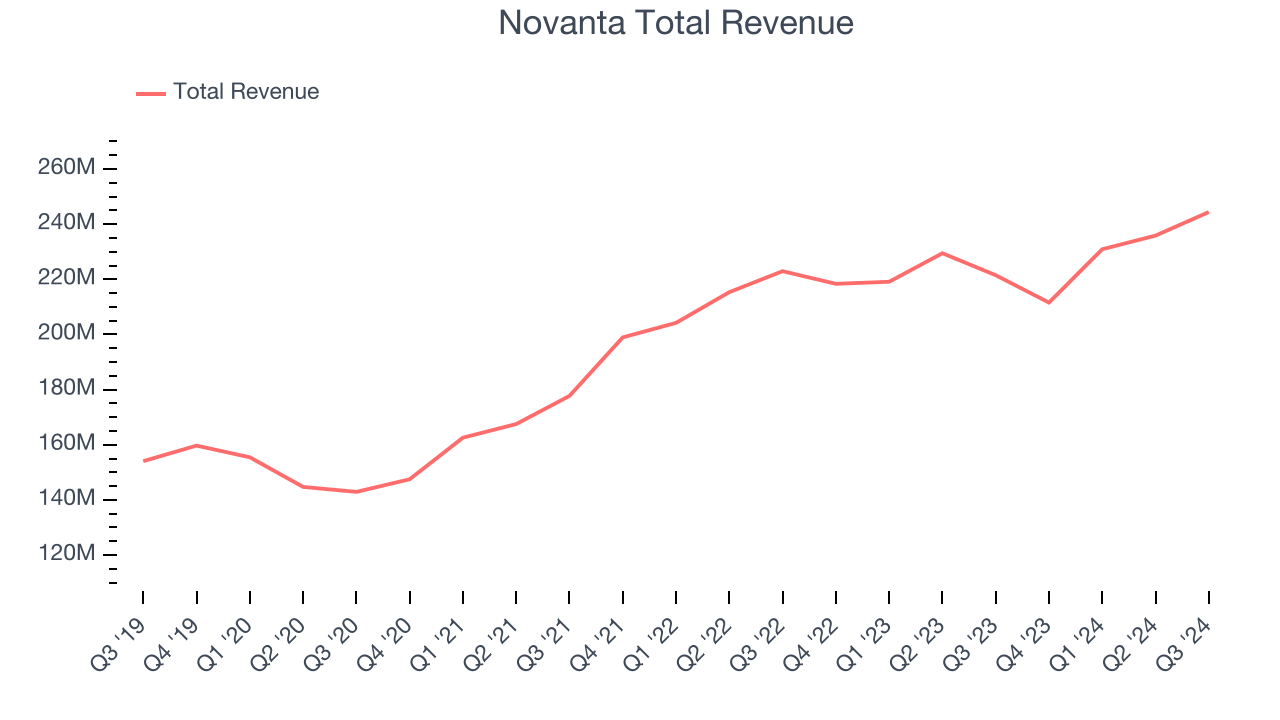

Medicine and manufacturing technology provider Novanta (NASDAQ: NOVT) met Wall Street’s revenue expectations in Q3 CY2024, with sales up 10.3% year on year to $244.4 million. On the other hand, next quarter’s revenue guidance of $239.5 million was less impressive, coming in 9.3% below analysts’ estimates. Its GAAP profit of $0.53 per share was 3.6% below analysts’ consensus estimates.

Is now the time to buy Novanta? Find out by accessing our full research report, it’s free.

Novanta (NOVT) Q3 CY2024 Highlights:

- Revenue: $244.4 million vs analyst estimates of $242.3 million (in line)

- EPS: $0.53 vs analyst expectations of $0.55 (3.6% miss)

- EBITDA: $56.98 million vs analyst estimates of $56.5 million (small beat)

- Revenue Guidance for Q4 CY2024 is $239.5 million at the midpoint, below analyst estimates of $264 million

- EBITDA guidance for the full year is $209 million at the midpoint, below analyst estimates of $219.4 million

- Gross Margin (GAAP): 44.7%, down from 45.9% in the same quarter last year

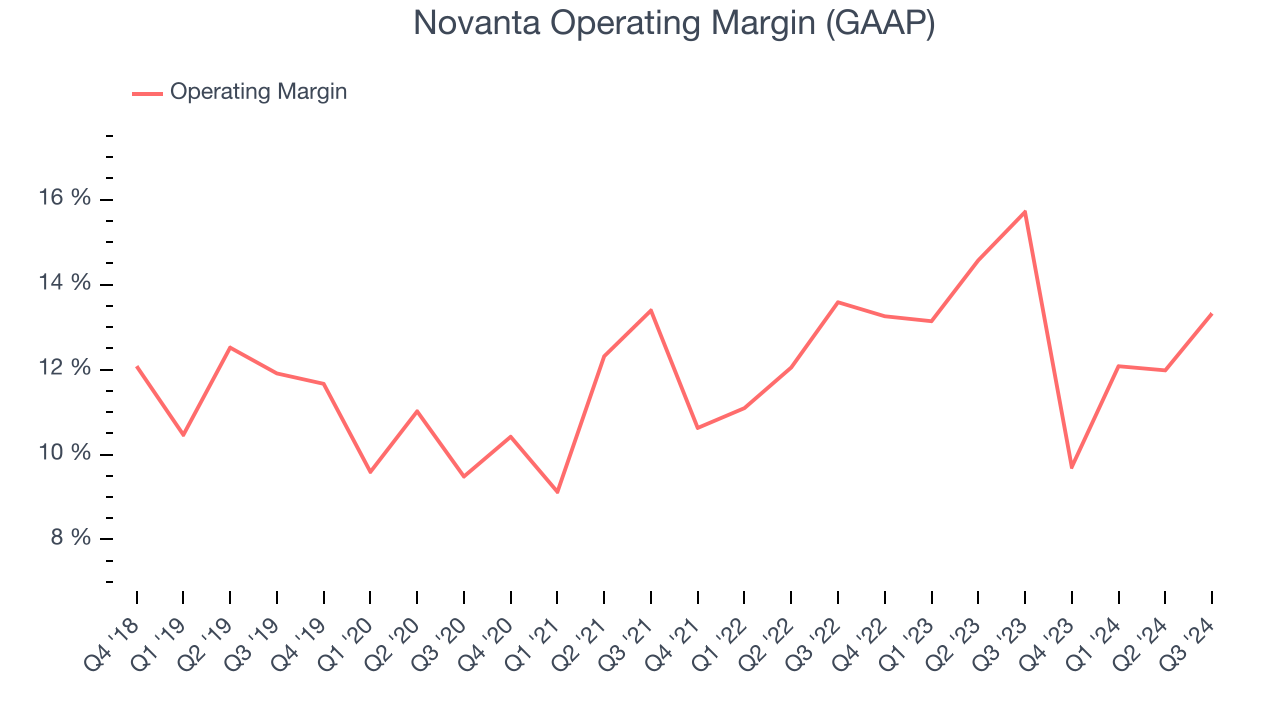

- Operating Margin: 13.3%, down from 15.7% in the same quarter last year

- EBITDA Margin: 23.3%, up from 19.9% in the same quarter last year

- Free Cash Flow Margin: 8%, down from 17.1% in the same quarter last year

- Market Capitalization: $6.25 billion

“Our team delivered strong third quarter results, at the top end of our guidance range, driven by the strength of our diversified business and the Novanta Growth System operating model,” said Matthijs Glastra, Chair and Chief Executive Officer.

Company Overview

Originally a pioneer in the laser scanning industry during the late 1960s, Novanta (NASDAQ: NOVT) offers medicine and manufacturing technology to the medical, life sciences, and manufacturing industries.

Electronic Components

Like many equipment and component manufacturers, electronic components companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include data centers and telecommunications, which can benefit companies whose optical and transceiver offerings fit those markets. But like the broader industrials sector, these companies are also at the whim of economic cycles. Consumer spending, for example, can greatly impact these companies’ volumes.

Sales Growth

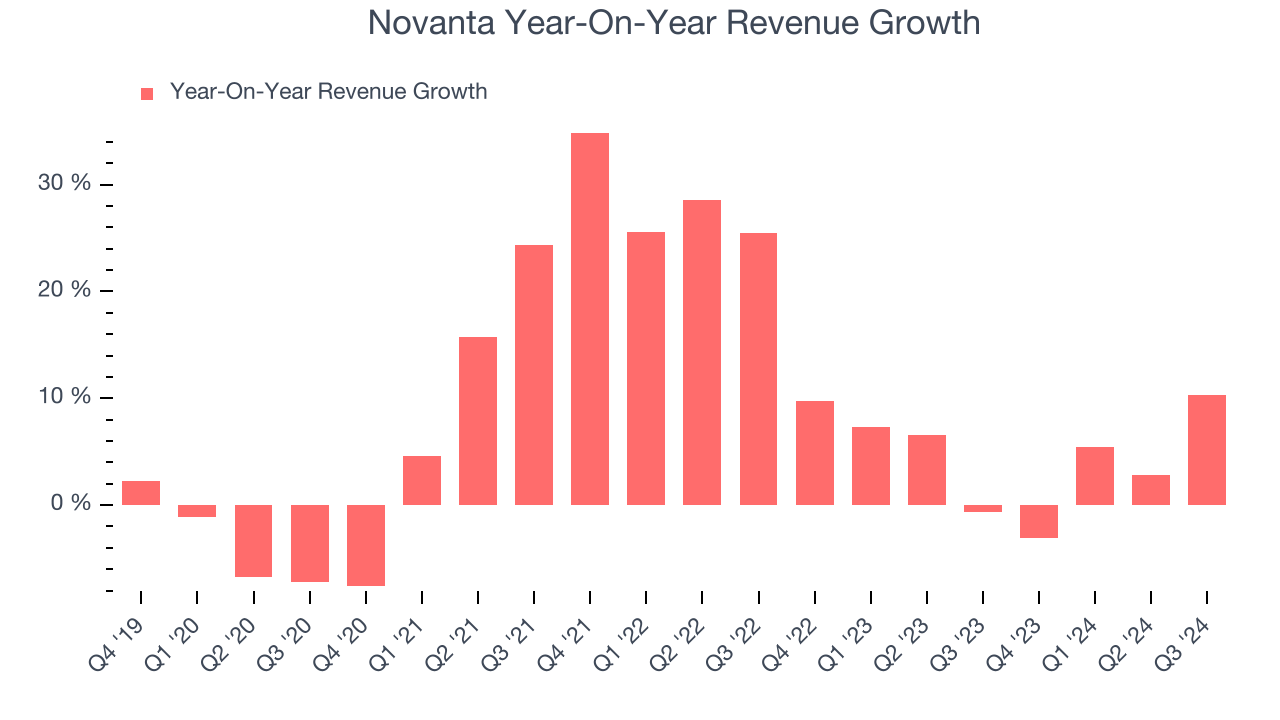

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Over the last five years, Novanta grew its sales at a decent 8.2% compounded annual growth rate. This is a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Novanta’s recent history shows its demand slowed as its annualized revenue growth of 4.7% over the last two years is below its five-year trend.

This quarter, Novanta’s year-on-year revenue growth was 10.3%, and its $244.4 million of revenue was in line with Wall Street’s estimates. Management is currently guiding for a 13.2% year-on-year increase next quarter.

We also like to judge companies based on their projected revenue growth, but not enough Wall Street analysts cover the company for it to have reliable consensus estimates.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Operating Margin

Novanta has been an optimally-run company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 12.1%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Novanta’s annual operating margin rose by 1.4 percentage points over the last five years, showing its efficiency has improved.

This quarter, Novanta generated an operating profit margin of 13.3%, down 2.4 percentage points year on year. Since Novanta’s operating margin decreased more than its gross margin, we can assume it was recently less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

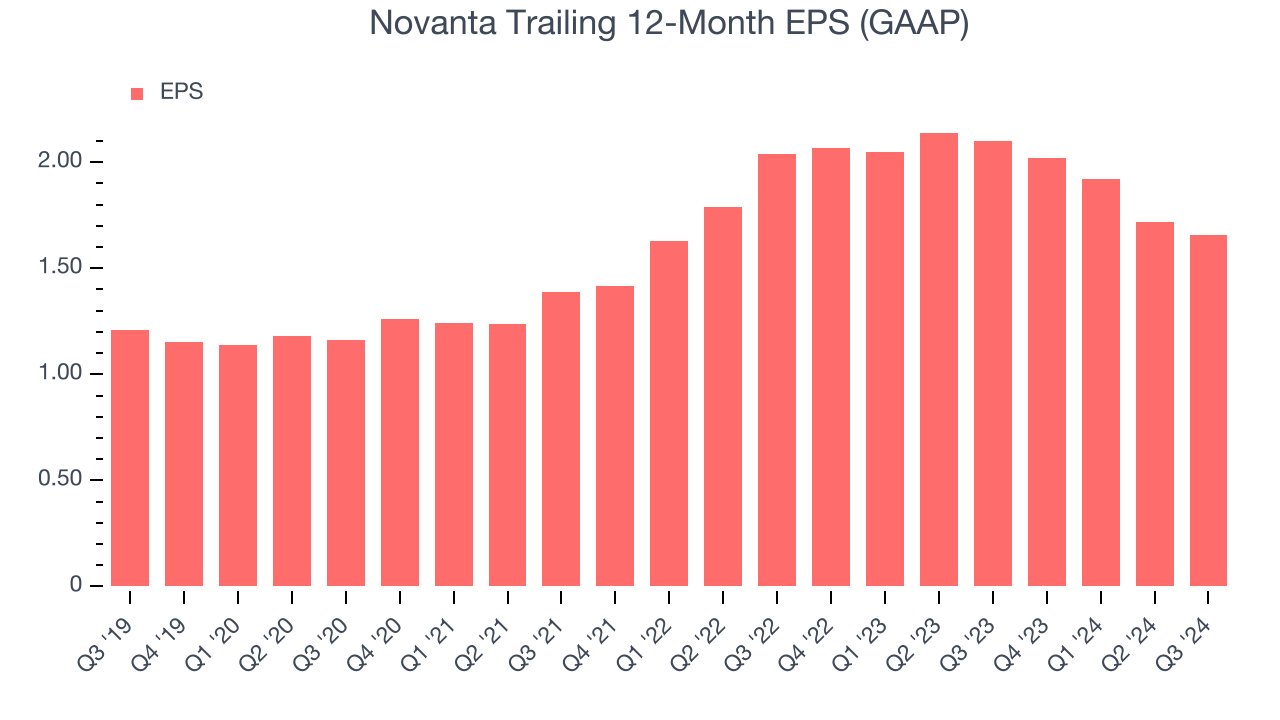

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth was profitable.

Novanta’s EPS grew at an unimpressive 6.5% compounded annual growth rate over the last five years, lower than its 8.2% annualized revenue growth. However, its operating margin actually expanded during this timeframe, telling us that non-fundamental factors affected its ultimate earnings.

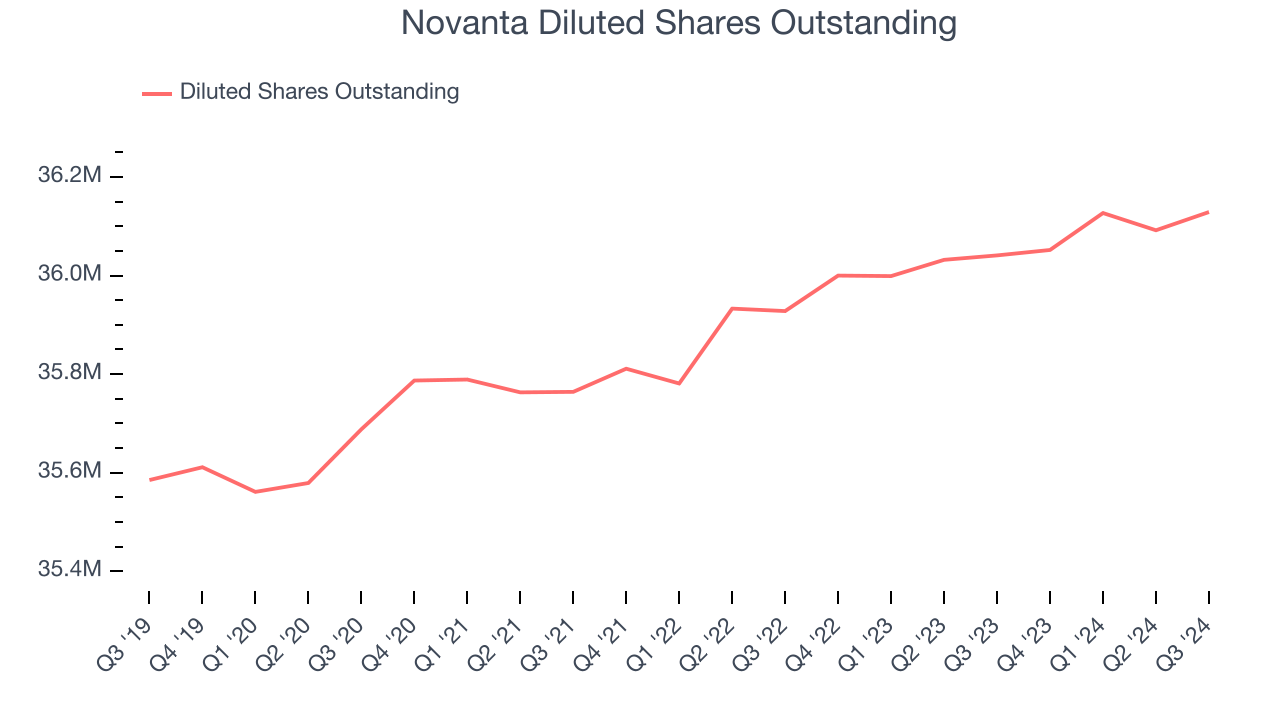

Diving into the nuances of Novanta’s earnings can give us a better understanding of its performance. A five-year view shows Novanta has diluted its shareholders, growing its share count by 1.5%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Novanta, its two-year annual EPS declines of 9.8% show it’s continued to underperform. These results were bad no matter how you slice the data.In Q3, Novanta reported EPS at $0.53, down from $0.59 in the same quarter last year. This print missed analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Novanta’s Q3 Results

It was good to see Novanta beat analysts’ revenue expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its EBITDA forecast for the full year missed and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $174.19 immediately following the results.

Novanta’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.