I hope everyone had an enjoyable, restful holiday season. I sure did. Later today, I’ll sit down and watch Indiana face off against Alabama in the Rose Bowl. My niece went to IU, so I’ll most definitely be cheering for the Hoosiers' dream season to continue.

As we move into 2026, part of my focus will be on the options market in general and unusual options activity, more specifically.

This past year was full of ups and downs for investors, but it’s hard to complain about the fourth consecutive year of gains for the S&P 500. Valuations continue to be a concern.

That said, it is New Year’s Day, a time for optimism for the year that lies ahead. I don’t know where the index will finish by the end of 2026 — Bloomberg’s survey of 21 analysts suggests a 9% gain — but, as always, there will be pockets of strength.

When it comes to unusual options activity heading into 2026, these three stocks look like good bets for gains in 2026. I’ve rated them mild, medium, and hot based on their option volume and unusual option activity heading into January.

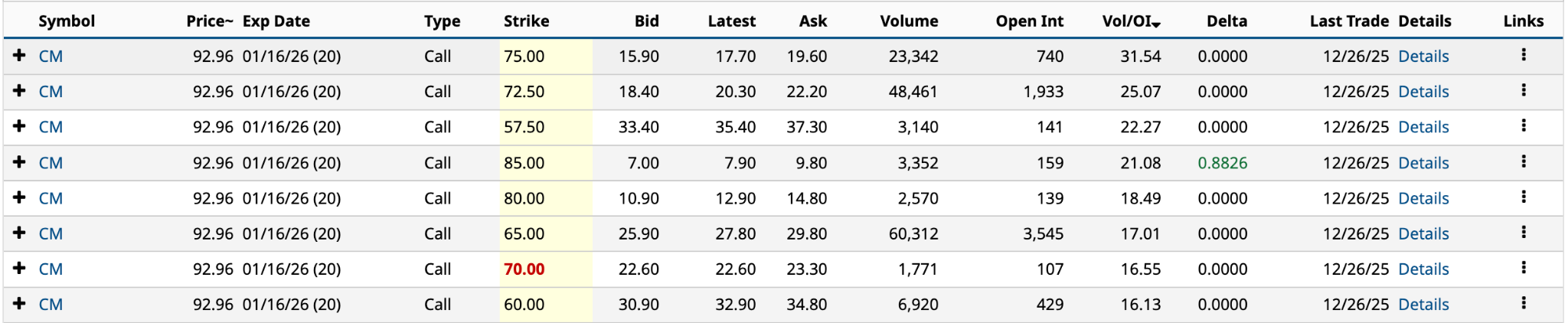

Mild - Canadian Imperial Bank of Commerce (CM)

Canadian Imperial Bank of Commerce (CM), commonly known as CIBC, is Canada’s fifth-largest bank. As of Oct. 31, 2025, it had CAD$1.12 trillion ($815.9 million) in total assets.

JPMorgan (JPM) CEO Jamie Dimon has expressed concern about a 2026 recession. His economists believe the chances of a recession are 33% heading into the new year.

If you’ll remember, the Big Five Canadian bank stocks outperformed their American counterparts during the 2008-2009 financial crisis — JPMorgan stock lost 65% of its value between Oct. 3, 2008, and Jan. 20, 2009, compared to 39% for CM -- and should another big crisis hit, the Canadian banks are positioned to handle the downturn.

However, Canadian bank stock valuations have crept up. According to S&P Global Market Intelligence, CIBC’s P/E ratio based on the latest 12 months is 14.77; the five-year average is 11.94x, so you’re not getting CM for a bargain.

In Dec. 26 trading, CM had options volume of 155,863, 1,788% higher than its 30-day average.

All eight of its unusually active options on Dec. 26 were in the top 100. All eight were expiring on Jan. 16; all were calls. Its Q1 2026 results don’t come out until Feb. 20, so it’s not earnings-related volume.

The 16 analysts covering CIBC are lukewarm on the bank's stock, giving it an Outperform rating according to S&P Global Market Intelligence, but only 2.44 out of 5.

Of Canada’s Big Five banks, CM stock has the second-best performance in 2025, up 39% through Dec. 26, lagging only Toronto-Dominion Bank’s (TD) 69% gain. I see the momentum continuing in 2026.

Medium - Nike (NKE)

The past four years have been a nightmare for long-time Nike (NKE) shareholders, who’ve seen their shares lose nearly 57% of their value, including 19% in 2025.

As someone who mostly wears Adidas (ADDYY), it’s not surprising to me that the Beaverton footwear behemoth has lost its mojo. Their shoes are generally bland and uninspiring.

Since founder Phil Knight stepped aside as CEO in 2004, the company has had some poor chief executives — William Perez lasted 13 months, and John Donahoe lasted four years — forcing it to draw from its alumni, bringing back Elliott Hill in October 2024, who retired in 2020 after 32 years of faithful service.

Fifteen months into Hill’s tenure, the brand appears to be on the rebound, even if it doesn’t show in the share price. UBS’s Evidence Lab just released its 11th global sportswear survey, and Nike appears to be building momentum.

“Two key elements of Nike’s strategy appear to be working under CEO Elliott Hill’s leadership. First, Nike’s prioritization of re-entering the wholesale channel has resulted in a higher percentage of global consumers reporting that Nike products are easy to find in stores and online, reversing a downward trend from 2019 through 2022,” Investing.com reported on Dec. 29.

“... Second, Nike’s refocused emphasis on sports has resonated with consumers. The percentage of consumers who say Nike is ‘good for doing sports’ has rebounded to its 2019 peak level, likely attributable to Hill’s strategic direction.”

Add to this better-than-expected revenues and profits in Q2 2026 -- its earnings per share were 53 cents, 15 cents higher than Wall Street’s estimate, while revenues came in at $12.43 billion, $210 million higher than the consensus.

Unfortunately, the 17% decline in China sent the stock lower. On the plus side, North American revenue was 9% higher in the quarter.

As for Nike’s options volume on Dec. 26, it was 60% higher than its 30-day average. Further, the put/call volume ratio was bullish at 0.70. It had 14 unusually active options on Dec. 26 with Vol/OI ratios above 1.24 and expiring in seven days or more.

It’s a work in progress.

Hot - Nvidia (NVDA)

Not surprisingly, Nvidia (NVDA) had the highest option volume on Dec. 26 at 3.26 million, 45% above its 30-day average, slightly higher than Tesla’s (TSLA) volume on the day, and a put/call volume ratio of 0.46, which is very bullish.

As for its unusual options activity, it had 25 call and put options on Dec. 26 with Vol/OI ratios above 1.24 and expiring in seven days or more. None is particularly attractive.

What can be said about Nvidia that hasn’t already? It’s a cash-generating machine like few others.

In May 2024, I debated whether Nvidia's or Tesla’s 939-day LEAP (Long-Term Equity Anticipation Security) option was the better buy. I sided with CEO Jensen Huang and Nvidia.

“I think AI is as generationally important as the smartphone, perhaps even more so,” I wrote on May 24, 2024.

“So, even though your initial outlay is four-fold higher for Nvidia, I do see it as the better call option to buy for long-term gains.”

How’s that worked out?

There are 354 days remaining until expiration, so the jury is still out. Shortly after my article was published, Nvidia completed a 10-for-1 stock split, which changed the numbers by a factor of 10. The $1,100 call strike is now $110, and the $329.55 ask price would be $32.96 today.

As I write this on Dec. 29, the share price is 41.14% ITM (in the money), with an ask price of $86.75, more than double its May 2024 level. Put another way, the ask price as a percentage of the strike price was 30% back then; today, it’s nearly 79%, an annualized return of over 102%.

As I write this on Dec. 29, the share price is 41.14% ITM (in the money), with an ask price of $86.75, more than double its May 2024 level. Put another way, the ask price as a percentage of the strike price was 30% back then; today, it’s nearly 79%, an annualized return of over 102%.

In May 2024, the share price was about 6% OTM (out of the money). To replicate that situation today, the Jan. 21/2028 $200 call strike, with 753 days to expiration (DTE), is your best bet. As shown below, the $250.65 break-even point is 27.17% above the current share price.

I would make this bet.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- NVDA, NKE, and CM: Bet on These 3 Stocks With Surging Unusual Options Activity for 2026 Gains

- Unusual Activity in Occidental Petroleum Call Options - A Signal Investors Expect a Dividend Hike

- Ethereum Has Crashed, but the Option Strategy I Showed You 3 Months Ago Is Hanging Tough. Now What?

- Tesla Ratio Spread Targets A Profit Zone Between 410 and 430