Princeton, New Jersey-based Bristol-Myers Squibb Company (BMY) discovers, develops, licenses, manufactures, markets, distributes, and sells biopharmaceutical products. With a market cap of $87.2 billion, the company focuses on products and experimental therapies that address cancer, heart disease, HIV and AIDS, diabetes, rheumatoid arthritis, hepatitis, organ transplant rejection, and psychiatric disorders.

Shares of this biopharma giant have considerably underperformed the broader market over the past year. BMY has declined 18.9% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 18.1%. In 2025, BMY stock is down 24.7%, compared to the SPX’s 17.2% gains on a YTD basis.

Narrowing the focus, BMY’s underperformance is also apparent compared to the iShares U.S. Pharmaceuticals ETF (IHE). The exchange-traded fund has gained 5.2% over the past year. Moreover, the ETF’s 12.5% returns on a YTD basis outshine the stock’s losses over the same time frame.

On Oct. 30, Bristol-Myers Squibb released its Q3 results, reporting a 2.8% year-over-year revenue growth to $12.2 billion. However, adjusted EPS fell 9.4% year over year to $1.63. Despite this, BMY raised its fiscal 2025 revenue guidance to $47.5 to $48 billion and updated its adjusted EPS outlook to $6.40 to $6.60.

For the current fiscal year, ending in December, analysts expect BMY’s EPS to grow 453% to $6.36 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

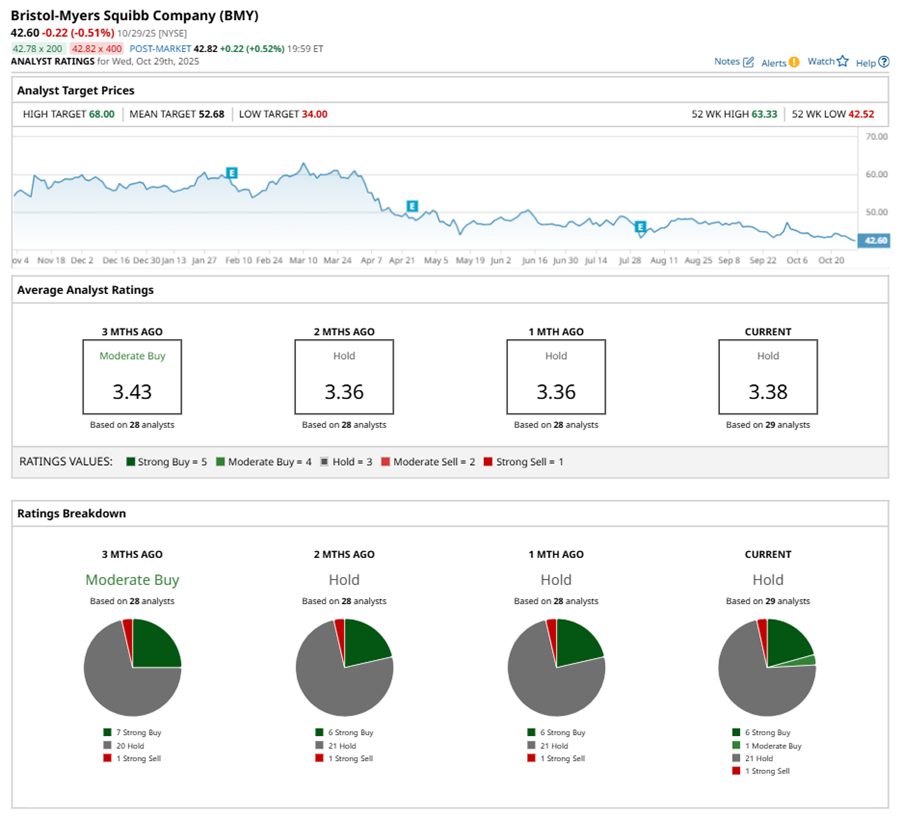

Among the 29 analysts covering BMY stock, the consensus is a “Hold.” That’s based on six “Strong Buy” ratings, one “Moderate Buy,” 21 “Holds,” and one “Strong Sell.”

This configuration is less bullish than three months ago, with seven analysts suggesting a “Strong Buy.”

On Oct. 28, Piper Sandler Companies (PIPR) analyst David Amsellem maintained a “Buy” rating on BMY and set a price target of $64, implying an ambitious potential upside of 50.2% from current levels.

The mean price target of $52.68 represents a 23.7% premium to BMY’s current price levels. The Street-high price target of $68 suggests an ambitious upside potential of 59.6%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Ashes to Alpha: Adobe’s (ADBE) Implosion Offers an Opportunity for a Rebound

- It's 'Going to Be Like a Shockwave' When Tesla's AI Innovations Hit. Should You Buy TSLA Stock First?

- Adobe Systems Bear Put Spread Could Return 233% in this Down Move

- Stocks Fall Before the Open After Mixed Big Tech Earnings, Trump-Xi Summit