Gas handling company Chart (NYSE: GTLS) fell short of the market’s revenue expectations in Q3 CY2024, but sales rose 18.3% year on year to $1.06 billion. The company’s full-year revenue guidance of $4.25 billion at the midpoint came in 3.5% below analysts’ estimates. Its non-GAAP profit of $2.18 per share was also 12.1% below analysts’ consensus estimates.

Is now the time to buy Chart? Find out by accessing our full research report, it’s free.

Chart (GTLS) Q3 CY2024 Highlights:

- Revenue: $1.06 billion vs analyst estimates of $1.09 billion (2.8% miss)

- Adjusted EPS: $2.18 vs analyst expectations of $2.48 (12.1% miss)

- EBITDA: $260.7 million vs analyst estimates of $260.3 million (small beat)

- Adjusted EPS guidance for the full year is $9.00 at the midpoint, missing analyst estimates by 9.9%

- EBITDA guidance for the full year is $1.03 billion at the midpoint, below analyst estimates of $1.07 billion

- Gross Margin (GAAP): 34.1%, up from 30.8% in the same quarter last year

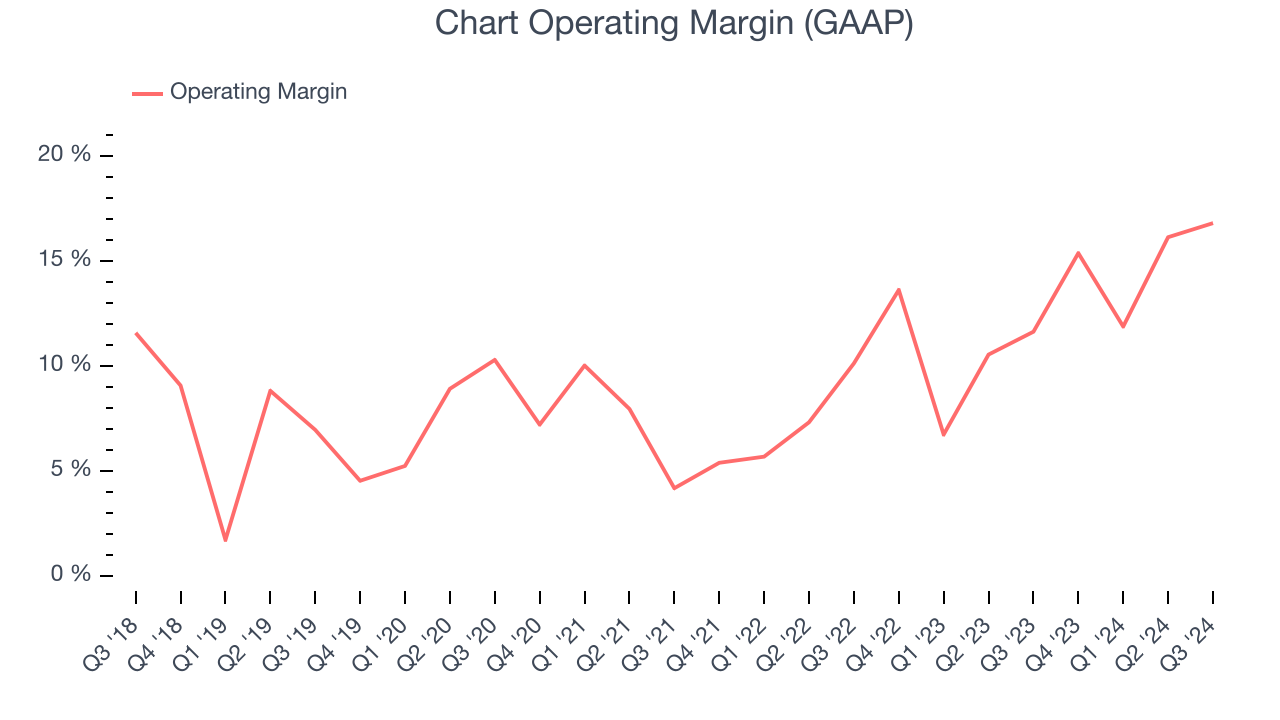

- Operating Margin: 16.8%, up from 11.6% in the same quarter last year

- EBITDA Margin: 24.5%, up from 21.7% in the same quarter last year

- Free Cash Flow was $174.5 million, up from -$86.2 million in the same quarter last year

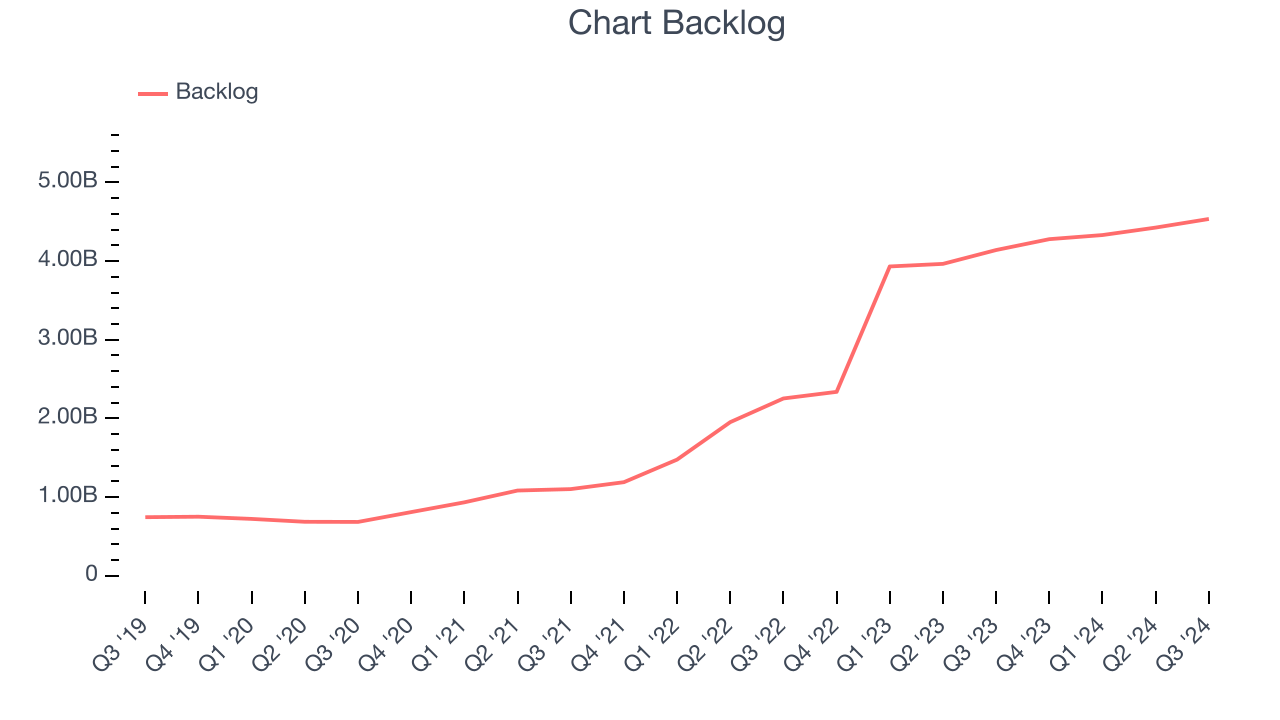

- Backlog: $4.54 billion at quarter end, up 9.5% year on year

- Market Capitalization: $5.08 billion

“We generated $174.6 million of free cash flow in the third quarter 2024 which was used for the reduction of our net debt and contributed to the decrease in our net leverage ratio to 3.04 as of September 30, 2024,” stated Jill Evanko, Chart’s CEO and President.

Company Overview

Installing the first bulk Co2 tank for McDonalds’s sodas, Chart (NYSE: GTLS) provides equipment to store and transport gasses.

Gas and Liquid Handling

Gas and liquid handling companies possess the technical know-how and specialized equipment to handle valuable (and sometimes dangerous) substances. Lately, water conservation and carbon capture–which requires hydrogen and other gasses as well as specialized infrastructure–have been trending up, creating new demand for products such as filters, pumps, and valves. On the other hand, gas and liquid handling companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

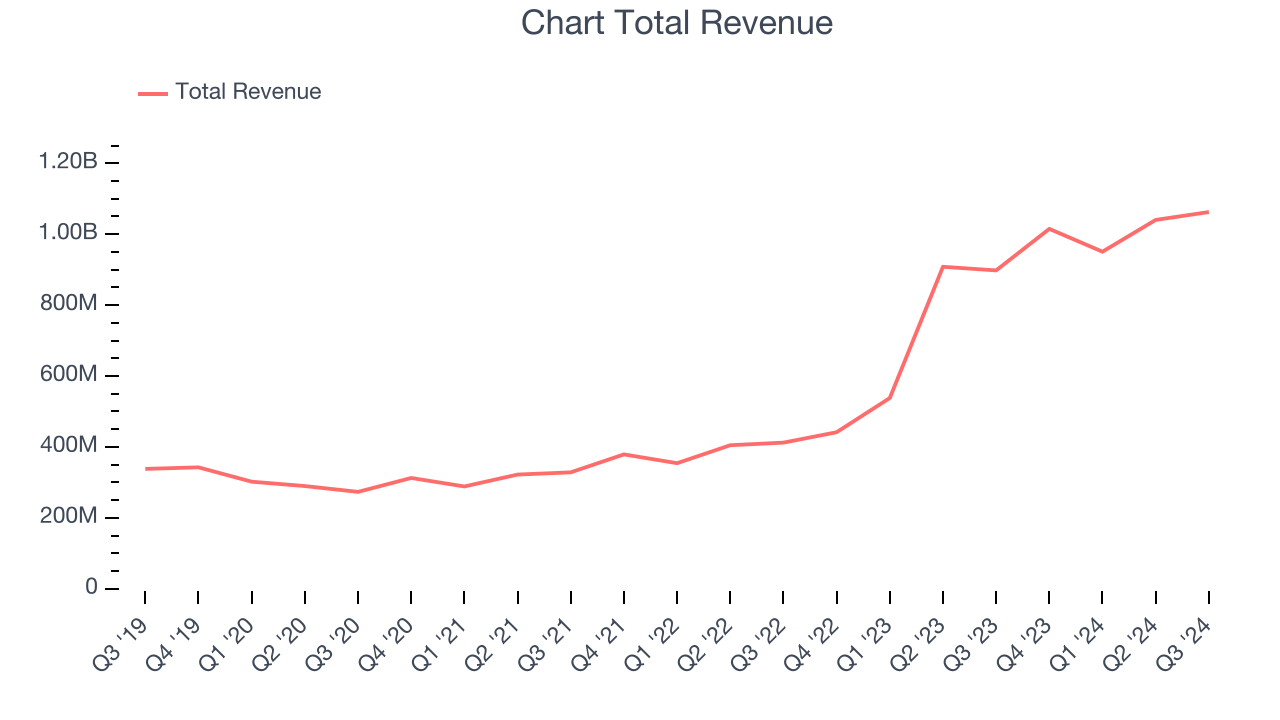

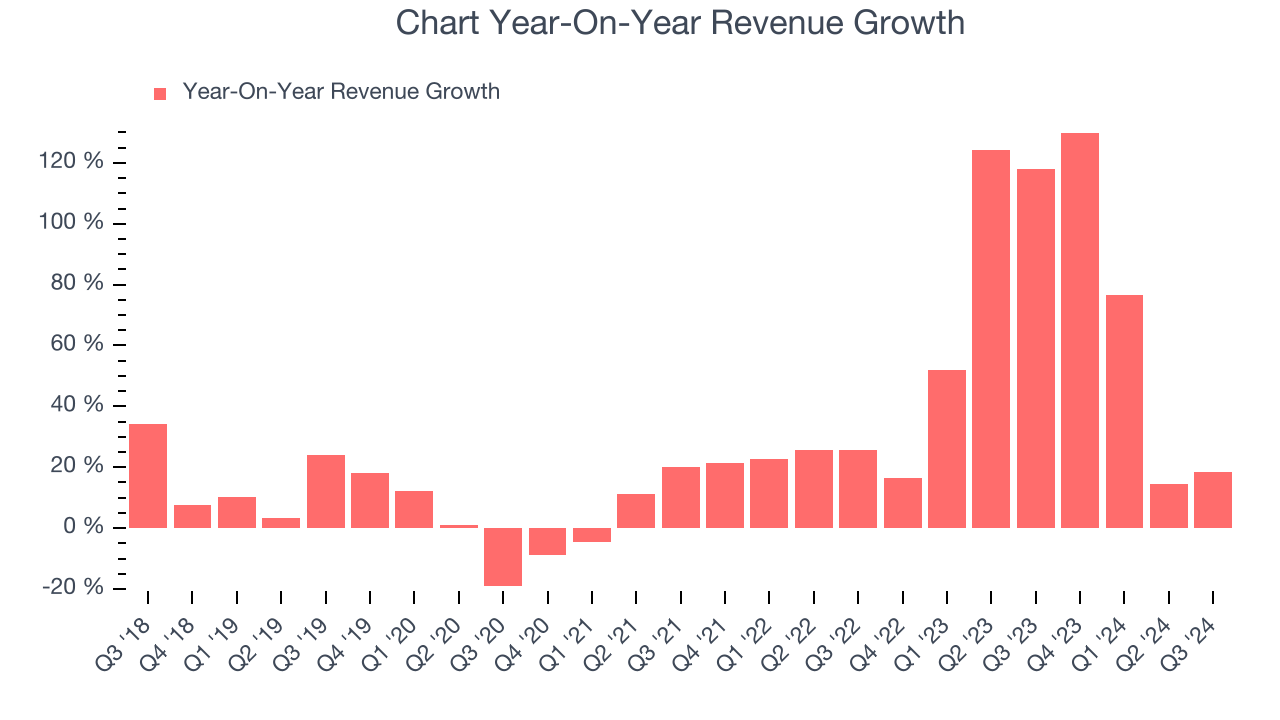

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Luckily, Chart’s sales grew at an incredible 28% compounded annual growth rate over the last five years. This is a great starting point for our analysis because it shows Chart’s offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Chart’s annualized revenue growth of 62% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Chart’s backlog reached $4.54 billion in the latest quarter and averaged 70.5% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Chart’s products and services but raises concerns about capacity constraints.

This quarter, Chart’s revenue grew 18.3% year on year to $1.06 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 18.3% over the next 12 months, a deceleration versus the last two years. Still, this projection is admirable and illustrates the market sees success for its products and services.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Chart has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 11%.

Looking at the trend in its profitability, Chart’s annual operating margin rose by 8.1 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Chart generated an operating profit margin of 16.8%, up 5.2 percentage points year on year. The increase was solid, and since its operating margin rose more than its gross margin, we can infer it was recently more efficient with expenses such as marketing, R&D, and administrative overhead.

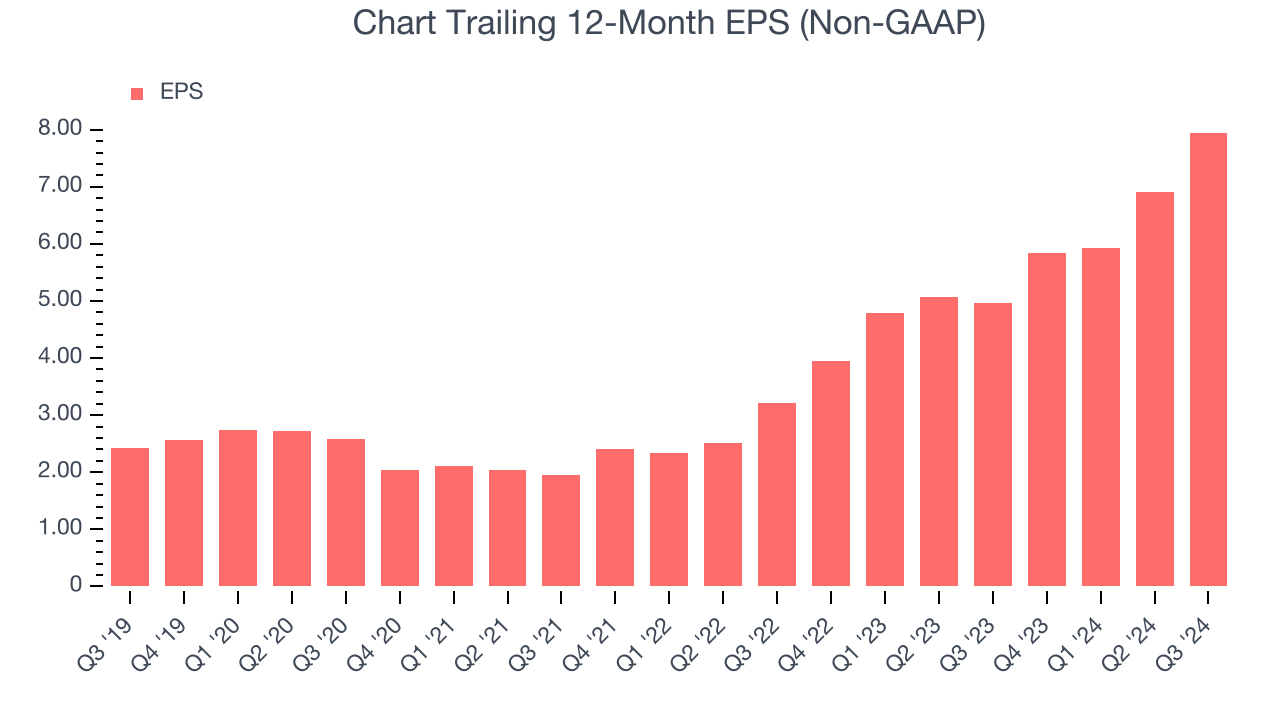

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth was profitable.

Chart’s EPS grew at an astounding 26.7% compounded annual growth rate over the last five years. Despite its operating margin expansion during that time, this performance was lower than its 28% annualized revenue growth. This tells us that non-fundamental factors affected its ultimate earnings.

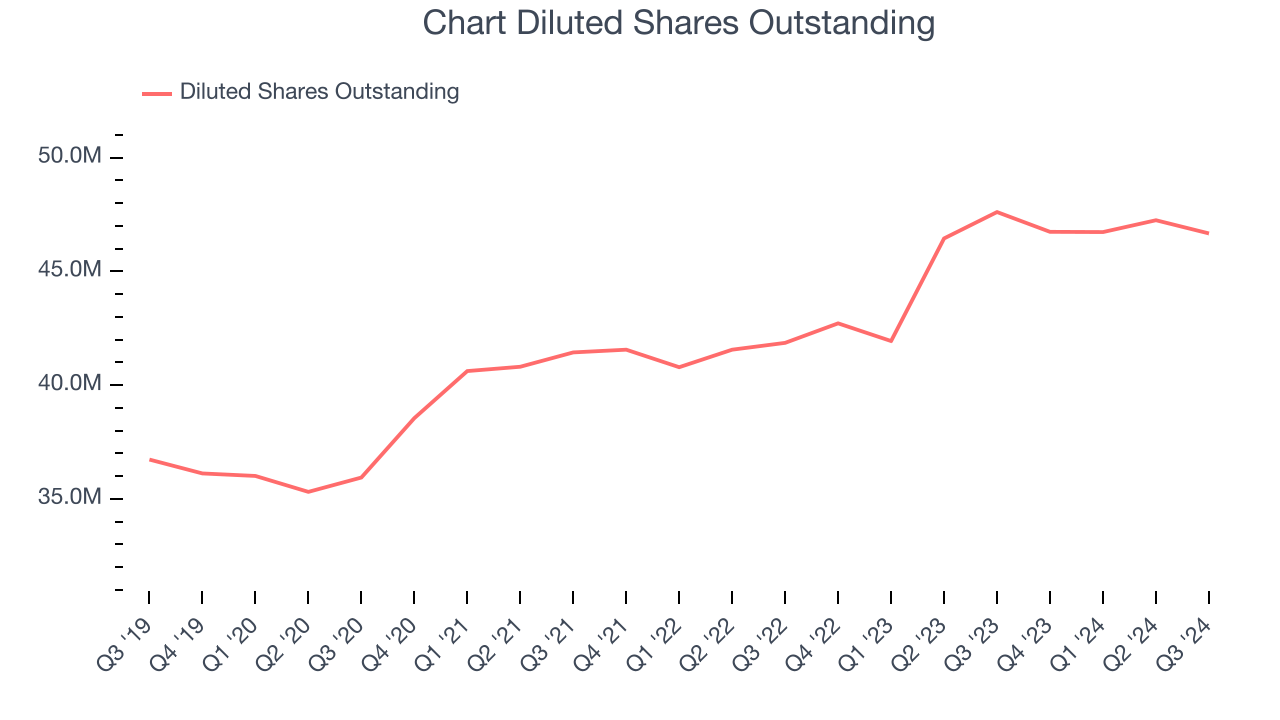

We can take a deeper look into Chart’s earnings to better understand the drivers of its performance. A five-year view shows Chart has diluted its shareholders, growing its share count by 27.1%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Chart, its two-year annual EPS growth of 57.1% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.In Q3, Chart reported EPS at $2.18, up from $1.14 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Chart’s full-year EPS of $7.95 to grow by 55.4%.

Key Takeaways from Chart’s Q3 Results

We enjoyed seeing Chart exceed analysts’ backlog expectations this quarter. On the other hand, its full-year revenue guidance missed and its EBITDA guidance for the full year fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 6% to $113.44 immediately following the results.

Chart didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.