Reston, Virginia-based NVR, Inc. (NVR) operates as a homebuilder in the U.S. Valued at $21.2 billion by market cap, the company builds single-family detached homes, town homes, and condominium buildings under the Ryan Homes, NVHomes, and other trade names. NVR provides a number of mortgage related services to its homebuilding customers and to other customers through its mortgage banking operations.

Shares of this homebuilding giant have underperformed the broader market over the past year. NVR has gained 4.4% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 13%. However, in 2026, NVR stock is up 4%, surpassing the SPX’s marginal rise on a YTD basis.

Narrowing the focus, NVR’s underperformance is also apparent compared to the iShares U.S. Home Construction ETF (ITB). The exchange-traded fund has gained about 10% over the past year. Moreover, the ETF’s 15.2% returns on a YTD basis outshines the stock’s single-digit gains over the same time frame.

On Jan. 28, NVR shares closed up by 1.7% after reporting its Q4 results. Its EPS of $121.54 topped Wall Street expectations of $104.96. The company’s revenue was $2.6 billion, beating Wall Street forecasts of $2.4 billion.

For fiscal 2026, ending in December, analysts expect NVR’s EPS to fall 5.3% to $413.28 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimates in three of the last four quarters while missing the forecast on another occasion.

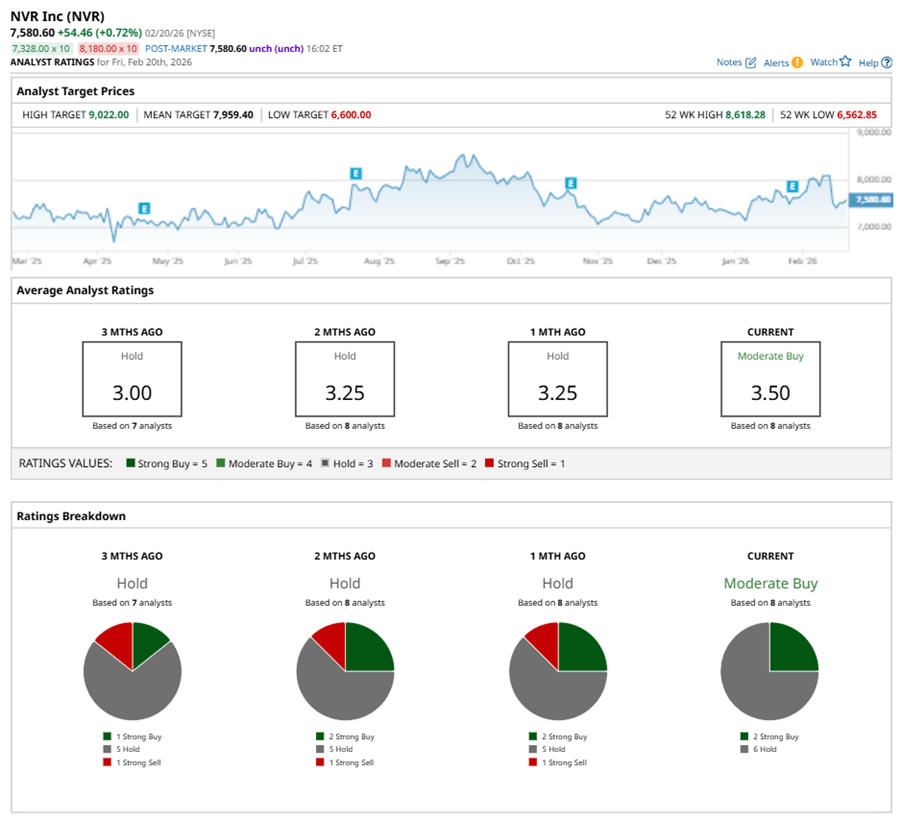

Among the eight analysts covering NVR stock, the consensus is a “Moderate Buy.” That’s based on two “Strong Buy” ratings, and six “Holds.”

This configuration is more bullish than a month ago, with an overall “Hold” rating, consisting of one analyst suggesting a “Strong Sell.”

On Feb. 13, John Lovallo from UBS maintained a “Hold” rating on NVR with a price target of $8,100, implying a potential upside of 6.9% from current levels.

The mean price target of $7,959.40 represents a 5% premium to NVR’s current price levels. The Street-high price target of $9,022 suggests an upside potential of 19%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Stocks Set to Open Lower Amid Tariff Uncertainty, Nvidia Earnings and U.S. Economic Data Awaited

- NVDA Earnings, Tariffs and Other Key Things to Watch this Week

- Record IPOs Are Back: Why Retail Investors May Be Walking Into A Trap

- Adobe (ADBE) Stock Has Been Beaten Up But the Smart Money Remains Resilient