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

It’s very expensive for RingCentral to acquire new customers as its CAC payback period checked in at 95.3 months this quarter. The company’s inefficiency indicates a highly competitive environment with little differentiation between RingCentral’s products and its peers.

Key Takeaways from RingCentral’s Q3 Results

We enjoyed seeing RingCentral beat analysts’ full-year EPS guidance expectations. We were also glad next quarter’s EPS guidance exceeded Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed analysts’ expectations. Zooming out, we think this was a decent quarter featuring some areas of strength but also some blemishes. The market seemed to focus on the negatives, and the stock traded down 2% to $38 immediately following the results.

So do we think RingCentral is an attractive buy at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.