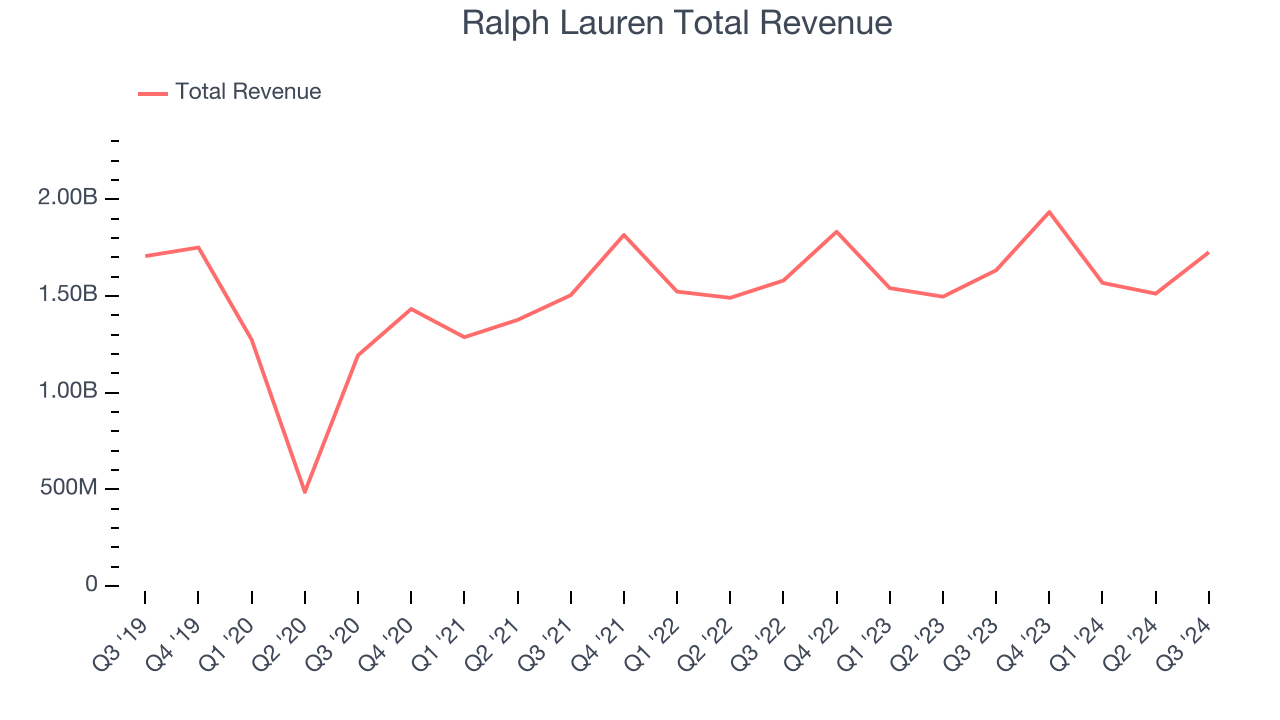

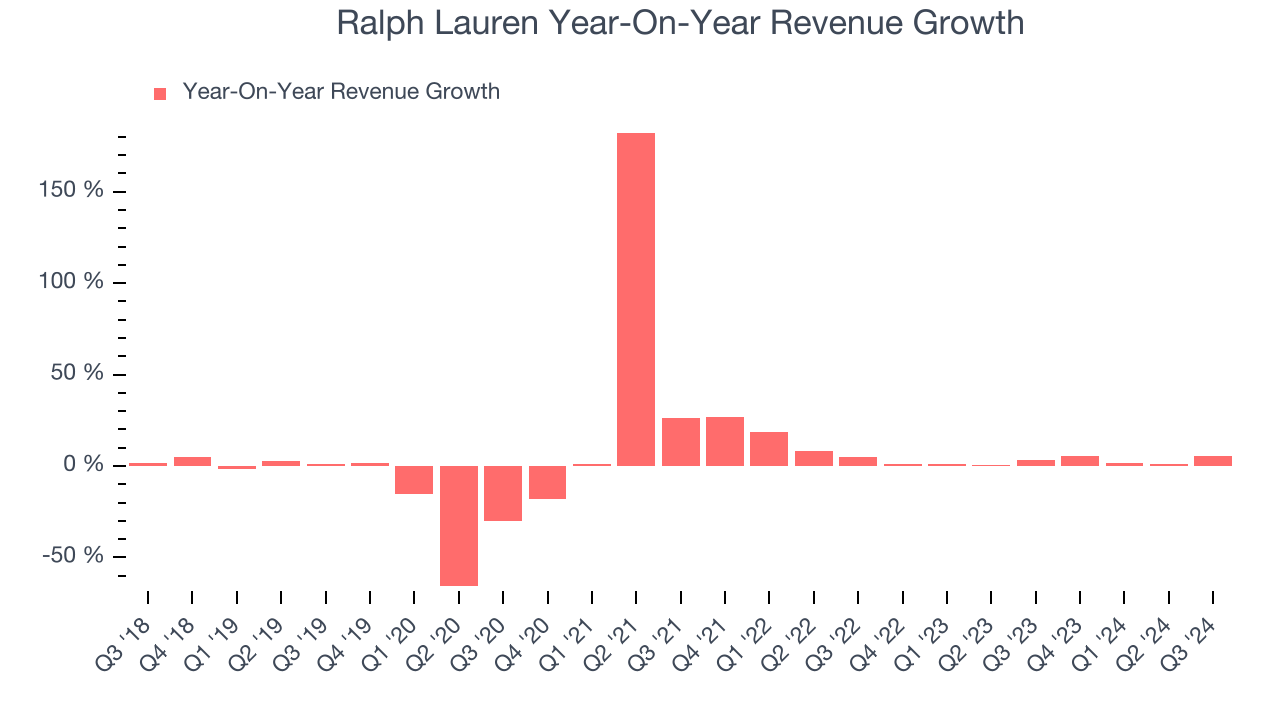

Fashion brand Ralph Lauren (NYSE: RL) announced better-than-expected revenue in Q3 CY2024, with sales up 5.7% year on year to $1.73 billion. Its non-GAAP profit of $2.54 per share was also 5.1% above analysts’ consensus estimates.

Is now the time to buy Ralph Lauren? Find out by accessing our full research report, it’s free.

Ralph Lauren (RL) Q3 CY2024 Highlights:

- Revenue: $1.73 billion vs analyst estimates of $1.68 billion (2.7% beat)

- Adjusted EPS: $2.54 vs analyst estimates of $2.42 (5.1% beat)

- Full year constant currency revenue growth guidance of to 3-4% year on year (slight beat)

- Operating Margin: 10.4%, in line with the same quarter last year

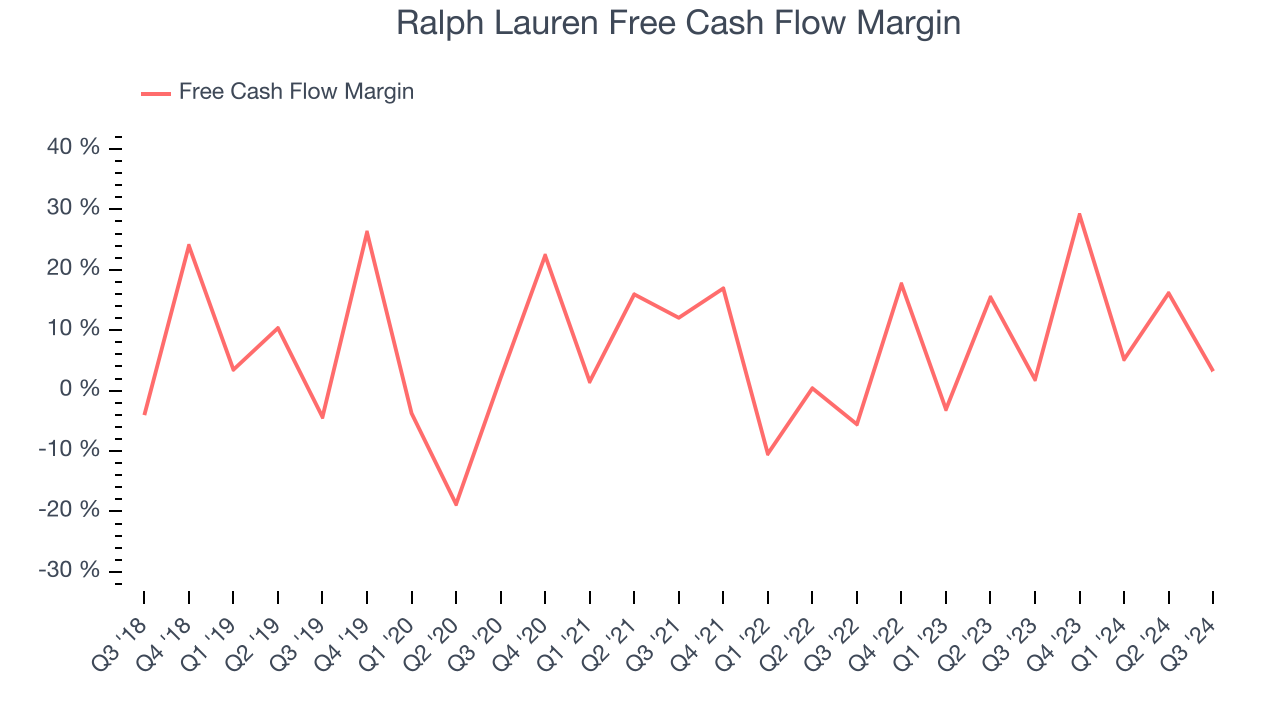

- Free Cash Flow Margin: 3.2%, up from 1.8% in the same quarter last year

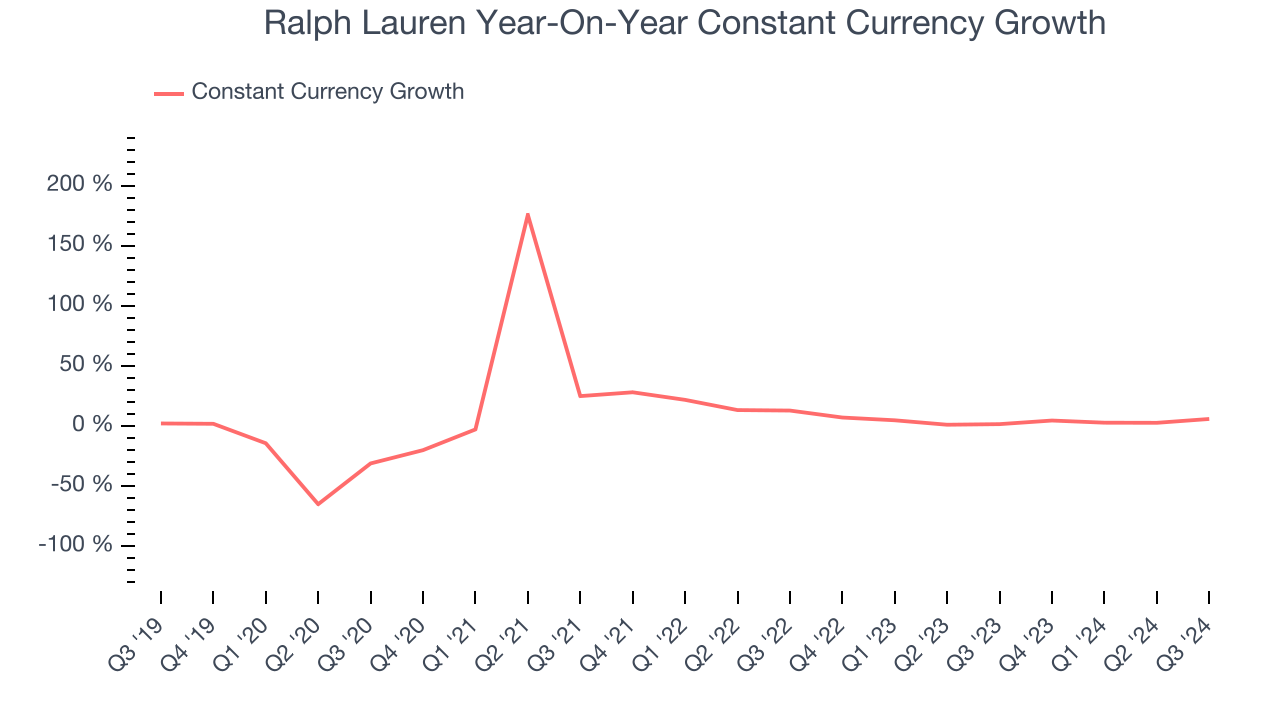

- Constant Currency Revenue rose 6% year on year (1.7% in the same quarter last year)

- Market Capitalization: $12.89 billion

"Our teams are executing well on our long-term strategy, injecting energy and excitement behind our storied brand through what continues to be a choppy global operating environment," said Patrice Louvet, President and Chief Executive Officer.

Company Overview

Originally founded as a necktie company, Ralph Lauren (NYSE: RL) is an iconic American fashion brand known for its classic and sophisticated style.

Apparel, Accessories and Luxury Goods

Within apparel and accessories, not only do styles change more frequently today than decades past as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel, accessories, and luxury goods companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Sales Growth

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Over the last five years, Ralph Lauren grew its sales at a weak 1.1% compounded annual growth rate. This shows it failed to expand in any major way, a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Ralph Lauren’s annualized revenue growth of 2.6% over the last two years is above its five-year trend, but we were still disappointed by the results.

Ralph Lauren also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 3.9% year-on-year growth. Because this number aligns with its normal revenue growth, we can see Ralph Lauren’s foreign exchange rates have been steady.

This quarter, Ralph Lauren reported year-on-year revenue growth of 5.7%, and its $1.73 billion of revenue exceeded Wall Street’s estimates by 2.7%.

Looking ahead, sell-side analysts expect revenue to grow 2.8% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates the market thinks its newer products and services will not lead to better top-line performance yet.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Ralph Lauren has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 11.2% over the last two years, slightly better than the broader consumer discretionary sector.

Ralph Lauren’s free cash flow clocked in at $55.5 million in Q3, equivalent to a 3.2% margin. This result was good as its margin was 1.4 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends are more important.

Over the next year, analysts predict Ralph Lauren’s cash conversion will slightly fall. Their consensus estimates imply its free cash flow margin of 14% for the last 12 months will decrease to 12.5%.

Key Takeaways from Ralph Lauren’s Q3 Results

We enjoyed seeing Ralph Lauren exceed analysts’ constant currency revenue expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Looking ahead, the company rounded out a good quarter by giving full year organic revenue growth guidance ahead of expectations. The stock traded up 5.6% to $219.88 immediately after reporting.

So should you invest in Ralph Lauren right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.