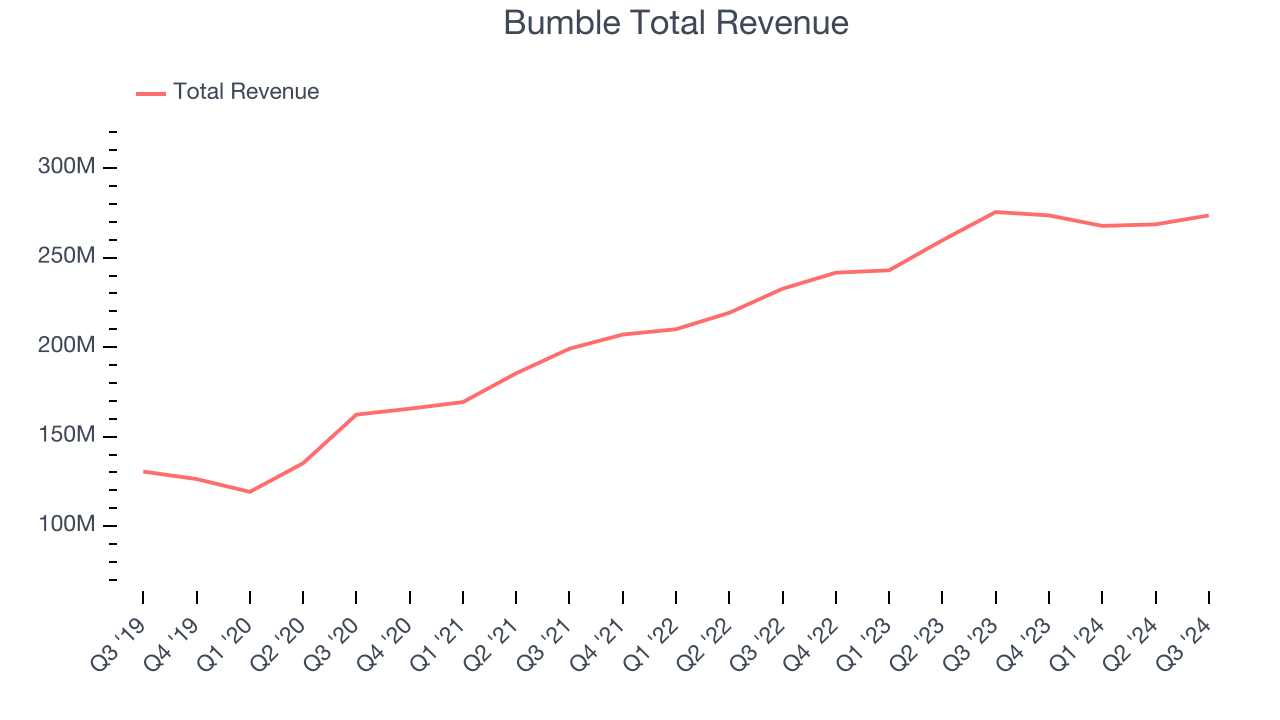

Online dating app Bumble (NASDAQ: BMBL) met Wall Street’s revenue expectations in Q3 CY2024, but sales were flat year on year at $273.6 million. The company expects next quarter’s revenue to be around $259 million, close to analysts’ estimates. Its GAAP loss of $5.11 per share was 2,757% below analysts’ consensus estimates.

Is now the time to buy Bumble? Find out by accessing our full research report, it’s free.

Bumble (BMBL) Q3 CY2024 Highlights:

- Revenue: $273.6 million vs analyst estimates of $271.7 million (in line)

- EPS: -$5.11 vs analyst estimates of $0.19 (-$5.30 miss due to a large, one-time impairment charge of nearly $900 million)

- EBITDA: $82.55 million vs analyst estimates of $78.69 million (4.9% beat)

- Revenue Guidance for Q4 CY2024 is $259 million at the midpoint, roughly in line with what analysts were expecting

- EBITDA guidance for Q4 CY2024 is $71.5 million at the midpoint, below analyst estimates of $73.89 million

- Gross Margin (GAAP): 70.9%, in line with the same quarter last year

- Operating Margin: -306%, down from 10.9% in the same quarter last year

- EBITDA Margin: 30.2%, up from 27.3% in the same quarter last year

- Free Cash Flow Margin: 33.6%, up from 11.6% in the previous quarter

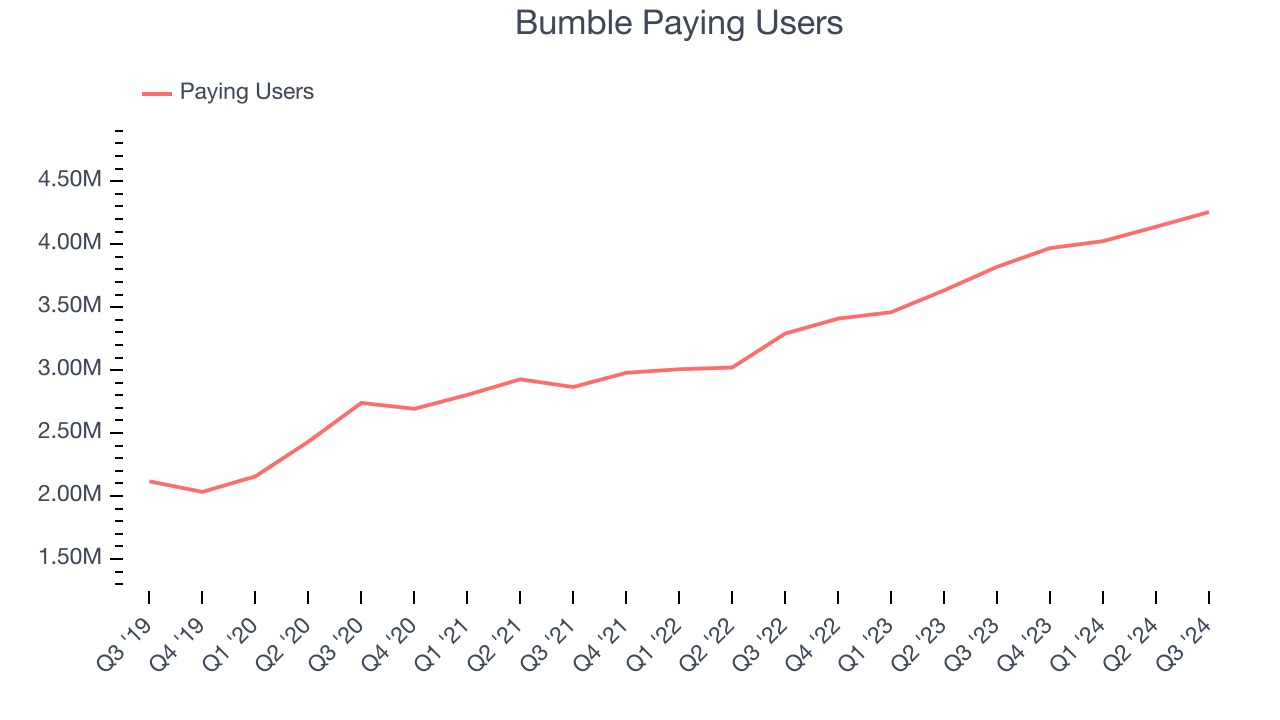

- Paying Users: 4.26 million, up 435,000 year on year

- Market Capitalization: $946.5 million

“We delivered on our financial objectives for the third quarter as we executed on our plans to reimagine Bumble App to enable the next generation of online-to-real-world connections,” said Lidiane Jones, CEO of Bumble Inc.

Company Overview

Founded by the co-founder of Tinder, Whitney Wolfe Herd, Bumble (NASDAQ: BMBL) is a leading dating app built with women at the center.

Consumer Subscription

Consumers today expect goods and services to be hyper-personalized and on demand. Whether it be what music they listen to, what movie they watch, or even finding a date, online consumer businesses are expected to delight their customers with simple user interfaces that magically fulfill demand. Subscription models have further increased usage and stickiness of many online consumer services.

Sales Growth

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Bumble’s sales grew at a solid 14.6% compounded annual growth rate over the last three years. This is a useful starting point for our analysis.

This quarter, Bumble’s $273.6 million of revenue was flat year on year and in line with Wall Street’s estimates. Management is currently guiding for a 5.3% year-on-year decline next quarter.

Looking further ahead, sell-side analysts expect revenue to decline 2.7% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and indicates the market thinks its products and services will face some demand challenges.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Paying Users

Buyer Growth

As a subscription-based app, Bumble generates revenue growth by expanding both its subscriber base and the amount each subscriber spends over time.

Over the last two years, Bumble’s paying users, a key performance metric for the company, increased by 15.5% annually to 4.26 million in the latest quarter. This growth rate is among the fastest of any consumer internet business and indicates its platform's popularity is exploding.

In Q3, Bumble added 435,000 paying users, leading to 11.4% year-on-year growth. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t accelerating buyer growth just yet.

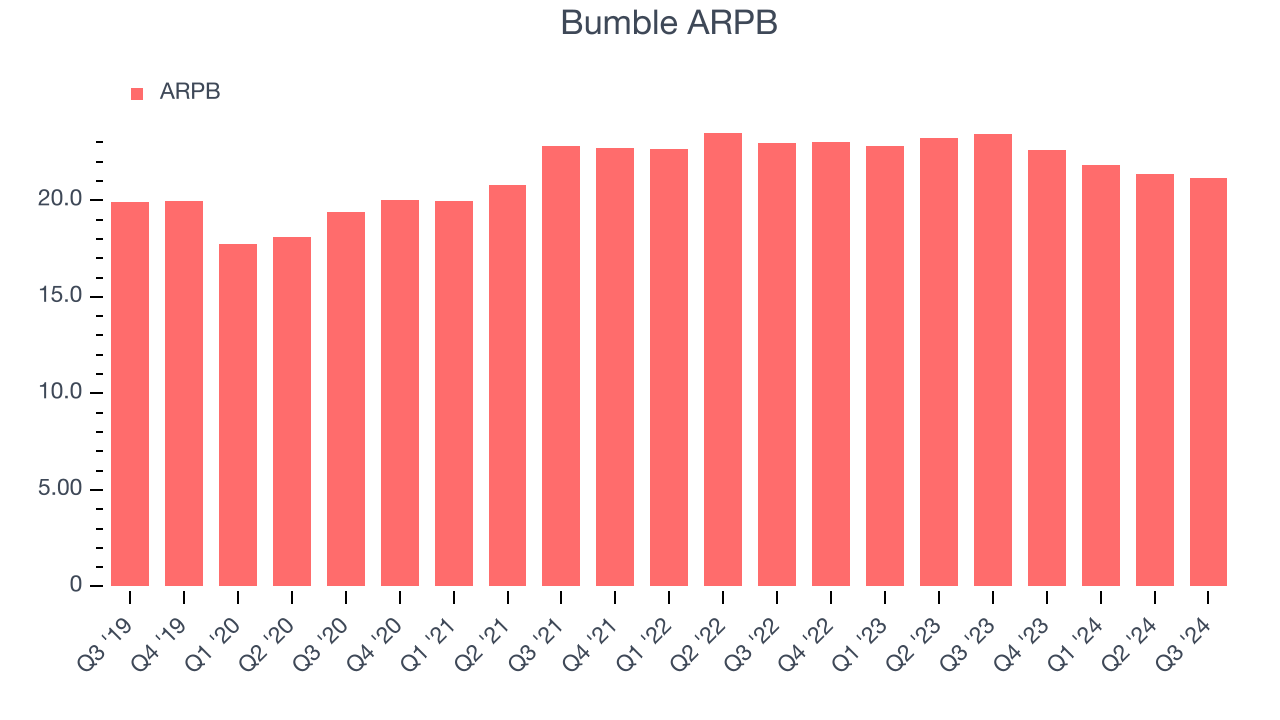

Revenue Per Buyer

Average revenue per buyer (ARPB) is a critical metric to track for consumer internet businesses like Bumble because it measures how much the average buyer spends. ARPB is also a key indicator of how valuable its buyers are (and can be over time).

Bumble’s ARPB fell over the last two years, averaging 2.6% annual declines. This isn’t great, but the increase in paying users is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Bumble tries boosting ARPB by taking a more aggressive approach to monetization, it’s unclear whether buyers can continue growing at the current pace.

This quarter, Bumble’s ARPB clocked in at $21.17. It declined 9.6% year on year, worse than the change in its paying users.

Key Takeaways from Bumble’s Q3 Results

We enjoyed seeing Bumble exceed analysts’ EBITDA expectations this quarter. We were also glad it expanded its number of buyers. On the other hand, its revenue growth regrettably slowed and its EBITDA guidance for next quarter fell short of Wall Street’s estimates despite in line revenue guidance. Overall, this quarter could have been better. The stock traded down 8.6% to $7.17 immediately following the results.

Should you buy the stock or not? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.