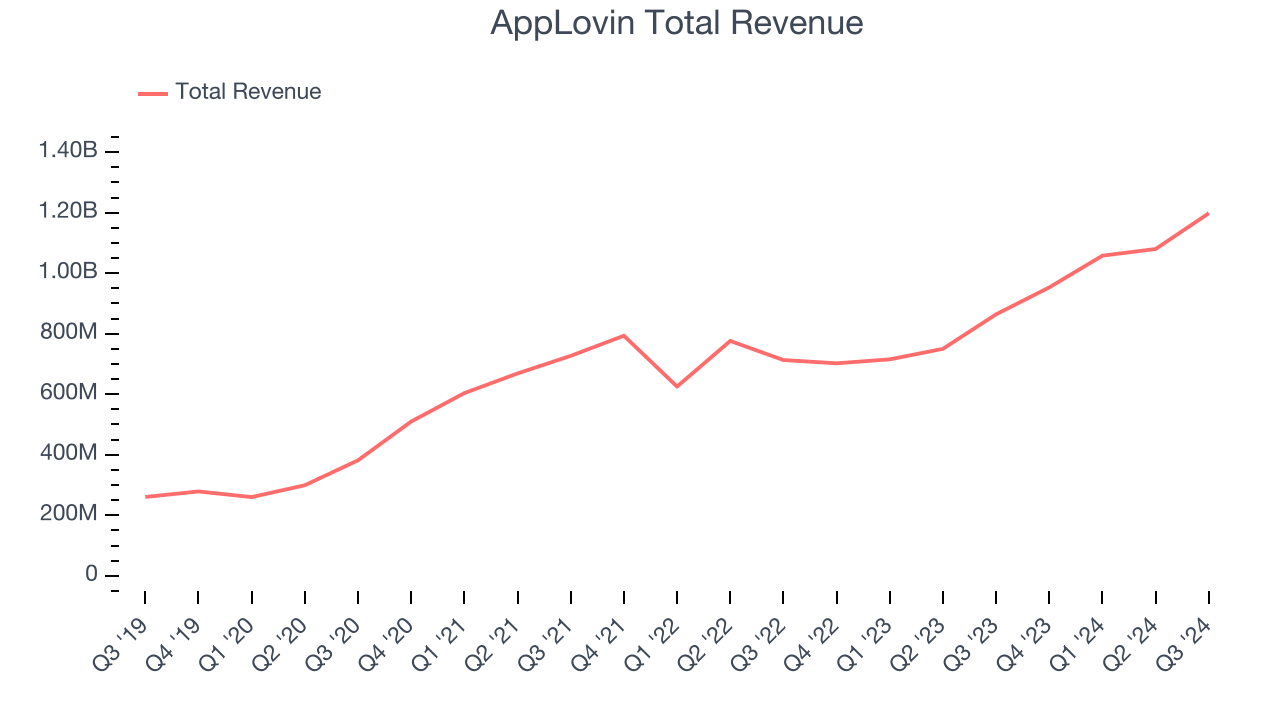

Mobile app advertising platform AppLovin (NASDAQ: APP) reported Q3 CY2024 results exceeding the market’s revenue expectations, with sales up 38.6% year on year to $1.20 billion. Its GAAP profit of $1.25 per share was also 34.8% above analysts’ consensus estimates.

Is now the time to buy AppLovin? Find out by accessing our full research report, it’s free.

AppLovin (APP) Q3 CY2024 Highlights:

- Revenue: $1.20 billion vs analyst estimates of $1.13 billion (5.9% beat)

- EPS: $1.25 vs analyst estimates of $0.93 (34.8% beat)

- EBITDA: $721.6 million vs analyst estimates of $645.5 million (11.8% beat)

- Q4 revenue guidance of $1.25 billion at the midpoint, above expectations of $1.18 billion

- Q4 adjusted EBITDA guidance of $750 million at the midpoint, well above expectations of $667 million

- Gross Margin (GAAP): 77.5%, up from 69.3% in the same quarter last year

- Operating Margin: 44.6%, up from 21.6% in the same quarter last year

- EBITDA Margin: 60.2%, up from 48.5% in the same quarter last year

- Market Capitalization: $55.21 billion

Company Overview

Co-founded by Adam Foroughi, who was frustrated with not being able to find a good solution to market his own dating app, AppLovin (NASDAQ: APP) is both a mobile game studio and provider of marketing and monetization tools for mobile app developers.

Advertising Software

The digital advertising market is large, growing, and becoming more diverse, both in terms of audiences and media. As a result, there is a growing need for software that enables advertisers to use data to automate and optimize ad placements.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, AppLovin’s 19.6% annualized revenue growth over the last three years was mediocre. This shows it couldn’t expand in any major way, a tough starting point for our analysis.

This quarter, AppLovin reported wonderful year-on-year revenue growth of 38.6%, and its $1.20 billion of revenue exceeded Wall Street’s estimates by 5.9%.

Looking ahead, sell-side analysts expect revenue to grow 16.8% over the next 12 months, a slight deceleration versus the last three years. This projection is still healthy and indicates the market sees success for its products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

AppLovin is extremely efficient at acquiring new customers, and its CAC payback period checked in at 16.8 months this quarter. The company’s efficiency indicates that it has a highly differentiated product offering and strong brand reputation, giving it the freedom to invest resources into new growth initiatives while maintaining optionality.

Key Takeaways from AppLovin’s Q3 Results

This was a classic 'beat and raise' quarter. Specifically, we were impressed by how AppLovin beat analysts’ revenue, EBITDA, and EPS expectations this quarter. Looking ahead, Q4 guidance was also very encouraging, with revenue and EBITDA guidance coming in ahead, the latter well ahead. Zooming out, we think this was a great quarter amid potentially lower expectations given the company's uneven performance in the last few quarters. The stock traded up 28.5% to $216.60 immediately following the results.

Sure, AppLovin had a solid quarter, but if we look at the bigger picture, is this stock a buy? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.