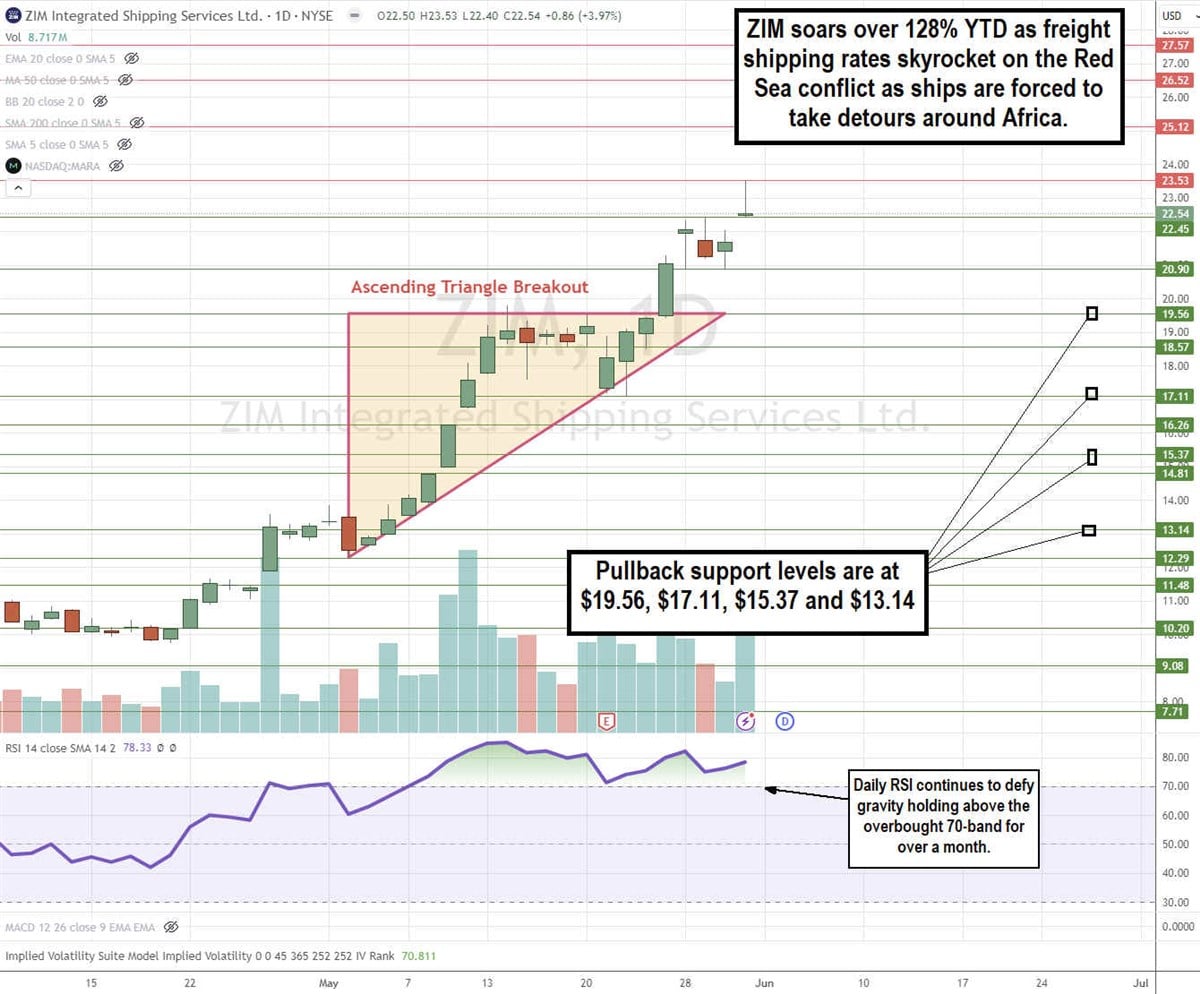

Global container ship company Zim Integrated Shipping Service Ltd. (NYSE: ZIM) shares have been on a tear, rising 128% year-to-date (YTD). Its shares recovered dramatically since the start of the Red Sea conflict, causing shipping companies to detour through South Africa. ZIM shares were trading down under $10 in April 2024. Meanwhile, shipping rates rebounded dramatically, as indicated on the Shanghai Container Freight Index surged to 3,044 on May 31, 2024, up from 993 in November 2023.

In 2024, electric utilities in the oil/energy sector and shipping companies are two key segments outside of the artificial intelligence (AI) space that are surging.

Zim competes in the transportation sector with peers Danaos Co. (NYSE: DAC), Genco Shipping & Trading Ltd (NYSE: GNK) and Star Bulks Carriers Co. (NASDAQ: SBLK).

Red Sea Turmoil Results in Big Green Payoffs for ZIM

Based out of Israel, Zim is the nation's largest cargo shipping company, with over 135 ships in operation. It offers container shipping as well as reefer, project, dry bulk, breakbulk and dangerous cargo services. Shares suffered initially when the Houthi rebels of Yemen launched attacks on cargo ships in the Red Sea.

This caused container ships to avoid the Suez Canal, which accounts for 15% of the world’s cargo volume, and instead take a longer detour around Cape of Good Hope in Africa, which tacks on an additional 4,000 miles and 10 to 14 days. While attempting to hurt Israeli commerce ships, shipping freight rates have skyrocketed as the conflict inadvertently resulted in a windfall for shipping companies. Zim’s stock price is a testament to this.

ZIM Forms a Daily Ascending Triangle Breakout

The daily candlestick chart on ZIM illustrates an ascending triangle breakout pattern. The ascending trendline formed at $12.29 on May 2, 2024, as shares rose to the flat-top resistance at $19.56. The ascending trendline is comprised of higher lows on pullbacks. ZIM tested the ascending trendline heading into its earnings report but squeezed higher afterward as a sell-the-news reaction turned into a buy-the-news reaction, sending shares through the $19.56 resistance. ZIM peaked at $23.53. The daily relative strength index (RSI) rose through the overbought 70-band on May 7, 2024, and has stayed above there ever since as it continues to float at the 78-band. Pullback support levels are at $19.56, $17.11, $15.37 and $13.14.

ZIM's Profitable Q1 2024 Earnings Report

On May 21, 2024, Zim reported Q1 2024 EPS of 75 cents, missing consensus estimates by $1.18. Net income was $92 million and adjusted EBITA was $427 million, up 14% YoY. A vast improvement compared to a loss of $58 million in the year-ago period. Operating income (EBIT) was $167 million compared to a loss of $14 million in Q1 2023. Revenues rose 14% YoY to $1.56 billion. The carried volume was 846,000 twenty-foot equivalent units (TEUs). Average freight rate per TEU was $1,452, up 4% YoY. Zim had a net debt of $2.11 billion at the end of March 31, 2024, compared to $2.31 billion in the year-ago period.

ZIM Increases Dividend and Raises Full Year 2024 Guidance

Zim CEO Eli Glickman noted they have taken steps to revamp its fleet to enhance cost structure. The Board of Directors has approved a 23-cent dividend representing 30% of its quarterly income. The improvement in the freight rate environment has enabled them to increase their full-year 2024 guidance for adjusted EBITDA between $1.15 billion to $1.55 billion and adjusted EBIT between zero to $400 million.

Spot Rate Increases are Spreading

Glickman also commented spot rate increases spread to additional traits, which previously didn't experience rate increases and were not directly impacted by the Red Sea conflict. Indicators of increased demand and constraints on equipment contributed to the pressure on supply. Glickman cautioned that it remains to be seen if the improved demand is sustainable for the remainder of 2024.

Glickman concluded, “Overall market dynamics still point to supply growth significantly outpacing demand growth with significant deliveries this year and to a lesser extent next year as well. As such, our longer-term expectations for the market have not changed. It remains our view that once the Red Sea crisis is resolved, we will likely revert to the supply-demand scenario that had begun to play out in '23. “